rob

132 posts

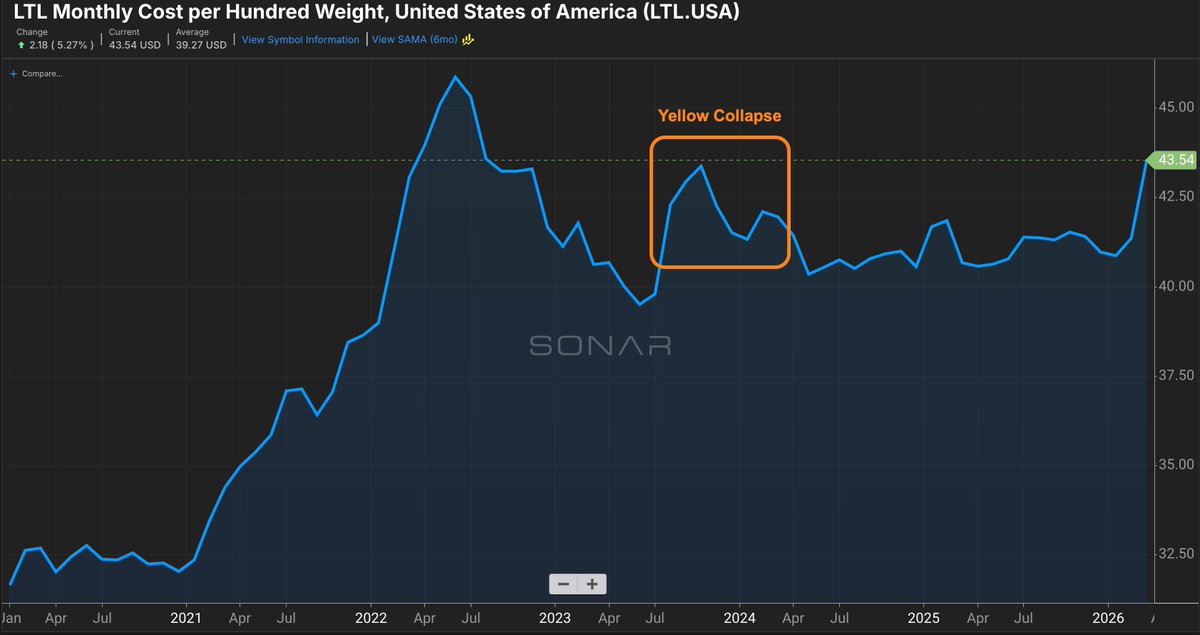

Brand SONAR new dataset:

National average rate for LTL.

LTL carriers finally gaining pricing power.

English

Timeline:

1. MVBs

2. Start of Production

3. Employee "Customer" Deliveries

4. External Customer Deliveries

Chris Hilbert@Hilbe

LFG 👀

English

If current van trucking spot rate momentum continues to surge, trucking spot rates could surpass COVID rates by mid-April.

English

What generally happens is that small carriers who aren't on contractual fuel surcharge programs have difficulty negotiating for the full amount of the diesel increase which eats into their allocation for 'linehaul'.

On the demand side, we've certainly seen things soften a bit from the weeks following the storms. Capacity is at or slightly below equilibrium which means things stay stuck at their current levels.

English

the SONAR site implies NTI includes fuel but VCRPM1.USA seems to have no fuel. are you comparing like for like?

