Sabitlenmiş Tweet

DD 滴滴

25.7K posts

@rtk17025

Full time BD for @o1_exchange Cofounder of @GMWallet Trade US HK stocks on @StableStock : DDD66 Best debit card @Backpack : backpack6666 Open for collabs 🦅🦅

< StableStock the best platform for stocks trading > 1. Why @StableStock ? Traditional investing in Hong Kong and U.S. stocks presents several common challenges, especially for investors in Asia and emerging markets: High account opening barriers Investors typically need to open accounts with overseas brokers (e.g., Interactive Brokers, Firstrade). The KYC process is strict and time-consuming, often requiring proof of address, tax forms (W-8BEN), and other documents Inconvenient deposits and currency conversion Funding usually requires bank wire transfers or third-party platforms in USD or HKD. This involves high fees, slow processing times, and exchange rate risks. Crypto holders face additional on-ramp/off-ramp steps Limited trading hours U.S. stocks trade only during U.S. Eastern Time (9:30–16:00), and Hong Kong stocks have fixed sessions. This makes it difficult to trade 24/7 or react quickly to after-hours news and event High fees and financing costs Commissions, platform fees, and margin interest can add up significantly, especially for leveraged or high-frequency trading. Overnight financing charges are particularly burdensome. Poor liquidity and integration — Stock holdings are hard to use within DeFi ecosystems (e.g., for staking or yield generation) and difficult to combine seamlessly with stablecoins, resulting in lower capital efficiency. StableStock was created to solve these pain points by allowing users to trade real Hong Kong and U.S. stocks directly using stablecoins (USDT, USDC, etc.). 2. What is StableStock? StableStock is a TraDeFi (Traditional Finance + DeFi) on-chain stock liquidity platform. It tokenizes real Hong Kong and U.S. stocks and in the future it will expands to stocks worldwide like Taiwan Japan Korea and other countries and ETFs on a 1:1 basis into sStock tokens (e.g., sAAPL, sTSLA). The underlying shares are held by licensed brokers, fully verifiable on-chain, and settled directly with stablecoins. Team Background CEO – Zixi Zhu (朱子曦) @ZixiStablestock : Graduate of Nanyang Technological University (Singapore). Former Head of Crypto Investments at Matrix Partners (经纬创投). Also co-founder of 10K Ventures. Brings deep experience in both traditional finance and crypto COO – Zac Lary: Co-founder who works closely with the CEO. The team has strong combined expertise in traditional finance and blockchain. Funding & Traction Completed seed round in 2025, incubated and led by @yzilabs Labs, with participation from MPCi (Matrix Partners) and Vertex Ventures Current metrics: 22,600+ active users, support for 1,900+Hong Kong and U.S. stocks & ETFs, and over $16.7 million in assets under management (AUM). Trading volume continues to grow steadily Key Advantages: Leveraged Spot Trading with Zero Intraday Interest Supports Leveraged Spot trading with up to approximately 10x leverage Zero intraday interest: No financing fees if you open and close positions on the same day — ideal for short-term trading and fee arbitrage Competitive overall trading fees Users can enjoy extra discounts with official top-tier referral codes like DDD66 Idle assets can be deposited into StableVault to earn yield, allowing users to combine stock exposure + DeFi returns These features make StableStock particularly attractive for investors who want low-cost, high-efficiency exposure to global stocks using stablecoins 3. How to Register Step-by-step registration: Go to the official platform: app.stablestock.finance/?join=DDD66 Click “Sign Up” Register with your email and set a password, or connect a supported wallet Enter the official referral code: DDD66 After registration, you can deposit stablecoins (USDT / USDC, etc.) and immediately start trading U.S. and Hong Kong stocks in both spot and leveraged modes The platform offers an intuitive interface and integrates tokenized assets with DeFi features

Bybit最近开始封卡了吗? 最近微信、支付宝、美团都无法使用了😂 我的GPT续费有问题了

这大概是目前最好用的 u卡了 除了中国人友善外,任何事情都能找的到人 无论是chatgpt/claude/codex订阅,不想订阅要退款,或是任何要客製化的服务 售后群 24小时随时都有人替您服务 u卡 用 mp 连结: mp.net/c/DDD66 邀请码 06283937 走Visa 售后群: mp.net/g/mp_kzV0j1

