AlwaysLearn

38 posts

Everyone’s asking what to buy in 2026.

The answer’s been in the executive orders the whole time.

The reshoring of America is real. And it starts with the ground-level stuff nobody talks about.

Critical Minerals: $MP $LAC $TMQ

Rare Earths: $CRML $USAR $TMC

Manufacturing: $STRL $CDNL

You can’t build the future without the raw materials first.

Then comes the energy layer — because AI, drones, and chips all need power.

Nuclear: $OKLO $CCJ $UUUU $XE

Energy: $GEV $BE $TE $FCEL

Batteries: $AMPX $QS $FLNC

Now you’re cooking. Stack the infrastructure, then deploy the technology.

Photonics: $CRDO $LITE $AAOI $AXTI

Chips: $NVDA $AMD $TSMC $ARM $INTC

AI: $MU $DELL $WDC $SNDK

The applications sitting on top of all of it?

Space: $ASTS $RKLB $PL

Drones: $ONDS $UMAC $AVEX

Robotics: $AEVA $OUST

Quantum: $IONQ $RGTI $QBTS $INFQ

Healthcare: $OSCR $CLOV $NVO

Crypto: $CRCL $HOOD $PURR

This isn’t a stock list.

It’s a supply chain.

Read the policy. Follow the capital. Connect the dots.

Not financial advice. DYOR.

Bookmark this post , like and repost so it can help others.

English

@InvestmentGuru_ do you think its a better buy than $nok this year

English

Leopold Aschenbrenner disclosed ownership of 12.4M Class A shares of $NBIS

English

@rjcurious66 Both has same potential from this price , both can be double but NOK might have edge over BB in short term

English

Two legacy mobile giants flying under the radar — $NOK & $BB

The market wrote them off. The story is changing.

$NOK

→ Repositioned as an AI & optical networking infrastructure company

→ Optical Networks grew 17% in Q4 — driven by AI & cloud hyperscaler demand, with book-to-bill above 1

→ 9 of the top 10 global hyperscalers use Nokia’s optical networks

→ $1B NVIDIA partnership integrating AI-native 5G-Advanced and 6G RAN architecture — field trials expected in 2026

→ Reorganized into a dedicated Network Infrastructure growth segment to capture the AI & data center buildout supercycle

→ Board authorized repurchase of up to 550M shares — capital return signal

→ Long-term OP target of €2.7–3.2B by 2028 — re-rating potential if optical keeps compounding

NOK is a slow-burn AI infrastructure play hiding in plain sight. Optical + IP networks are the pipes the AI supercycle runs through.

$BB

→ Hardware is dead. The software pivot is very much alive.

→ Q4 earnings beat: $0.06 adjusted EPS vs $0.04 consensus, $156M revenue vs $144.6M expected

→ QNX hit record revenue — up 20% YoY in Q4 and 14% for the full year — $950M royalty backlog

→ QNX embedded in 275M+ vehicles — works with all 10 top automakers and 24 of the top 25 EV makers

→ NVIDIA collaboration integrates QNX OS for Safety 8.0 with IGX Thor — plugging BB into physical AI across robotics, medical, and industrial

→ Defense wins stacking: TKMS naval deal, SecuSUITE naval integration, Secure Communications back in growth

→ AtHoc platform just secured FedRAMP High re-certification 🏛️ — the highest bar for US federal cloud security

→ Directly aligned with Washington’s growing investment in mission-critical emergency notification and crisis coordination

→ Positions BB as a trusted vendor for federal agencies and critical infrastructure at exactly the right moment

→ 76% gross margin — pure software story, no hardware drag

→ FY27 guidance: mid-to-low double-digit revenue growth + ~$100M operating cash flow

→ Stock hit a 4-year high on back-to-back sessions this week 📈

BB is stacking catalysts across EVs 🚗, AI 🤖, defense 🛡️ and now federal government 🏛️ — four of the hottest spending themes in the market right now.

Both $NOK and $BB were left for dead when smartphones took over. Both quietly rebuilt around software and AI infrastructure. Both now have genuine catalysts heading into H2 2026.

The mobile era ended for them. The AI era may just be beginning.

Not financial advice.

English

@Tanr45 @Sergeant991 why do you think they will sign Verizon or ATT

English

@Sergeant991 Conservatively $20 EOY.

If they sign a T-mobile, Verizon, AT&T for there AI towers, $30-40

English

I’m glad I doubled down on this $NOK position, I originally had 300 shares and soon added another 300 when it attempted breakout No 3.

Now I’m regretting not buying 1000 shares!

Hindsight is a real killer. 😂

English

@aleabitoreddit @aleabitoreddit have you looked at $nok which has photonics revenue stream completely ignored

English

It's highly nuanced, and I'll explain why it's not late, but late to some:

Photonics is the newest supercycle (maybe H1 into H2 2025 was the start).

