Russell Robertson Abaxx CBDO

48 posts

Russell Robertson Abaxx CBDO

@ru55rob

Developing the next generation of derivative market solutions

Singapore Katılım Eylül 2009

69 Takip Edilen124 Takipçiler

@ru55rob @JoshCrumb Russell we need a few meme worthy zingers from you (like big months^tm)

English

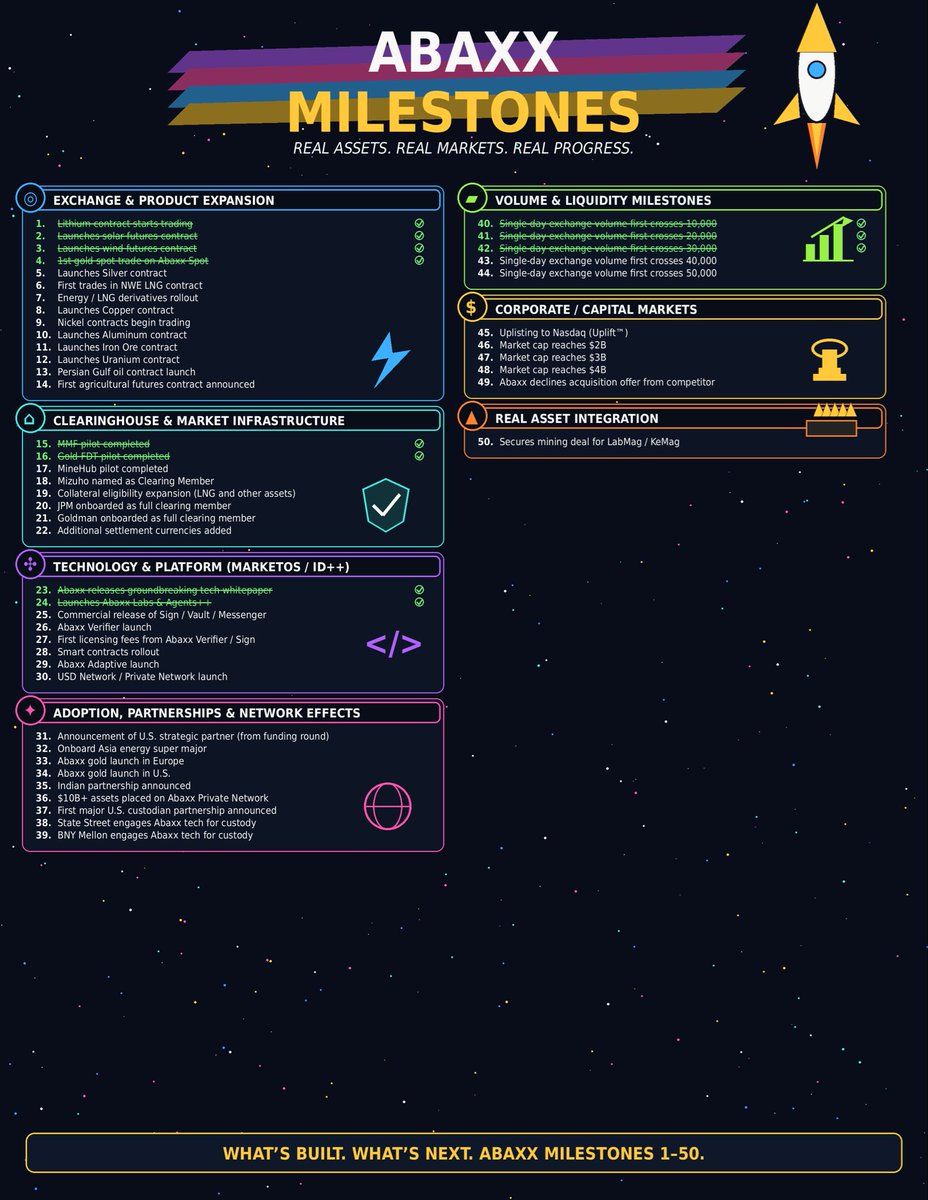

A lot of mine faces opened up and we have people on all of them. An interesting mix of imminent and longer term milestones here (most look like they’re within the next ~12mo though), directionally correct. Not enough on LNG, MarketOS or Agents++ though, we got more mucking from those faces. Plan to make the ~45 day period between calls feel like a six month later update on progress.

