Foudres@xFoudres

Case study about crypto startups : a long journey towards product-market fit

The harsh reality is that most startups are doomed to fail. Research shows that nearly 90% of startups don’t survive, and they are failing within five years. The reasons are often the same—lack of funding, inability to achieve product-market fit, or mismanagement. In the crypto space, the stakes are even higher as volatile markets, limited resources, and the rapid pace of innovation make the odds of success even slimmer.

Hatom Labs is no exception. Operating within a nascent ecosystem comes with its own set of challenges, and the team faced significant obstacles that could derail most projects. Through calculated strategies, diligent risk management, and a focus on innovation, the team has worked to overcome these barriers and progress toward building a sustainable and impactful presence in the DeFi ecosystem.

This case study explores the challenges Hatom faced, the critical decisions that shaped its trajectory, and the lessons learned along the way. It provides a detailed look at how the misperceived limits of an ecosystem are just another obstacle to overcome, not an inevitability, delivering insights into the strategic thinking and resilience required to succeed in this highly competitive field.

____________________________________

Last April, I was asked to carry out an analysis of the Hatom Protocol. I've been closely following its evolution, and monitoring what's been happening since the protocol was launched, knowing the importance of such a central piece of the DeFi that was being built.

With the incomplete information available to me at the time, this analysis highlighted certain positions that I considered risky, but which were actually under control and now completely sound. However, the player who entrusted me with this analysis seems intent on using it to his own strategic advantage, what began as a search for transparency, turned into a goal to damage the project to benefit their own planned protocols.

This analysis was intended to remain totally confidential, unless I decided to make it public on my own, which I have decided to do today to avoid any appropriation of my work without my agreement, for a purpose that was not the original one.

Also, as with all on-chain analysis, the devil is in the detail, over-interpretation and bias can happen very quickly, even more so when someone, already biased, influences you indirectly in his direction. It's therefore as important for me to rectify it as it is to publish what happened back then from a transparency point of view. My opinion as presented inside this analysis is no longer at all in line with what I think today, especially after having been able to understand the problem from the outside and the inside.

Here's a summary of the events which I believe accurate and which will give the exact picture about everything:

Hatom started its development in 2022 with its own funds and then raised $2 million in equity to bring the protocol from a simple proof of concept to mainnet release. In order to meet the needs of the ecosystem and find a model that could work and achieve a product market fit in a sustainable way, they chose to also build a Liquid Staking protocol, as well as an indexer and price oracles similar to TheGraph & Chainlink in order to make the protocol as secure as possible.

A further $6 million were raised through private and public sales, which were in reality reduced to $4.1 million after the expenses linked to the bootstrap of the protocol itself and its launchpad (KYC expenses, CEX Listings, first batch of protocol incentive, marketing, etc) as well as taking into account the drop in EGLD price from July to October.

Knowing that the team had spent around $2 million on various protocol audits and legal frameworks, needed to incentivize the first year of the protocol to the tune of $3 million USDC before achieving sustainability and product-market fit, and had to bear a cash burn of approximately $200k per month for team payments and infrastructure maintenance for over a year, they found themselves in a challenging position. Compounding these pressures with a token that underperformed, remaining relatively stable around the initial raise price, only a few months after the launchpad the team found itself up against the wall and had to make a difficult decision.

Hatom had the option to simply launch their protocols without incentives after their fundraising, preserving their treasury intact, but instead, they chose to bootstrap DeFi and go all-in.

At the end two choices were open to them :

- Start selling tokens very early in the platform's development and enter survival mode, reduce future investments and incentives, open themselves up to a total devaluation of the token with the first vesting that was about to be unlocked, which would have sent them into a downward spiral and perhaps start blaming the lack of funding and liquidity in our ecosystem as an excuse for their failure.