Then there's many different architectural changes in each supercycle:

-> $LITE, $COHR, Innolight, $AXTI and these names led the first

I did a thesis post on mentioning all four of them as the largest beneficiaries (all are up 500-1000% 1Y)

-> $AAOI, $JBL and others types of names are benefit immensely as the transitional bridge (eg. 1.6T pluggable)

-> $SIVE, Celestial, Ayar, $POET are others future gens eg. CPO (what I'm focusing on now)

-> VisEra, QD Laser, $ALMU and others are likely going to be future gens (quantum dot, different packaging types, etc) if you fast forward 4 years.

Of course, $LITE does everything. $AXTI will be used for everything.

But the amount of pure play exposure for each architectural shift in each mini supercycle is different.

For example, inp usage with quantum dot is still there, but less used. Or DFB laser arrays for CPO instead of EML.

There's probably still 50%+ with $LITE and $COHR. And you're a little on the "late" side of things.

But you're extremely early to new architecture generations.

What I'm trying to do is point regular retail investors into the direction of new gold mines for free.

Before institutions figure out sooner or later by paying $20k for equity research reports.

Rabbit@rabbitrun97o

@aleabitoreddit Missed the opportunity to make money by investing in photonics. Do you think there is 50% upside from here?

English

10 Under-the-Radar Tech & Semiconductor Names Worth Watching

$HIMX — Taiwanese fabless semi leader in display driver ICs + automotive displays. IBM partnership in play. Q1 earnings May 7. Stock up 36%+ from March lows. WiseEye ultralow-power AI sensing = hidden edge AI angle.

$TRT — Trio-Tech. Revenue up 82% YoY in Q2 FY2026, led by AI chip final testing services (+113% segment growth). $5.3M burn-in board order for next-gen AI GPU platform. $2.5M automotive IDM burn-in contract ramping through 2026. Tiny cap, massive AI testing exposure.

$SHMD — Schmid Group. German advanced PCB + semiconductor packaging equipment maker. Secured major order for wet-process equipment supporting AI & HPC infrastructure. Delivered first InfinityLine H+ panel-level packaging system to a leading U.S. tech company. high risk

$OPTX — Syntec Optics. Vertically integrated U.S. optics manufacturer. $2M AI-powered AR camera order for U.S. warfighters. $4M+ in defense orders in March. LEO satellite optics ramping — on track to nearly triple 2026 deliveries. NDAA domestic sourcing mandates = structural tailwind. Stock up 7x in 1 year.

$QUIK — QuickLogic. Radiation-hardened FPGA play. $89M SRH FPGA prime contract ceiling. $13M contract tranche secured. New eFPGA design win on 12nm data center ASIC. Defense + commercial dual-track revenue building. Underowned, underknown.

$NOK — Nokia. Q1 2026: revenue +4%, operating margin expanded 200bps, free cash flow €629M. Optical Networks booming on 800G demand, €1B in new orders. Infinera acquisition synergies flowing. AI + cloud infrastructure = Nokia’s second act.

$ALMU — Aeluma. III-V-on-silicon photonics platform. NASA award for quantum dot laser platform. $4M+ in U.S. government contracts in April alone. Targeting AI interconnects, defense sensing, quantum & AR/VR. Revenue inflection expected 2027-2028. Tower Semi + Sumitomo as foundry partners. Early-stage, high-conviction speculative.

$LPTH — LightPath Technologies. Vertically integrated IR optics + camera systems. Black Diamond glass + G5 Infrared acquisition. 2026 NDAA beneficiary — domestic infrared optics sourcing mandate. Up 473% since 2018. Defense sensing and thermal imaging long-term compounder.

$OSS — One Stop Systems. Rugged GPU-accelerated edge compute for defense. 20-25% revenue growth guidance for 2026. $10.5M in new U.S. Navy + defense contractor awards. P-8A Poseidon lifetime revenue now $65M+. Returned to profitability in 2025. AI-on-the-battlefield is the entire thesis.

$LPKFF — LPKF Laser & Electronics. German laser systems maker for PCB prototyping, semiconductor packaging, plastic welding & solar. OTC-listed. Revenue ~$135M TTM. Stock up ~95% from 52-week lows. Warburg Research maintains Buy rating.  Earnings Apr 30. Morningstar fair value estimate $59 vs current ~$15 — significant implied upside if demand recovers. Niche but critical in advanced electronics manufacturing.

defense tech, AI sensing, optical systems, laser manufacturing, and rugged compute — the hardware layer of next-gen warfare and AI infrastructure. Not the flashy names. The picks and shovels for the decade ahead.

Not financial advice.