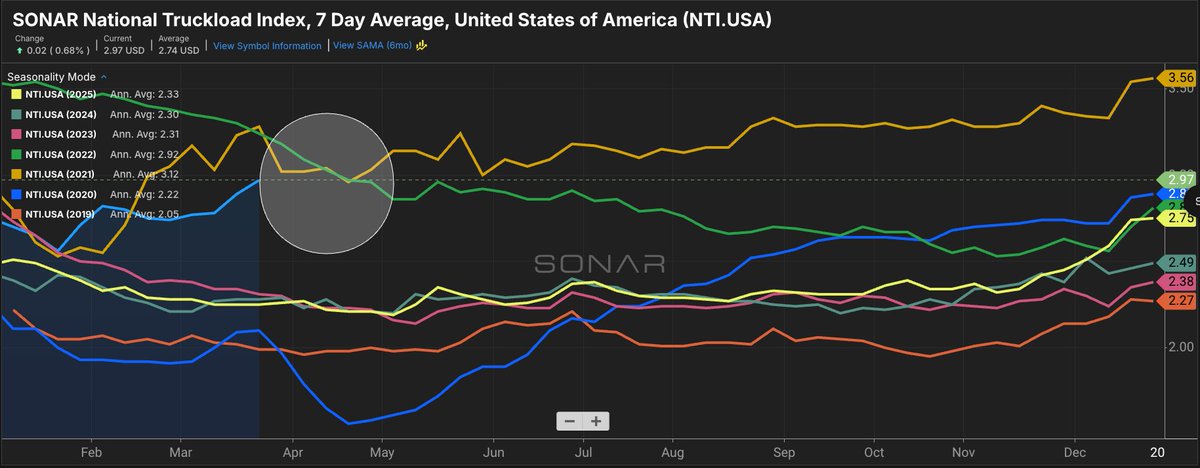

NTI.USA – A 7-day moving avg

NTIL.USA – A 7-day moving avg of the daily spot rate less the estimated cost of fuel. Fuel costs are based on the avg retail price of diesel fuel and fuel efficiency of 6.5 miles per gallon.

English

Spot rates holding near cycle highs, while contract rates are moving up.

Overtime, these two data points should converge....

Note: this is a different index than rates which accounts for fuel surcharges.

In this index, neither has fuel calculated.

English

@REGIONRAT @ThomasWasson Good to hear. With spot up this much I thought would see a squeeze

English

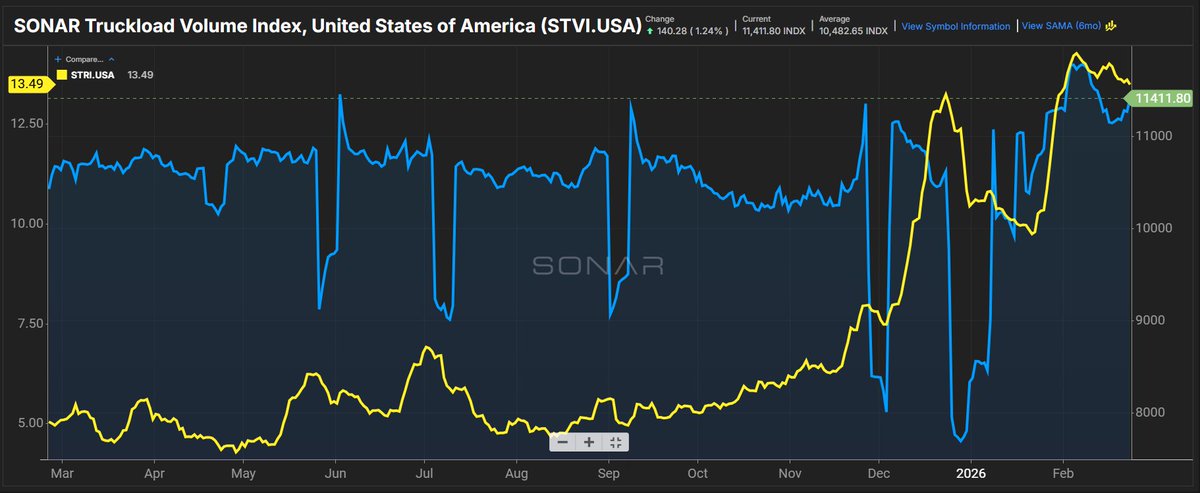

1/ Mid-February truckload snapshot: Outbound tender rejection rates eased slightly last week… but volumes stayed elevated and rejections remain “higher for longer.”

STRI fell 52 basis points week-over-week to 13.49%.

STVI rose 2.3% to 11,411.8 points. Thread 👇

English

@thefreightnerd you need to show the annual seasonality chart for this to have any relevance

English

Total load posts continue to regress back to the long-term daily average. I was especially surprised by how slow it was this past Friday with an impending weather event (or domestic manufacturing renaissance as the kids call it nowadays) about to hit the Northeast.

English

@FreightAlley the brokers that thought December-Early Feb was the new normal (and didn't come close to honoring their commitments) are rightfully being fired by the top shippers. so more immediate business. and ongoing convos about how to grow together for future biz

English

The largest brokers are gaining markeshare as small brokers give back freight to shippers that is underwater.

I’ve had 4+ top 10 3PL CEOs in the past week share stories about how they are winning a lot of business because shippers trust scale, compliance, resources, and balance sheets in this market.

English

@FreightAlley when volumes stop moving, inventories deplete. volumes are still moving.

English

@robbo_wcs The opposite. Inventories need to be rebuilt. Currently at all time lows.

English

Despite experiencing one of the most disruptive winter storms in years and parts of the country still offline due to power outages, freight volumes were up 1% YoY.

This is a very bullish sign for coming weeks, as big weather systems can create shipment backlogs.

English

@christankerfund is it odd to you that ocean rates have come down so much, but ocean charter rates have held really strong? it seems these would need to converge at some point in the future?