不知道你们有没有发现? 你们的粉丝数量今天掉了一大批 昨天被封创作者收益的大 V 们今天账号甚至直接冻结

Some observations on Kimi: 1. It's a very good model! I don't think its performance can be explained away by distillation or anything like that. In agentic coding sessions, it seems pretty much on par with the best public models of Q1 2026. In my fairly limited use, it also seemed very token hungry. It's not obvious to me that this model is actually that cheap to run. 2. I am personally surprised the Chinese state continues to allow the open sourcing of models this good, given potential risks. To be clear, I *myself* might be fine with models presenting this level of marginal risk being open weight, but I am surprised that China is fine with it. I suspect the reason they are is 75% explained by strategic blindness/lack of AGI-pilledness (the CCP is very Yann Lecun-y in its views of AI). The other 25% or so is their lack of compute for customer inference (making China's open-weight strategy an unintended byproduct of US export controls) and the normal Chinese strategy of aggressive exports. For the companies, as opposed to the government, the decision to open source is partially ideological and partially because they are behind, and they know that very few people would pay for sub-frontier models from China. 3. Open-weight models are inherently decelerationist, and I'm continually surprised to see the so-called "accelerationists" so excited about open-weight models. I suspect the reason they are is that they know open-weight models are effectively ungovernable, and they simply like the overall cloak of ungovernability open-weight models create over the whole of AI. It's not a bad strategy; it reminds me of James Scott's recounting of the hill people in "the art of not being governed." Still, in the end, open-weight models deter further AI capex. 4. One probable outcome of an open-weight-model-dominant world is full AI communism, which is precisely what China proposes: rather than a market product, AI is a "public good" which will ultimately be provided by the state as a kind of "digital public infrastructure." This future strikes me as a dystopian hellscape, but I've never met an open-weight models advocate who doesn't ultimately concede this is where things end. You'd be surprised how many 'accelerationists' lobbied me, while I was in government, to support an eleven or twelve-figure federally funded data center so that startups could train models at a subsidy and then give them away for free. There was no other way for AI to progress, they said. Perhaps this is the logical end state of things. Nonetheless, I find myself surprised to see supposed accelerationists excited about such an outcome. I think many of them just don't know what they're doing. Many accelerationists do not view the creation and serving of frontier models as a legitimate business. 5. I would guess that the Trump Administration will at some point realize that their best strategy here would be to create large amounts of regulatory risk around the use of open-weight Chinese models. You don't need to "ban open source" (one of the dumber motifs of AI policy discussion). You just need to direct every agency to issue soft law that creates FUD. "A Federal Reserve Advisory Bulletin found that there may be backdoors in Chinese AI models." It needn't be that well justified. You just create enough regulatory risk that every regulated enterprise backs off. You probably don't want to create so much regulatory risk that you scare off the hyperscalers from serving Chinese models; this will just drive startups to sketchier providers. There's a happy middle ground here. I'd assume they will do some version of this. 6. It's probably true that open-weight models of this capability make the world a bit more dangerous, but not so much more that you'll really notice. At some point the models will be capable enough that you will notice. "A nonliving, invisible, dangerous, and infinitely self-replicating agent escaped from a Chinese lab," you say? Color me shocked.

Backpack U 卡 1. 支持中国用户,可用护照 身份证ID申请 2. 目前內測仅开放给 Backpack VIP 3. 同样免地址证明 4. 可直接出金到渣打,众安,天星等银行,目前按照等级给予不同的免手续费出金额度 backpack.exchange/refer/backpack… 或输入 backpack6666

huge mistake posting this less than 24 hours ago i defended @brian_armstrong and tbf i’ve been doing that for years so at least i was consistent i won’t be doing that anymore sry everyone 🙏

before: “we want brian armstrong to embrace meme culture on @base” after: “wait not that meme that’s the wrong one i meant my meme” 😂😂😂

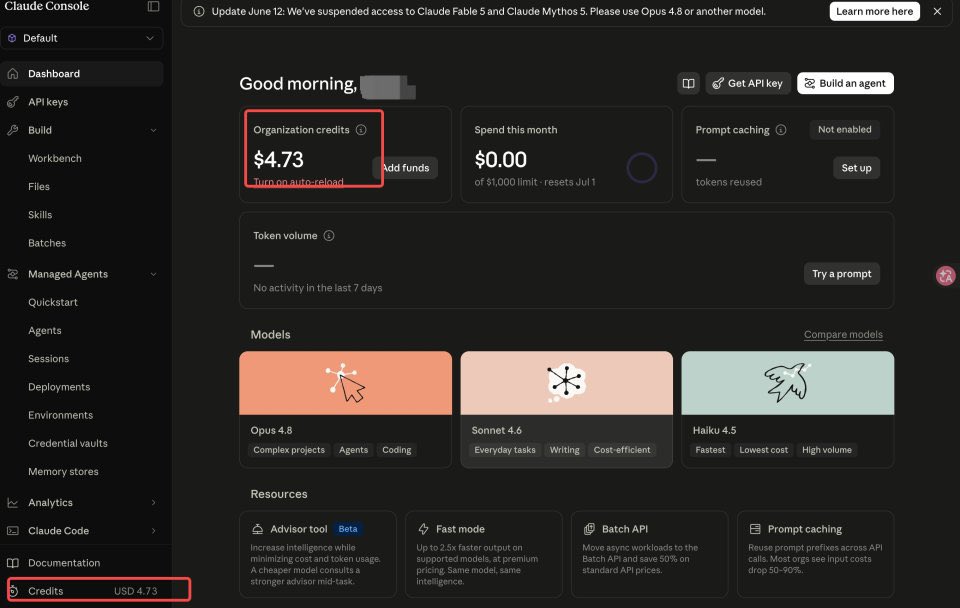

最近比较多人在询问怎么开 Anthropic ( Claude fable / opus )API 以及 OpenAI Codex 的 API 这里用 MP chat 的 U卡 来做示范 这张一样免地址证明,可以直接开 连结: mp.net/c/DDD66 邀请码 06283937 走Visa