Sabitlenmiş Tweet

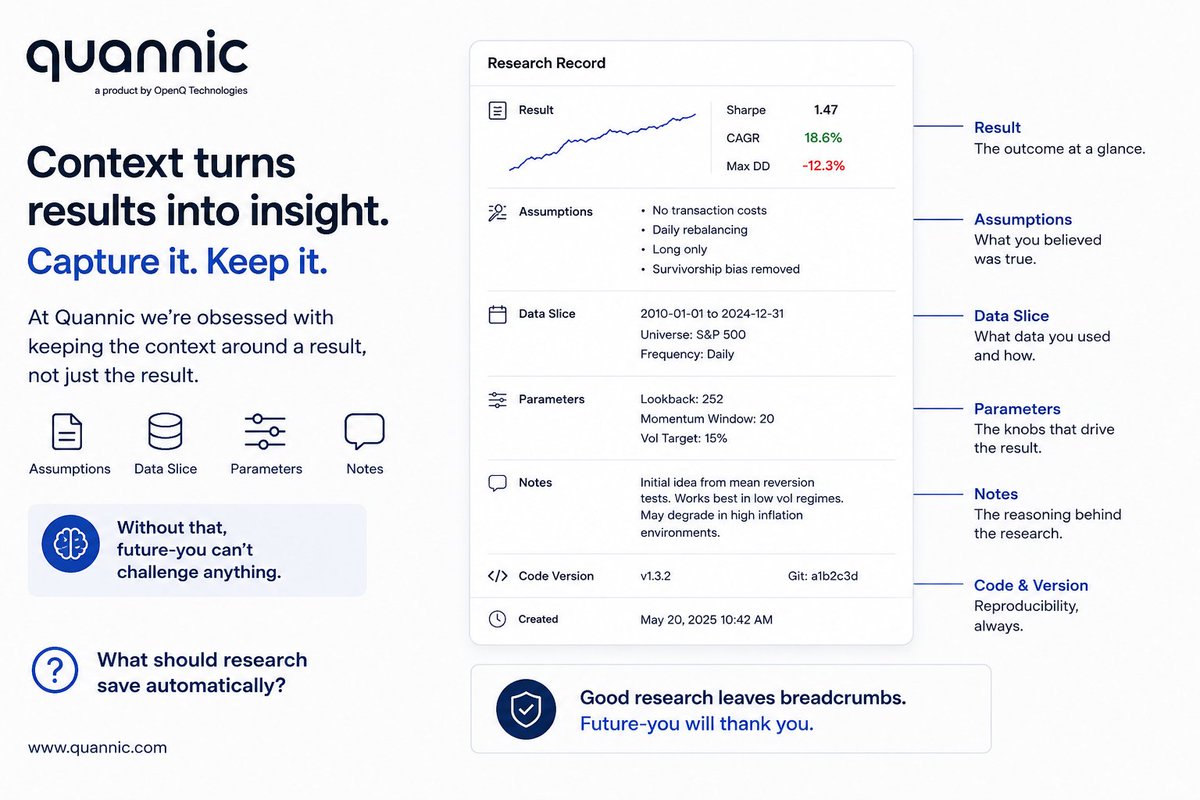

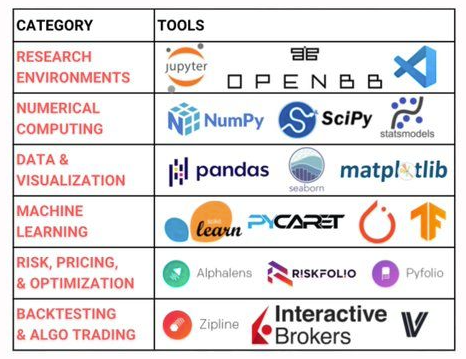

I’m building Quannic.

A no-code platform to build, backtest and deploy quantitative investment strategies without writing code.

Most investors don’t need more stock tips.

They need systems:

clear rules

tested logic

risk management

repeatable execution

Quannic is still in development.

We’re opening a waitlist for early beta testers who want to help shape the product before launch.

Join here:

quannic.com

English