English

HARPEX steady for another week as container charter rates remain close to +3 year highs…

$DAC $ZIM $CMRE $GSL $ESEA $NMM

English

@Sunshiny808 @maziehirono how do you know Matson is raising shipping rates?

English

@maziehirono In Hawaii, Matson will be raising shipping rates 25%…

What does Mazie say about it?

Trump bad

English

In Trump World, children are going hungry because the President refuses to fund SNAP benefits, even after being ordered to do so by a federal court —

Meanwhile, in that same Trump World, the Department of Homeland Security is funneling over $100 MILLION from DHS ad contracts to firms connected to DHS insiders, and the FBI Director is flying around in a taxpayer-funded private plane to visit his girlfriend, who has FBI agents providing her personal protection services…

In Trump World, this regime spends taxpayer money like it grows on trees, while families go hungry and health care becomes unaffordable.

Trump World is a world where children go hungry while lawlessness and corruption are rewarded. What’s wrong with this picture?

English

Container freight futures curve ended up, with February up 7%

$ZIM $MAERSK

English

$ZIM Den of Thieves

$ZIM ’s board and management have betrayed shareholders.

$24 cash/share, $50+ in assets, trading at $15 and they blow capital buying ships instead of returning it.

This isn’t strategy; it’s value destruction.

They should be selling ships at current market highs, not empire-building at shareholders’ expense.

Enough is enough - shareholders demand immediate answers, a forensic review, and the removal of Eli Glikman and any executive prioritizing self-interest over shareholder value.

From discussions I’ve had over the past few days with institutional investors, it’s clear that the recent fund buyers will also support action against the crooks. Everyone knows what’s happening inside $ZIM and where the stock should be if shareholder interests came first.

English

@ThomasWasson7 is it possible we are just seeing a delay in the normal seasonality, per the tender rejection chart?