Anyway, we still cookin’, meltin’ GPUs #MayDays

Human capital >> Financial Capital

#29ers $ABXX

English

Another Record @abaxx_exchange Day!

Total Lots Traded: 50,227

Total Exchange Revenue: $156,572.50 ($214,777 CAD)

1. GOLD NEW RECORD: 45,501 Lots

2. TOTAL VOLUME NEW RECORD: 50,227

@JoshCrumb @JoeRaia5 @DavidVGreely @ru55rob @CommodMkt @abaxx_tech @abaxx_spot @abaxx_labs

English

Thank you to @straitsfinancia for hosting us at the LME HK dinner last week. They are clearing members of @abaxx_exchange

Hong Kong is clearly evolving as a China focused financial centre and an international gateway which will bring many trading opportunities and regional price discovery to the market.

The development of Hong Kong as a Gold Hub compliments well with the Singapore kilobar market development. I also look forward to the new @abaxx_exchange physically delivered 1000oz .9999 Silver contract launching soon which should create some excellent arbitrage and risk management connectivity between the regions.

It’s all about regional connectivity and basis risk management that will grow the next generation of commodity liquidity and flow.

@abaxx_spot @abaxx_tech @abaxx_labs @JoshCrumb

English

Russell Robertson Abaxx CBDO retweetledi

Russell Robertson, Chief Business Development Officer at @abaxx_exchange and Clearinghouse, shares why #China, #India, and other major #Asian economies are preparing for a more fragmented and volatile #global energy landscape in the months ahead.

Click here to access full podcast: youtube.com/watch?v=RhS8wI…

#Asia #EnergySecurity #SupplyChains #GlobalTrade #EnergyMarkets #Geopolitics #OilMarkets #LNG #Trading #MarketVolatility #EnergyTransition #Abaxx #China #India #Energy #Logistics

YouTube

English

Come and join us on @gulf_intel Daily Energy Markets live.

On zoom at 10:30 am UAE (14:30 Singapore) time today 11th May 2026.

@abaxx_exchange @abaxx_tech @abaxx_spot @abaxx_labs @JoeRaia5 @JoshCrumb

English

Russell Robertson Abaxx CBDO retweetledi

Abaxx Exchange Named Newcomer of the Year at @RiskDotNet's 2026 Energy Risk Awards

Recognition follows the introduction of 16 commodity futures benchmarks and growing activity across Abaxx Exchange markets.