English

@rjcurious66 @aleabitoreddit If you use a brokerage with international access like $IBKR

English

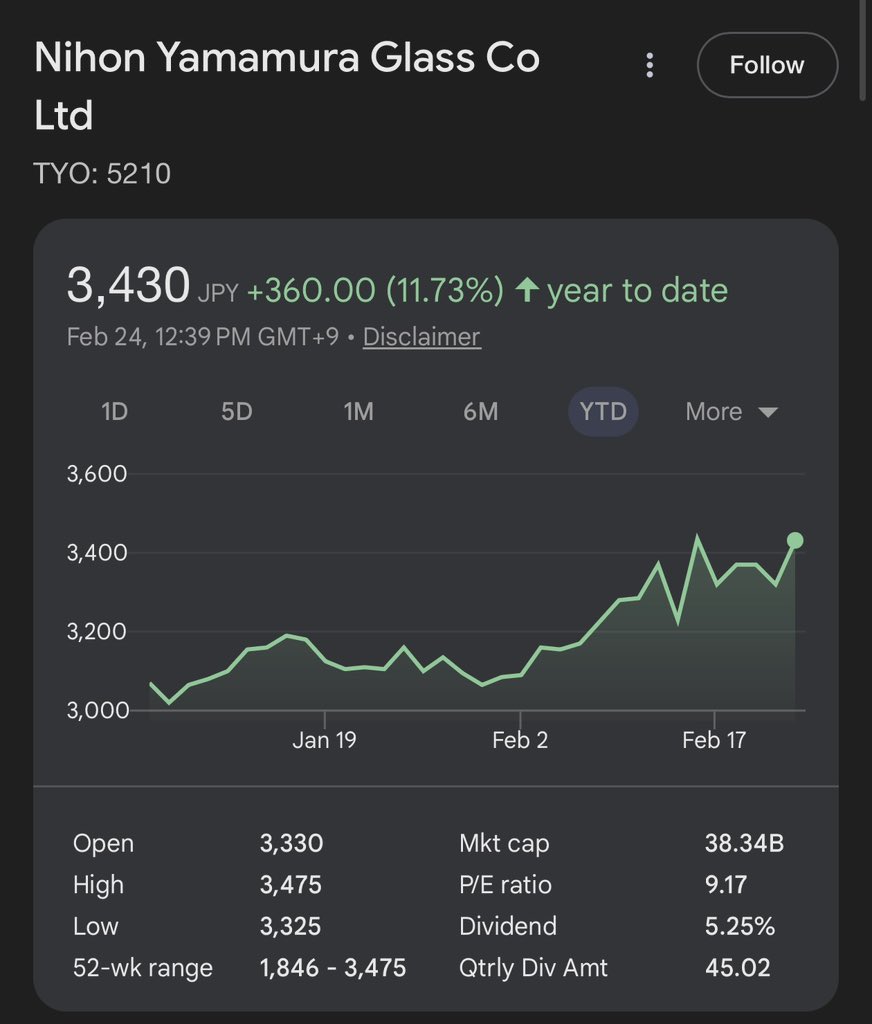

Took a closer look: Yamamura glass (TYO: 5210) is a banger.

You’re basically buying the business for free?

And their photonics division is growing 91% Y/Y for optical communication caps.

You are paying $240M for a company that does $500M sales with $360M+ in actual book value (factories, equipment, cash) and a fast growing AI DC photonics division.

Before this was a trap but

-> they upped dividend amount to 5.5%, which is the biggest signal that value is now unlocked. And now from their Feb 12th earnings, they confirmed this was structural (not just one off that markets were fearing)

It’s just wait and chill basically?

kjnk@kjnkjp

Yamamura Glass - $220mn mcap (0.6x PB, 11x PE) Japan's largest 'glass bottle' manufacturer with 110yr history, and also produces plastic caps, applied that technology to photonics--has a subsidiary that produces "optical package caps" used for fiber-optic communication in DCs.

English

@OngJunJieOJJ Yeah, this not even including their other growing divisions lol

English

Deloitte’s semiconductor outlook reports that GenAI chips are driving 50% of the forecasted $975B revenue in annual sales in 2026, despite making up only 0.2% of total unit volume.

Wild 250:1 revenue-to-volume ratio

Massive value concentration in AI

$MU $EWY $SNDK $TSM $NVDA

Trade Whisperer@TradexWhisperer

$MU: $75B Market Cap, $8.1B revenue last qtr $AMD: $138B Market Cap, $7.8B revenue last qtr $PLTR: $213B Market Cap, $0.8B revenue last qtr You can't undo what you've seen. Micron is the Bargain of the Century.

English

@InvestorOfJAMMU if someone invested in 2010, he finally can sell share without loss in 2024

English

If someone invested 1 Cr in Vedanta at 40/share in April 2020, he is getting 1 Cr as dividend every year including capital appreciation of 1350%.

Power of Dividends🔥🔥

English

@AlvaroMysterio you sold 50 % NBIS right.. are you still with cash or bought NBIS again

English

These calls have definitely helped! I am up over +3786% and I am not selling! $NBIS

Not gonna sell till we are $120 in a few weeks. I also have some nice LEAPS that I will hold until $200.

And obviously I own tons of the underlying stock which I am not selling for MANY, MANY years (Hopefully over 10 years)!

George Koutalidis@geokoutalidis

1-Year Performance of my Main Portfolio Getting closer to 1000%! Main Portfolio 1 Year Return: +821.24% VS +19.6% for the $SPX

English