- Being bold, take measured risks, go all in as founders, innovate to make the token really attractive and sound, invest more into the protocol to attract liquidity from other ecosystems, and ultimately leverage part of their HTM treasury through the protocol itself as a buffer to drive the potential growth that these new technical investments could bring, rather than selling and reducing their future growth potential.

Fortunately, they never opted for the easier path. Instead, they consistently pushed themselves to tackle every challenge head-on, ultimately deciding to pursue the more ambitious and impactful option.

Now that we have the background to this decision, let's look at a condensed version to draw the most important conclusions of the data analysis I carried out in April, when I had no idea of the near-critical situation Hatom was facing, which is affecting so many start-ups in this industry. (All the following assertions will be backed by data available at the end of this thread)

A little before the arrival of the booster, Hatom took advantage of their sEGLD bag from the launchpad fundraise to take loans initially in EGLD, so as not to impact stable liquidity, which was relatively low.

With the arrival of the booster, they wanted to put the HTM price on the right track and eliminate the selling pressure since the launch of the protocol, so they decided to use parts of their treasury to buy back HTM, with the effect of converting their collateral form sEGLD to HTM collateral to secure their loans. But the surge in EGLD in December (while HTM had already reached its ATH in EGLD and was starting to slow down), forced the team to convert the debt into stablecoin to avoid any situation that could become dangerous.

After this migration, their utilization factors returned to healthier values of between 30% and 50%.

With the development of the TAO Bridge, the team began to migrate their collateral from HTM to the treasuries they had built up in TAO to take full advantage of the growth of this ecosystem and the liquid staking opportunities offered by their own protocol. This allowed them to completely secure their (approximately) $4 millions dollars loan in Stablecoin with a strong and liquid asset, with $4 million dollars in TAO, although HTMs continued to be used to maintain a healthy borrowing factor.

As we've seen, the market in May was starting to seriously sputter, and it was at this point that I contacted the team to discuss the situation, understand their motivations, and make sure that I wasn't missing any data in the analysis I'd just handed in to its commissioner my initial conclusion.

What I didn't know at the time was that the situation was already known to the MvX Foundation, as the Hatom team had sought their help and made them aware of it. The Hatom team assured me that the Foundation was providing significant assistance on many fronts and doing their utmost to support whenever possible. However, given the market conditions at that time, they were unable to offer the help needed.

Second and most importantly, that the situation was much more under control with a better risk management than I thought and what the partial data showed me.

The Founders of Hatom also had their personal treasury on the protocol, allowing them to pay back the whole of the Loan in the event of a problem. As I said earlier, they were ready to go all in, even if it means repaying the loan out of their own funds.

After discussing the situation at length with Ahmed, it was clear that the team already had plans in place to address the debt. I continued monitoring the protocol and eventually saw that the majority of the debt—approximately 90%—was repaid. Currently, only the interest on the loan remains unpaid, amounting to around $1.4 million with a ~30% utilization rate. The founders still hold their own personal assets, including wTAO worth over $11.5 million, as collateral to secure their overall position on the lending protocol.

If at the time I considered Hatom's weight within the DeFi ecosystem as a risk because of this incomplete vision I had, after having worked closely with them for 5 months now, I think I'm in a position to affirm that I was largely mistaken.

There was, in reality, no substantial risk; the true risk was that the Hatom team put their personal funds on the line to keep the protocol running and thriving.

Hatom has now reached a state of self-sustainability, with a healthy treasury and all previously mentioned challenges firmly behind them.

In their efforts to make their protocols thrive, Hatom also managed to repurchase the entire HTM allocation of their Equity Investor. Every move they make is for the benefit of the ecosystem and to ensure the long-term success of their project.

It was also very revelatory for me, when I confronted the team with what I knew in a rather direct and harsh way, rather than being closed to discussion, they were very open, appreciative of my work and ready to offer me a place on the team to benefit from my expertise on the subject, giving me the chance to monitor everything from the inside and make up my own mind, which says a lot about their intention.