English

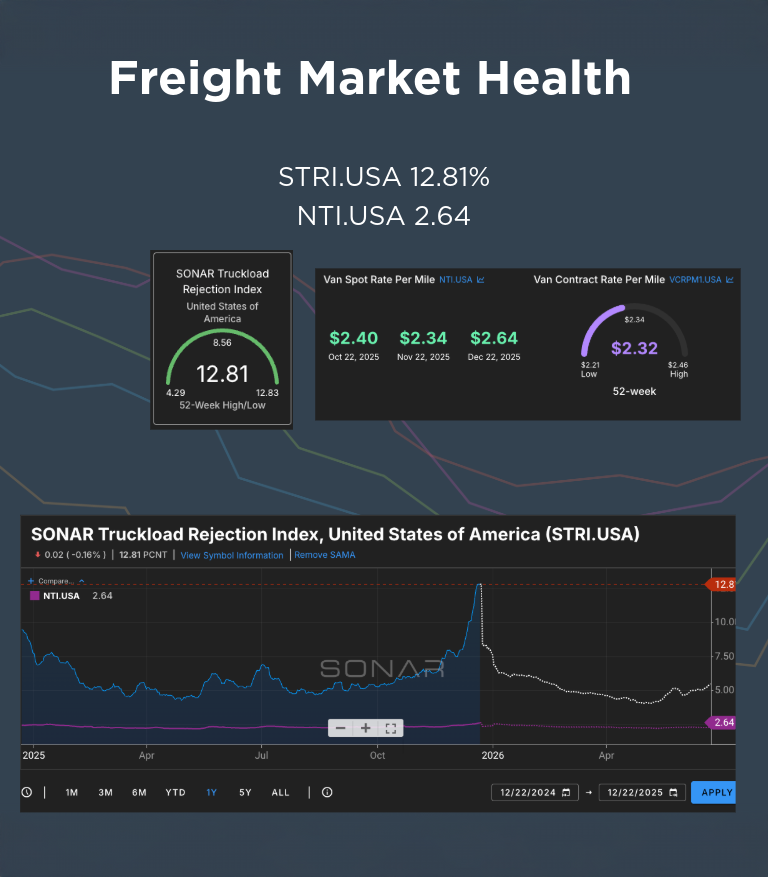

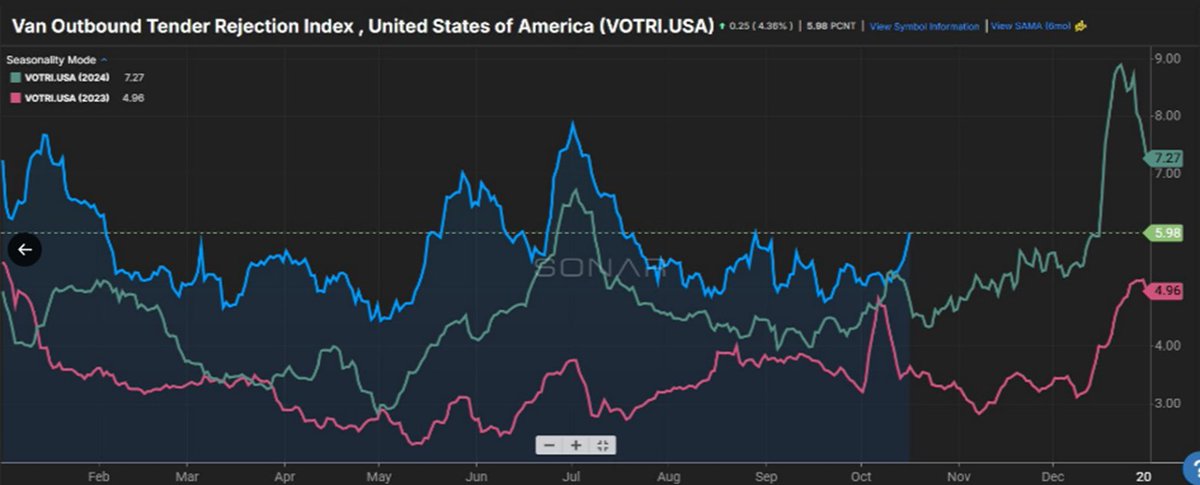

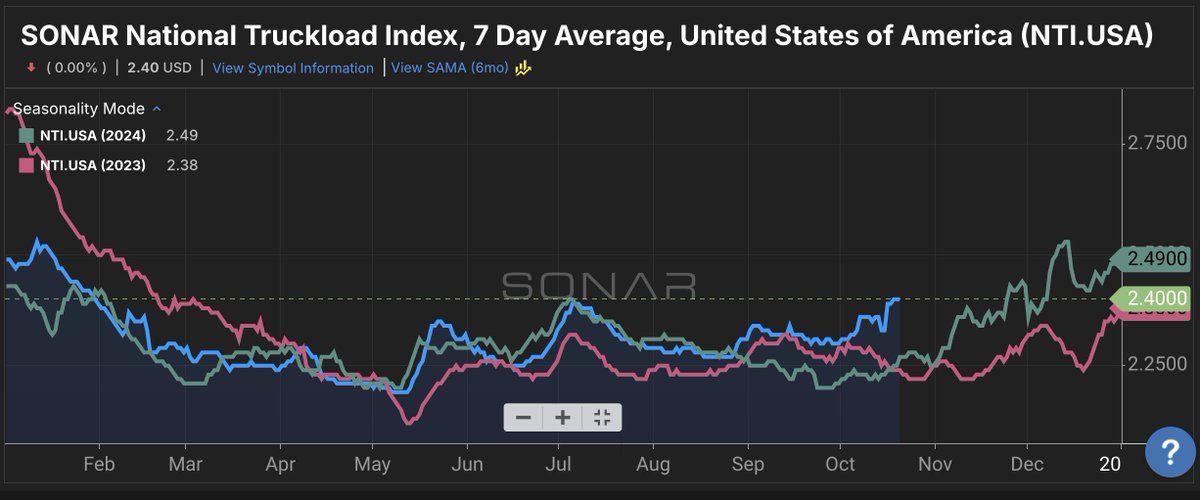

A rally in dry van spot rates continues as concerns over truckload capacity push rates to levels not seen since late January. The SONAR National Truckload Index 7-Day Average rose 4 cents per mile week over week from $2.36 on Oct. 13 to $2.40 all-in. This is the highest rate since Jan. 30. The NTI is now 13 cents per mile higher than $2.27 in 2024 and 16 cents per mile higher than $2.24 in 2023.

Dry van outbound tender rejection rates also saw week-over-week improvements. VOTRI rose 36 basis points from 5.40% to 5.76%. Compared to the previous two years, VOTRI is 123 basis points higher than 4.53% in 2024 and 221 basis points higher than 3.55% in 2023.

A challenge for peak season predictions remains that truckload capacity continues to decline in tandem with declining truckload demand via lower outbound tender volumes. This creates the potential for greater market volatility, especially in the more volatile spot market space.

One sign that current rates are outside of seasonal expectations comes from the SONAR seasonally adjusted moving average (SAMA) feature, which projects a rapid drop in spot market rates before a steady stair-step improvement through late November into late December. At this time it appears that spot market rates should continue to rise in the next week based on the daily movement in the National Truckload Index, which feeds the NTI 7-Day Average.

English

Dominic LeBlanc says after a detailed conversation between PM Carney and President Trump, officials have been directed to reach a deal quickly to bring more certainty to sectors hit hard by tariffs, steel, aluminum, and the energy sector.

English