Shob

328 posts

Shob

@runningthemodel

On the path to $1M at age 25 $TSLA $NVDA $PLTR $IREN

Katılım Temmuz 2021

62 Takip Edilen23 Takipçiler

$IREN SW energization is great, but massive amounts of capital is needed to fund this unicorn site. Shareholder dilution is too costly.

Energize, Sign, and Execute (1/3) ✅

IREN@IREN_Ltd

Sweetwater 1 has been successfully energized – a key milestone in the development of the broader 2GW Sweetwater campus. @danroberts0101, Co-Founder and Co-CEO of $IREN commented: “Delivering Sweetwater 1 substation energization on schedule reflects our disciplined execution, the strength of our supply chain relationships and the efficiency of our vertically integrated development model. It is another example of our ability to design and construct large-scale infrastructure reliably and at speed to meet market demand.” Learn more: iren.gcs-web.com/static-files/d…

English

@seper8tor @danroberts0101 Oh no, 4 days later than I wanted. I’m gonna sell.

English

@danroberts0101 This could have been so much more effective monday instead of friday after the bell. $IREN used to be world class at pumping their stock. I'm a little disappointed here!

English

Shob retweetledi

345kV substation energized at Sweetwater 1.

Power first, compute next. $IREN

English

Shob retweetledi

Sweetwater 1 has been successfully energized – a key milestone in the development of the broader 2GW Sweetwater campus.

@danroberts0101, Co-Founder and Co-CEO of $IREN commented:

“Delivering Sweetwater 1 substation energization on schedule reflects our disciplined execution, the strength of our supply chain relationships and the efficiency of our vertically integrated development model. It is another example of our ability to design and construct large-scale infrastructure reliably and at speed to meet market demand.”

Learn more: iren.gcs-web.com/static-files/d…

English

@Lazarus_Capital @ilzmcfly Nebius earns more per gpu in their microsoft contract because of location. New Jersey vs Texas. New Jersey is low latency to key markets such as new york. Land and power is also more expensive there.

It’s not a reflection of much else beyond that.

English

Idk anyone who was arguing the hyperscaler contracts for $NBIS were anything other than bare metal.

Two, can get a good estimate of how many GPUs they ordered based on their density and power capacity.

Three, the main NBIS margin expansion comes from NBIS designing and setting up their server racks internally than paying DELL 10%+.

Just working back from from the $IREN $MSFT deal, $1.94B on 76,400 GB300s comes out to $25,392 ARR per GB300. Using that for NBIS and their yearly revenue, you would need over 137k GB300s.

Based on Nscale standard of fitting 104k GB300s into 240 mw, that tells use NBIS needs >316mw. Impossible for their fit.

Based on @genZinvest0r latest breakdowns of the nat gas gen power capacity, PUE, emissions control, etc, the MW get reduced even more. I linked the thread. This tells us theyre likely earning even more per mw than estimated.

Since we established $NBIS earns more per mw and per GB300 than $IREN from the same customer $MSFT, we can move unto costs.

$NBIS saves a significant amount setting up their racks in house vs out sourcing it to Dell. I linked how backing out Dell's disclosures to get an operating margin of over 9% on AI servers. Gross margins will be even higher. And since IREN purchased GPUs with all the associated hardware (networking, storage, other ancillary equipment, etc) their margin goes even higher. Arkady stated 15-20%. Semianalysis stated 10--15%. I took the mid point of 15%.

Lets assume that MSFT gave the same contract rates to IREN and NBIS, NBIS would need 137k GB300s.

IREN paid $5.8B on 76,400 GB300s. That would be $10.4B in capex. 15% savings is $1.56B saved. 10% is $1.04B. Can adjust by adding 2% back from NBIS margins.

That's a lot of savings even if their GPU rates are the same.

Also, seen some $IREN bulls attempt to compare the savings $NBIS gets on GPUs to $IREN savings on their DC. Just make sure theyre comparing the delta in savings and not accidentally doing some colo vs owned site math.

x.com/Lazarus_Capita…

x.com/genZinvest0r/s…

English

Roman from $nbis just confirmed Meta and Microsoft are bare-metal deals (NO SOFTWARE) on Daniel Koss Interview

"We have Meta and Microsoft which are big customers that come to the bare-metal layer of our platform"

"They consume these large clusters, they bring most of software themselves"

"they need reliable infrastructure"

Everything Iren bulls said Roman confirmed it.

$Iren bulls were right yet again..

Do you understand why we don't know the GPU Count, Model and Colocation fees payed...

It's quite funny seeing the Nebius bulls argue that they got a better deal than Iren and it included software, but they didn't.

I don't blame them because Nebius did not release any details but you were gullible to believe Microsoft or Meta will pay those software margins.

Bear arguments against Iren dead.

Bull arguments for Nebius dead.

none of those bare-metal nebius deals included payed off owned datacenters.

Iren actually got the better end because it 5 years they will have a payed of datacenter + gpu's.

English

Shob retweetledi

Where power becomes intelligence.