Read Release

abaxx.exchange/newsroom/press…

English

Russell Robertson Abaxx CBDO retweetledi

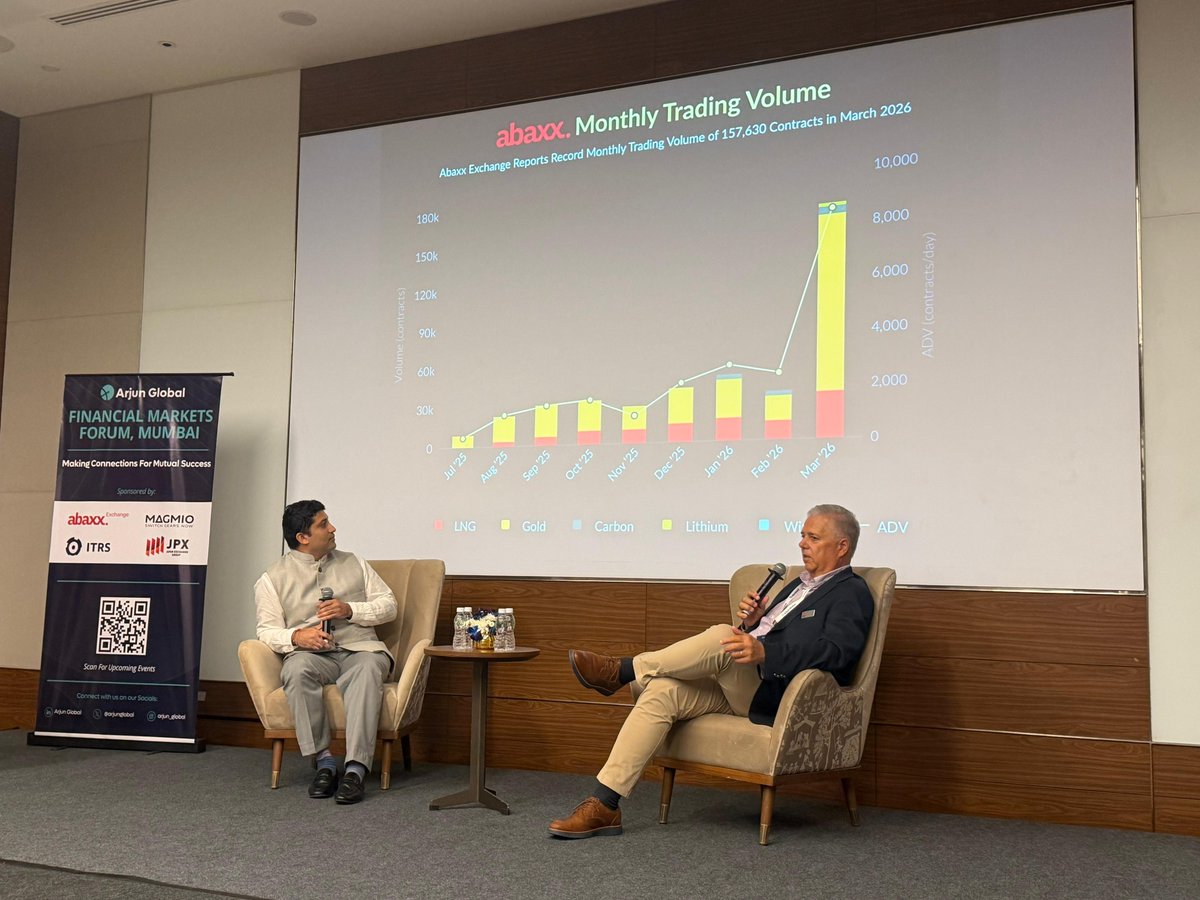

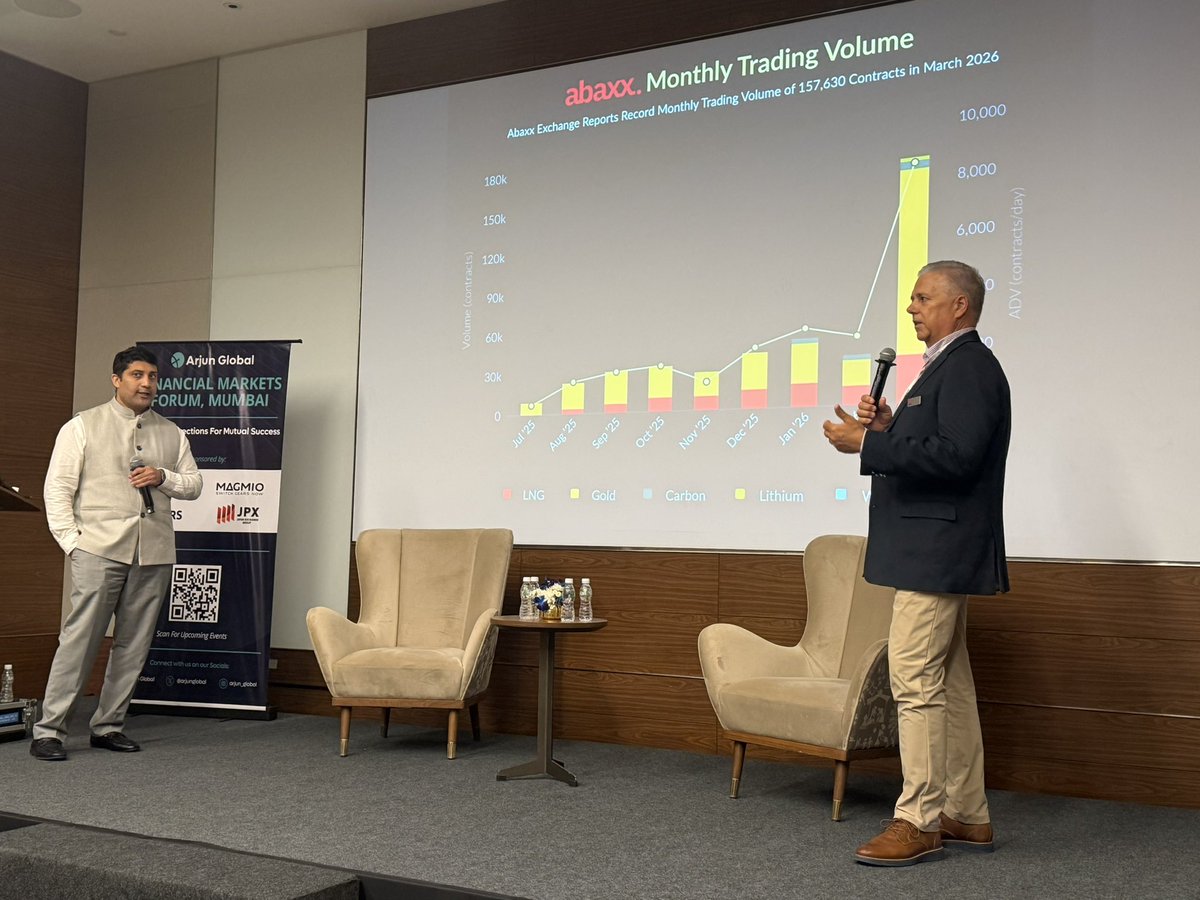

Another update after another full day of institutional investor 1x1s post the 106 target (and blue sky) report. $ABXX

On valuation and volumes; I don’t care too much about the revenue number in 2026. This is pilot trading, hasn’t even started yet. Still priming for the main show onboarding and product pipeline. The big volume day spikes are of course encouraging and some days even above our own current expectations, but two things I’d point out from discussions on the calls

1) short/medium term I still focus more on the derisking and node onboarding deeded for full-scale volume and the conservatively ~300mm per year EBITDA that comes with a ~1mm contract per day commodity exchange. The early jump shows that the nameplate “global commodity exchange capacity” is showing signs of utilization, and that number can grow quickly from 30k days to +150k days over next 12mo with more regions, products and bank FCMs (and to the point of the analyst, valuation is still pricing something like 20% chance of success on just LNG and Singapore Gold/PMs…and who the heck has the other 80% chance when we so far have no competitors to scaling these markets…”Who's gonna do it? You? You, Lieutenant Weinberg?”)

2) longer term, and I ended up having this discussion with a few tech investors this week on the back of Agents++ release, you’re still in the “counting CDs mailed from Netflix days”, not focused on what the Abaxx Network actually is with the clearinghouse, MarketsOS and now Agents++. If I may be so audacious, I’m sure Hoffman got super annoyed when all the analysts wanted to know about was CDs mailed the next 12mo (and why they dropped off in April’0*)? The prize is the tech [insert always had been meme]

#29ers #PlanYourMineMineYourPlan #WorldBuildersOrBust

Josh Crumb 🆔++@JoshCrumb

Been having some very interesting institutional investor meetings after this report — as has the analyst, from my understanding — especially after calling out that $2,500 per share blue sky number (kudos to the analyst on that btw, having been in a similar seat I know it takes guts to put that in writing). Given the conversations, I’ll spend more time on valuation and the way we think about growth and ‘spendvesting’ allocations on the next call. But a few thoughts on the subject (and please, this is ALL subject to risk causations, forward looking statements, analyst disclosures, etc….we are world-builders-or-bust