Rob!n retweetledi

$SNAP and $QCOM signed a multi-year deal to power future Specs eyewear with Snapdragon XR chips.

Snap says the standalone AR glasses launch later this year with a focus on on-device AI, graphics and shared experiences.

English

Rob!n

4.6K posts

@ro_rademaker

Technology focused investor ~ Ideas not financial advice ~ Put in the work ~ Ask the right questions

Nvidia’s market cap has now increased by more than $2.15 trillion since Michael Burry began shorting the stock.

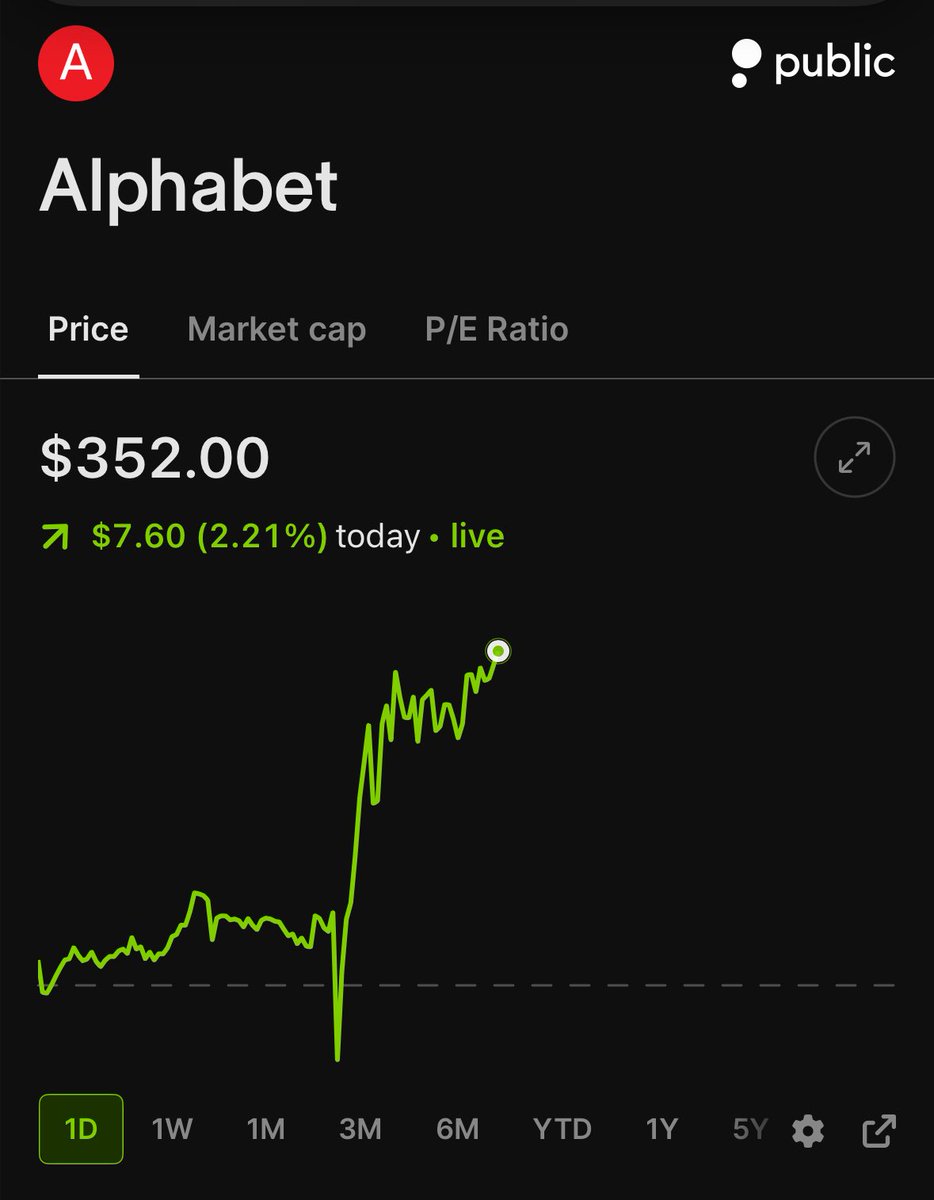

Does anyone know why Qualcomm is up?