NVIDIA GB300s arriving at Childress for our Microsoft Horizon deployment. Big effort from the team. $IREN

Childress, TX 🇺🇸 English

@Lazarus_Capital Ultimately its a question of whether you have faith in the management to finance it as well as possible. They definitely have loan capacity. They have also said previously that they would be using data center financing. I have no reason to believe otherwise.

English

@runningthemodel Can quantify all that but they’ll need to raise for expansion. The you into into return > cost of capital

English

All these $IREN bulls have 100%+ IRRs yet no one is able to share a model.

Shob@runningthemodel

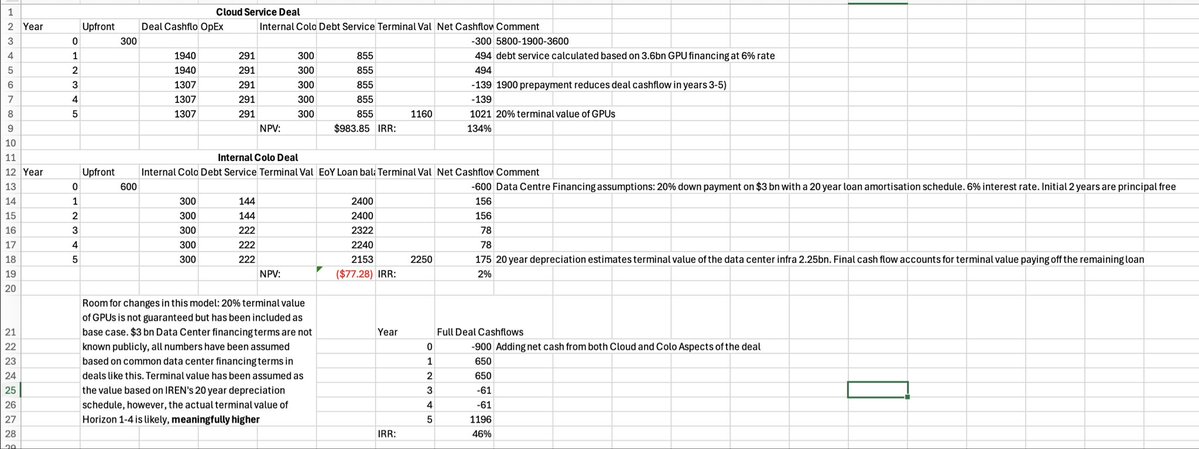

@Lazarus_Capital 135% levered IRR on the microsoft deal btw. But yeah ur right… unattractive returns.

English

@Lazarus_Capital Peep EQIX ebitda margins last year. They are also guiding for it to go higher. This is not the top.

English

@runningthemodel that should be reflected in the colo rates vs cost to build and Im not seeing it. I am seeing several land acquisitions with power and power expansion.

English

@Lazarus_Capital Also, IREN is far from tapped out on financing.

1. Microsoft deal backing covers the GPU, DC infra and some on top of it

2. IREN has a pretty good D/E compared to alot of others in the industry.

3. They have revenues and profits at present even without HPC through BTC

English

@Lazarus_Capital Owning the DCs derisks the company alot. The market is also starting to increase colo rates for DCs since the power scarcity thesis has come into play in a big way in the last 12 months it may even turn into a great financial driver in the near future.

English

@Lazarus_Capital Appreciate the kind words though. Put effort into that model.

Largely I do agree with you on the point though that management brushes off the datacenter aspect of things. Its definitely the less exciting part.

English

@Lazarus_Capital There isn’t any point modelling this because its completely unknown. Management also puts more focus on the cloud portion of the deal because that is the actual thing that microsoft is paying for. The data center also has a life that goes far beyond the deal horizon.

English

@runningthemodel Hi Shob, feel free to share your model or where you got these numbers because it’s multiple higher than even what management guide to.

English

Seems pretty clear that $IREN is unable to effectively land cloud deals at attractive returns.

With their advantage (according to bulls and management) being in DC development, why aren't they doing colo?

They have over 4GW of power, they won't even be able to raise enough capital or bring the DCs online for years! What's the problem?

QUICK MATH:

$6B ATM

$3.5B CAPEX for B300 guide.

$2.5B for other.

$2.5B on a 80% LTV enables $12.5B

@ $10/mw allows for 1.25GW CT IT, 1.875GW gross

@ $15/mw allows for 833MW CT IT, 1.25GW gross

Still no where near to sell out of their portfolio.

Lazarus@Lazarus_Capital

Seems like the popular $IREN bulls didn’t cover the b300 guide down that came with the $6B ATM. Funny how they’ll have 50 posts about a transformer being delivered to SW but AWOL when it comes to cash flows. Here’s the breakdown.

English

Do $IREN bulls not understand how bearish this tweet is when they just guided down on their b300 ARR?

Inherently saying no pricing increase unless compute demand shortage increases.

Daniel Roberts@danroberts0101

Feels like we’re still early in the compute cycle. Supply isn’t easy, real-world constraints are everywhere. And every step forward in AI just seems to create more demand for compute.

English