from the beginning, allocate appropriately, big problems trying to solve, big risk/big potential reward, baja racer emotions till we cross the line, etc): 1) Start with the core signal, there are tons of moving parts, but focus on three basic questions as a foundation: a) Is the business model proven and sound, does management have the experience to execute: obvious yes (and I’ll add that we put together the best global team in commodity market building, we ARE the global-A team even compared to companies 50-100x bigger that we will compete with imo) b) Is Singapore an important emerging global gold hub (especially given geopolitics across rivals NY, Shanghai, Dubai, etc)? Is Abaxx the only futures market, spot market, and most advanced HQLA tech vision? Yup. Ours to lose. Next question. c) Now to the stage-1 flagship, is there an LNG price/benchmark everyone trades on as a standard, or is it up for grabs and what are the alternatives to Abaxx now that its already showing liquidity? …no agreed price, and HHub is not LNG, TTF is not LNG, and billions of people are not going to price their core energy on a reporter surgery of limited information participation…and China doesn’t recognize the ‘Japan Korea’ survey, they are very astute about building new commodity markets — unlike the overly bureaucratic and overly financialized “west” IMO (Abaxx now has much greater than 50% of “winning this estimated $5B asset” imo, and we hope to put the nails in that coffee within the next 12mo). There, forward risk-adjusted valuation justified. Done. Nothing is certain. You want certainty and lower mark to market draw down risk while you manage OPM, buy a bond or an index. You want risk adjusted return, a team hell bent on providing solutions to some of the world biggest challenges, with the best teams to do so, join us. We were “too expensive” for a lot of the street as an “idea” at ~$200mm pre rev (~$12), even though we could have sold our infra for more than that, it was the stupidest asymmetric option in the market and I wasn’t afraid to say it. For those who think $50/$60 is too expensive until we fully prove out benchmark status, just test out how little is for sale between $60 and that $100 price target, because the real money (large and small) that owns this asymmetric option are comfortable with any [hedge-fund driven] draw downs and IMO not willing to sell (just on business model stage 1, and i don’t intend to give up or lose on the larger business model stage 2 that I founded this company on either). $ABXX #29ers #NowWeScale #LetsGetPhysical #MayDay

