@QueenConspires How are you still finding these? There's 5 locations in my area and all of them were sold out within 3 days and each store got 30-35 of them. 😔

English

P1 Stocks

5.7K posts

@p1stocks

Largest positions: $GME $PBI $EVLV $AMPG $NTDOY $ADBE $NVAX

It is not too late @ryancohen $GME , a list of alternatives from February 2nd: $NXST 6.3B $SAM 2.3B $SFM 6.9B $W 14B $BRKR 7B $MOH 10B $BIRK 7B $SFM 6.9B $SLM 5.5B $NAVI 1B $FMCC 4.8B $FNMA 9.7B $DOM LN 1B $FND 7.4B $POOL 9.5B $KNSL 9.2B $NEU 6.3B $FTDR 4.3B $DOM 14B $OSIS 4.6B $IDT 1.4B $JACK 400mm $SIG 3.8B $ETSY 5.5B $OVV 11B $TDOC 1B $ROKU 15B $GOOS 1.2B $WYNN 11.3B $BEN 13.5B $CMA 12B $HP 3.6B $ADT 6.7B $RH 3.8B $M 5.3B $MGM 9.2B $AGO 4.5B $ANF 4.2B $WTM 5.2B

I know Warren Buffett says that we have never had people in a more gambling mood than now, but i think that is not necessarily the case. We are addicted to S&P 500 buying no matter what. We have been taught to love ETFs no matter what kind. If individual stock investing hadn't been so denigrated it would be less of a casino

