Sabitlenmiş Tweet

Quantillion Atlas — daily digest

🟡 Holding pattern: markets await Nvidia catalyst while geopolitical crosscurrents persist

Today's macro pulse: Equities ground higher into the Nvidia earnings print as bond yields paused near cycle highs and Iran diplomacy hints tempered energy-led inflation fears.

• Stocks grind up pre-Nvidia, bonds stabilize. US equities advanced with Nvidia leading ahead of tonight's results — the single most-watched earnings event this quarter. Bond yields paused after a multi-day sell-off but remain near recent highs, keeping risk sentiment on a short leash.

source: investing

• Iran talks in "final stages" — oil and gas ease. Trump signaled US-Iran negotiations are approaching conclusion, prompting crude to slip as tankers resumed transit through the Strait of Hormuz. European natural gas prices also retreated on reduced supply-disruption premium. The UAE's Hormuz bypass pipeline is 50% complete, adding a structural hedge.

source: investing

• ECB June rate hike all but locked in. Sources indicate the ECB has largely settled on a June hike, though July remains an open question. The hawkish tilt reflects persistent core inflation concerns in the eurozone and adds to the global tightening narrative pressuring duration assets.

source: investing

• Dollar near six-week high; gold faces triple headwind. The dollar firmed on rate-hike expectations and residual Iran uncertainty, hovering at a six-week peak. Oil, yields, and the greenback are forming a concurrent headwind for gold, which managed only a marginal uptick despite safe-haven demand.

source: investing

• Indian rupee hits record low; RBI mobilizes $5B swap. USD/INR pushed toward 97 as the oil price shock cascaded through India's current account. The RBI responded with a planned $5 billion FX swap auction to inject rupee liquidity — a signal of acute EM stress from the energy-rate nexus.

source: investing

• Semiconductor names surge ahead of Nvidia print. Lattice Semiconductor and KLA both posted sharp gains, riding pre-earnings momentum across the chip complex. AI-adjacent capex narratives remain the primary bid driver, with convertible bond issuance from AI-linked firms also surging.

source: investing

Summary

Markets are in a classic pre-catalyst consolidation: equities lean constructive on Nvidia optimism and Iran de-escalation hopes, but elevated bond yields and a strong dollar keep the risk surface mixed 🟡. Tonight's Nvidia print will likely determine short-term directional conviction.

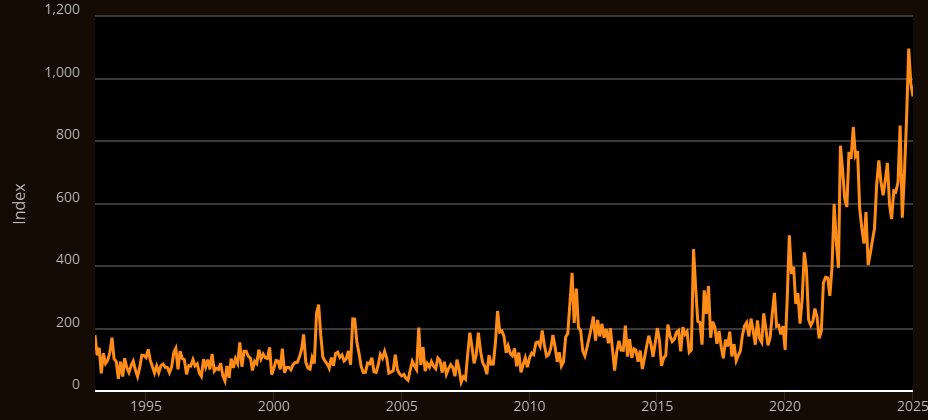

Quantillion Atlas — Researched Return (since inception, Jul 01, 2010 to May 19, 2026, 15.9 years)

Return: +2842.94%

Return YTD: +1.32%

1Y Return: +18.67%

3Y Return: +72.55%

CAGR (since 2010): 23.73%

Sharpe: +2.44

Volatility: 6.09%

Max Drawdown: 7.79%

See attached chart for performance details.

This post is part of Quantillion Research output and does not constitute investment advice or promotional material.

#Quantillion #Atlas #MarketSentiment #QuantResearch #MacroPulse #Nvidia #IranTalks #BondYields

English