English

English

@ru55rob @abaxx_exchange @JoshCrumb Thank you kindly for your time and the detailed response. Always interesting times ahead for $ABXX and the #29ers . In the meantime i leave you with a fun version of my song. Keep crushin it🍻 youtu.be/s0CvSIhF_tA?si…

YouTube

English

@abaxx_exchange

Commodity prices are set against big benchmarks in certain areas that may not truly show the relevant price for an asset at the right time or the right place. We will change that for true price discovery, recently working with major Chinese lithium operators.

English

@Bprivateers69 @abaxx_exchange @JoshCrumb There is opportunity to look at how this buying power can get assets at relevant prices. Abaxx is clearly a good venue to look at these changes and build more efficient price discovery mechanism.

Great question and you can write a deep paper on it

English

@ru55rob @abaxx_exchange @JoshCrumb Hey Double R. First time caller long time listener. I feel like ur message above could be applied to UAE and oil markets. Do you see OPEC fissures as an opportunity for $ABXX in the oil market/contract space. I’ll hang up and listen, thank you. #29ers

English

@Bprivateers69 @abaxx_exchange @JoshCrumb That said the value of Middle East crudes is very relevant as well as Brent and WTI.

But again. Why should the biggest buyer of Middle East crude (china) or swing buyers (India) continue to do what they are told.

English

@Bprivateers69 @abaxx_exchange @JoshCrumb The changes in oil markets are happing rapidly and historical spreads have been blowing out big time the last couple of months.

Disruption events to benchmarks do not happen very often and oil is pretty complicated as there are a few formulae’s for different grades of oil.

English

Russell Robertson Abaxx CBDO retweetledi

Velocity Trade and Kilo Capital Execute First Trades in Abaxx Spot Gold Pool

"Abaxx offers a compelling platform as the market evolves, particularly against the backdrop of broader efforts to position Singapore as a trusted gold hub."

Read Release

investors.abaxx.tech/press-releases…

English

Russell Robertson Abaxx CBDO retweetledi

Gold Singapore futures fuel Abaxx Exchange's single-day trading record via @FOWGroup

"The surge in gold Singapore futures trading activity has driven Abaxx Exchange’s single-day volume record this week, underscoring the physical contract’s expanding foothold in Asia."

English

Russell Robertson Abaxx CBDO retweetledi

Abaxx Exchange is now recognized as an Organised Market Place by the EU Agency for the Cooperation of Energy Regulators (ACER), enabling the exchange to meet reporting obligations under EU REMIT.

abaxx.exchange/newsroom/press…

English

Russell Robertson Abaxx CBDO retweetledi

Back from the @ArjunGlobal India Roadshow, where @wuthel moderated “Hunting Alpha in an Uncertain World” and led a gold trading workshop in Gurugram and @JoeRaia5 joined a fireside in Mumbai on how Abaxx Exchange is building the next generation of commodity futures benchmarks.

English

@Bprivateers69 @abaxx_exchange @JoeRaia5 @abaxx_tech @arjunglobal The million lot party going global 🥳🥳

English

@wuthel @abaxx_exchange @JoeRaia5 @abaxx_tech @arjunglobal Russell you gotta fly me around with you and JR in q3 for the 6’6 volume bar pictures and a couple ice cold BLs #29ers

English

The @abaxx_exchange trading volume bars are taller than @JoeRaia5 !!!

@abaxx_tech group continue in Mumbai with @arjunglobal

English