On top of this, I consider it important for everyone to keep in mind that, behind the scenes, the Hatom team is tirelessly working on multiple innovative products, meticulously designing their architecture to address critical gaps in the ecosystem. These developments, while not yet revealed to the community, are another clear reason why I believe their approach will expand the protocol’s reach and solidify its role in the broader DeFi ecosystem for years to come.

Hatom is truly a stellar team, with a passion for building to solve problems that sometimes seem insolvable, and a never-say-die attitude to obstacles, which has enabled them to strive and grow the DeFi ecosystem we know today. The effort accomplished over the last few months has been gigantic, we've already worked on so many things that I couldn't possibly list them all, dozens of research papers, to do better wherever possible, and continue to position ourselves as a major player in DeFi.

There's also a lesson to be learned for builders: your growth isn't inevitably limited to that of your ecosystem. You can, and must, make it grow too. This requires you to be able to think out of the box, to be strategic, but also to be able to capture growth where it is, and bring it back to where you think it most deserves to be.

This is why after multiple back and forth and discussions with the team, I’m proud to announce now officially that I’m part of Syfy, working on both Hatom Labs & Soul Labs as On-chain Analyst & Researcher, and will be working with risk assessment entities drafting strategies together. Many lessons have been learned, and of course, I will always try to maintain my objectivity as much as possible and my research activity on MvX to always push forward this ecosystem !

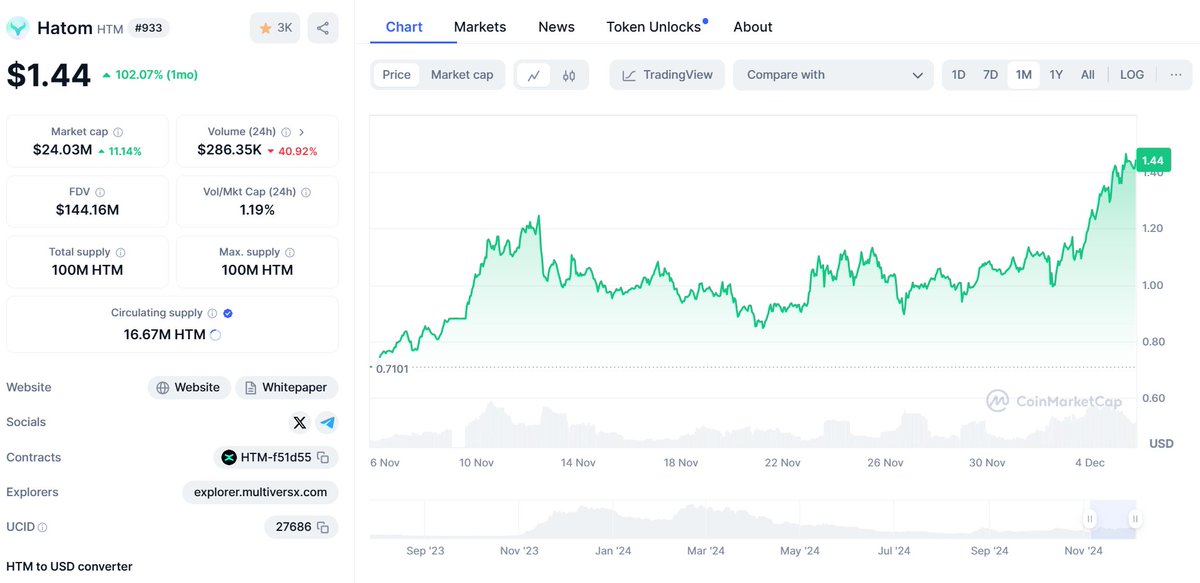

Below, you will find the charts of Hatom's positions in the protocol, the different Collateral and Borrow, the token composition of Collateral and Borrow, as well as the Borrow Utilization Factor from the beginning of the protocol, until the resolution of the above-mentioned events.