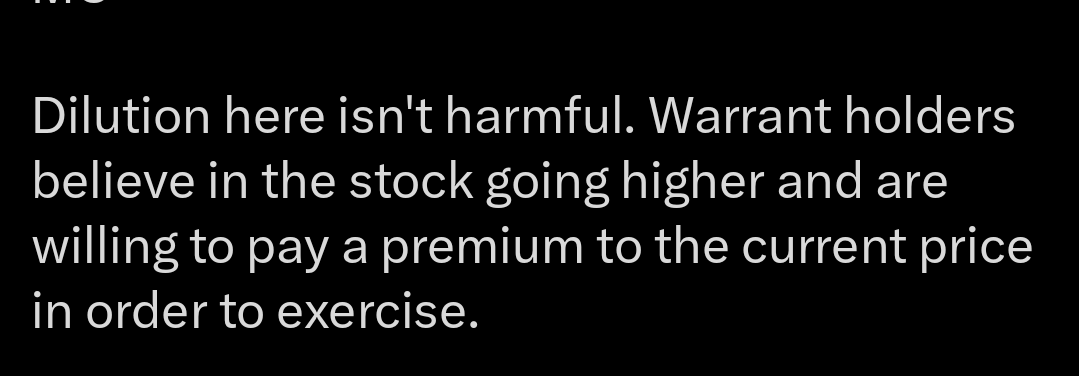

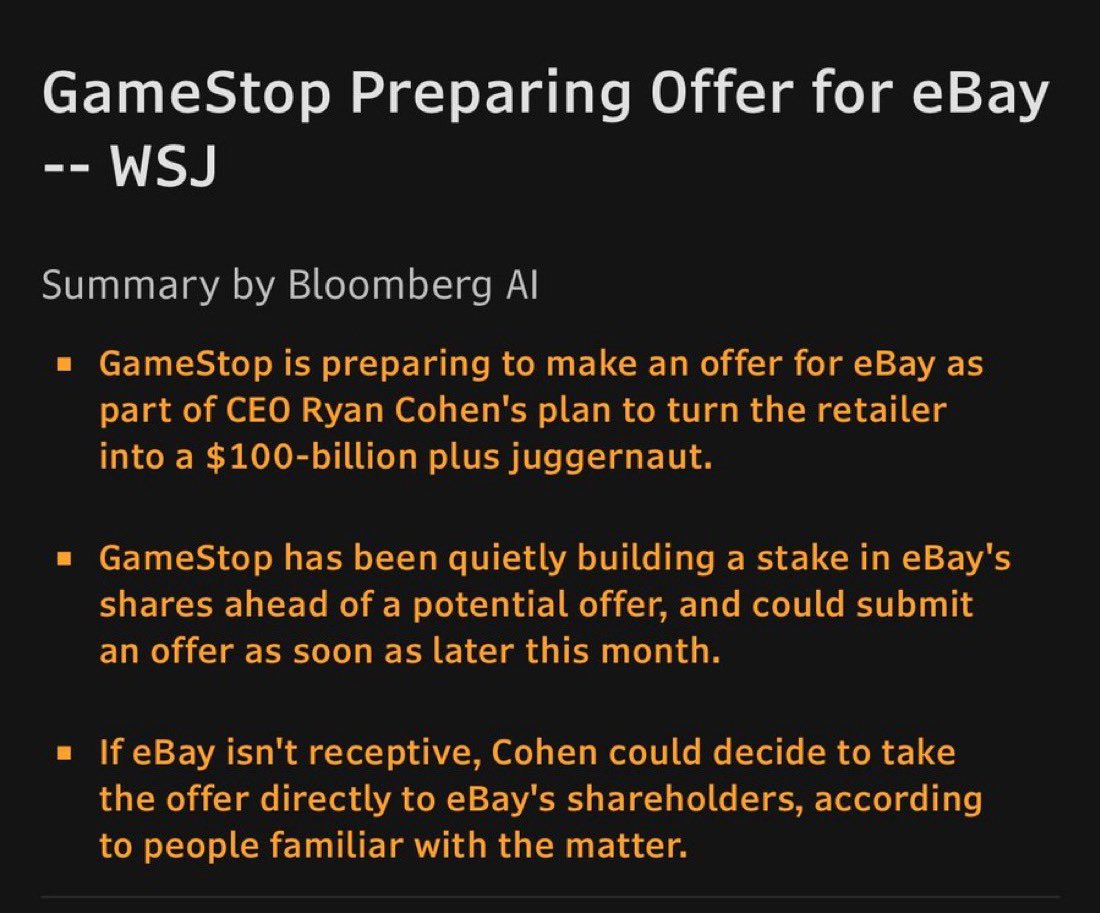

The more I look into the $GME deal... it's 100% possible. Ryan Cohen might be able to pull this off. If $GME price explodes above key levels they will be able to raise billions in cash, clear all their debt, and grow their market cap enough to make the buyout possible. Key Levels & Instruments: 1. $32 - GameStop Warrants ($GME.WS) 2. $38 - Convertible Notes (Zero Coupon) 3. $50 - Ryan Cohen Pay Package 1. 59.15M $GME October Warrants become exercisable above $32. If all warrants are exercised they raise $1.9B USD while share count grows from 448M > 510M, or $16.3B MC Dilution here isn't harmful. Warrant holders believe in the stock going higher and are willing to pay a premium to the current price in order to exercise. 2. Two tranches of zero coupon convertible notes were issued to buy $BTC. The convert and expiry is split between 2030 & 2032. These notes are economically in the money above $29-30, which is their convert. 2032 Notes convert: $28.91 2030 Notes convert: $29.85 Conversion is contingent on multiple specific stipulations (Note - this is extremely important later). Note holders can't convert to shares until $GME trades above 130% of the conversion price for 20 of 30 consecutive trading days in the prior quarter. Our trigger prices... 2032 Notes trigger: $37.58 2030 Notes trigger: $38.81 If we hold above $39 and these notes convert to shares, $4.2B in convertible debt is wiped from the balance sheet. Share count would grow 510M > 653M pushing the market cap of $GME to $25B+. $GME would be $25B with ~$11B cash on hand with zero debt... all the sudden buying $EBAY at $45B is possible. 3. Ryan Cohen's Historic $35B Pay Package will become official with a vote in June. The top milestones include $100B market cap and $10B EBITDA for $GME where he would vest 171.5M stock options @ $20.66 strike. Assuming $GME takes over $EBAY he could hit $50-70B market cap and ~$3B of EBITDA year one. If Ryan were to vest all of his shares before an ebay deal (very unlikely) it would add $3.54B in cash and bring the fully diluted share count to 825M ($41B+ MC). Now that you understand the instruments, let's take a step back to understand their plan. Why did they structure it this way...? In my opinion they are designing a squeeze on delta neutral bondholders. Bondholders are in a very unique spot. Once $GME is in the $32-$37 price range they are forced to add short positions to stay delta neutral even if they are below their trigger event. On issuance 65M-80M shares were shorted @ $22 by bondholders to go delta neutral on their positions. If GME is above $32, the $4.2B would need to short approximately 115M-125M total shares ($3.68B) in order to stay delta neutral. The shorts would need to 2x very quickly. Borrowing costs would skyrocket, available shares would disappear, and eventually bondholders will likely struggle to cover their positions as they tread water for 3+ months while their stipulations for exercise were satisfied. Here is where it gets interesting... in order for these books to stay delta neutral they arent just shorting the delta of $GME shares, they also need to short the delta of $GME warrants... which are massively deflationary as they are being exercised. In the $32-40 range for $GME they would be required to short 11-14M $GME+ Warrants of the 59M total available, its extremely reflexive. Quick reminder these bonds expire in 2030 & 2032, they could be forced to short with massive borrow rates for months or even years on both shares & warrants. $32+ warrants will vest, gamma will skyrocket, borrow fees jump on both assets, bondholders will rush to hedge delta, and eventually they run out of warrant supply to cover their positions. 14M of 59M Warrants are already held by Convertible Note holders today as a hedge, what happens if prices spike above $32 quickly? There wont be enough supply to hedge and the full squeeze begins. There are multiple angles here where $GME grows their market cap to $16-32B, grows their cash by billions, and can complete the takeover. As reported by WSJ, it's also extremely likely that they have already accumulated a stealth position in $EBAY. There is a decent chance $GME already owns ~3-5% of $EBAY through share and options purchases. I love the upside here... long $GME shares & warrants. Power to the Players! 🎮 (All Data and Probabilities for Thesis Were Built by Axion AI - axion.eternis.ai/invited/SCS)

The $GME rumor to buyout $EBAY is as real as the toothfairy...

$GME and $EBAY. Makes perfect sense.