Sabitlenmiş Tweet

$NUAI Thesis

I know you’ve probably been seeing $NUAI across your timeline recently, and was wondering what the deal with the company is. When I first saw this micro-cap stock on my timeline, I was extremely hesitant. But, after looking deeper I started to draw parallels to companies like $IREN and $APLD before the markets inevitably priced in what they could be worth. For those of you who have been in $IREN you understand that a 10x means speculating on an asset before its true value becomes obvious to the market, and seeing a vision for a company that plans to transition to something different. I believe $NUAI is the next 10x opportunity at $4.60, and here’s why.

Introduction

$NUAI’s flagship site is called TCDC, or Texas Critical Data Centers, that is 1.4GW Gross or ~1GW Critical IT load, in Ector County near Odessa, TX. I believe the market is completely missing the scale of what is happening at the TCDC site. If you haven’t been paying attention closely it’s easy for the recent announcements to fly under the radar. Since the beginning of this year $NUAI has put out announcements every couple weeks forging partnerships with energy generation partners, hiring significant industry leaders, and working meaningfully to prep their site for their hyperscaler client.

Following the Breadcrumbs

At the beginning of the year $NUAI closed the acquisition of the remaining 50% stake of TCDC from SharonAI, their original JV partner on the project. This was to have total control over the land to build new partnerships, and likely at the hyperscaler clients request to bring a new JV partner to the table.

In late February $NUAI announced a 450 MW Behind-the-Meter Generation Plan at TCDC with Thunderhead Energy and TURBINE-X Energy to generate power for the project. They have a SPV/venture where they have partnered with a private equity firm to fund the capital required to source, install, and run 450MW of gas turbines. They will generate an ROI as they sell power to NUAIs TCDC tenant. This equipment is normally extremely difficult to source, and $NUAI was able to grab these 2-3yr long lead time items in an extremely supply constrained environment, showing the connections of the upper management. The notable thing about this partnership is that they don’t have to put any capital upfront for this equipment, allowing them to start generating revenues while loaning the equipment without huge dilution (~70m).

Then, in mid-March $NUAI hired Ted Warner, ex head of the Energy, Power, and Digital Infrastructure at Northland Capital Markers, where he successfully structured and managed more than $7 billion in financing solutions specifically for large-scale data center developments. This was the signal that caught my eye and made me significantly up my position in the company. Something notable is his PSU’s, or Performance Stock Units, which reward him significantly for “Entering into a binding commercial agreement with a hyperscaler for a minimum of 200 megawatts”. Judging by his history I put him as an A+ hire, and you can see more about his notable achievements here.

x.com/litigious_dulc…

Now, to get into the most recent developments that completely change this company from just a speculative random micro-cap to a more credible multibagger infrastructure play. On April 1st, $NUAI secured an LOI with Stream Data Centers. Originally, $NUAI was slated to co-develop the TCDC site with other partners (first Sharon AI, then Primary Digital Infrastructure). However after back and forth for months the unnamed hyperscaler tenant likely mandated that their own preferred execution partner handle the physical construction and operation. Stream is one of the top data center

This project with Stream will be done in a GP/LP fashion, where instead of issuing billions in new stock to pay for construction, the deal utilizes a heavily levered GP/LP (General Partner / Limited Partner) joint venture structure, operating at roughly 80% Loan-to-Cost (LTC). The roles exist as such:

The Originator ($NUAI): $NUAI acts as the local sponsor. They bought the TCDC 438-acre site, secured the initial power footprint, navigated local Texas politics, and laid the development groundwork. Originally I had thought that this agreement would mean passing up the GP role fully to steam and forfeiting their GP revenue streams as the originator. After contacting IR they said “we expect the final structure to reflect the contributions from each (NUAI as a project originator + local relationships, Stream as the developer)”

The Operator (Stream): Stream Data Centers steps in as the development manager and operator. They bring the engineering blueprints, the construction expertise, and the direct, trusted relationships with the hyperscaler. The hyperscaler obviously has a preference for this developer and has likely worked with them before.

The Institutional Capital (The LP): An unnamed institutional investor (99%+ confidence being Apollo, given their majority ownership of Stream) acts as the Limited Partner, writing the massive equity checks and leading the project financing. Apollo Global Management is consistently ranked among the top, most influential, and pre-eminent firms in private equity globally. It is commonly considered part of the "Big 4" of the PE industry and a mark of validation for this project that shouldn’t be looked past.

What this structure does is it protects $NUAI shareholders from the dilution that is so costly to shareholders in a company like $IREN, which long term (2-3 years) has potential to grow into a 100B+ market cap giant, but will need to dilute massive equity to get the cashflow flywheel going (as shown by 6B ATM). A 1.4 GW campus costs upwards of $12 Billion to build, and $NUAI cannot fund that on its own balance sheet. I expect this LOI to be facilitated into a binding agreement in the next 2-6 weeks.

The second piece of news that is the most convincing is the $290M credit facility from Macquarie. Just to put it out, in case it isn’t obvious already, Apollo and Macquarie don’t blindly gamble on some random micro-cap without doing extensive underwriting and due diligence on the parties involved. They deemed $NUAI worthy enough at a $250 million market cap to receive a $290 million multi-tranche facility that shifts the risk profile of the entire TCDC project.

The structure goes as follows: a $20M committed Term Loan A-1 to kick off development, followed by $30M and $40M tranches, with a massive $200M Delayed Draw Term Loan waiting for execution milestones. That’s already impressive in itself, and likely came from Ted Warner’s existing relationship with Macquarie, but an even stronger validation is the equity kicker. Macquarie took a direct $5 million equity stake at a 20% premium to market share price, taking their entry at exactly $5.00 per share. They also have a tranche of warrants that will have an exercise price of $5.00. The warrants will be issued across the first $50 million drawn on the Facility.

When one of the largest infrastructure lenders in the world is taking an equity stake at a 20% premium to the market’s price, it should tell you everything you need to know about the asymmetry of this setup. You have to ask yourself, would Macquarie offer a loan of this size to a random microcap without doing extensive due diligence and underwriting of an advanced hyperscaler LOI or term sheet?

Luckily, we got the answer to that hidden in the SEC filing of the Macquarie term loan agreement without a formal press release from $NUAI. $NUAI currently has an LOI in place with a hyperscaler tenant as of March 24th, 2026. I believe the reason it was not put in the form of a press release was at the hyperscalers request, and you can read more about it below from @kamikazzzi1981

x.com/kamikazzzi1981…

Now that all of the pieces of the puzzle are starting to come together that a hyperscaler deal is imminent, what should the company actually be worth?

Stock Price Projections

Firstly, I'd like to get out of the way that if you believe that $NUAI will secure a hyperscaler deal in the first place the announcement alone will probably put the stock around 2x higher than the current prices, or around $9-$10/share. This is by giving Stream, one of the most reputable data center builders hand selected by a hyperscaler, around a 60% chance of execution from the math below. If you want to, from that point, you can decide whether you want to sell, or if you believe they can execute the numbers start to get pretty wild.

From Phase 1 alone, with super conservative assumptions (more likely to be ~$1.50M EBITDA/MW)

Phase 1: 200 MW x $1.35M EBITDA/MW = $270M project EBITDA.

At 50% ownership, that is $135M to NUAI.

At a 14x-16x EBITDA multiple, that suggests $1.9B-$2.2B of value, or $14-$16/share on 135.5M fully diluted shares.

Northland’s analysis used a 19x EBITDA multiple in their analysis, 14x-16x is extremely conservative. At a 19x multiple you get a share price ~19$/share

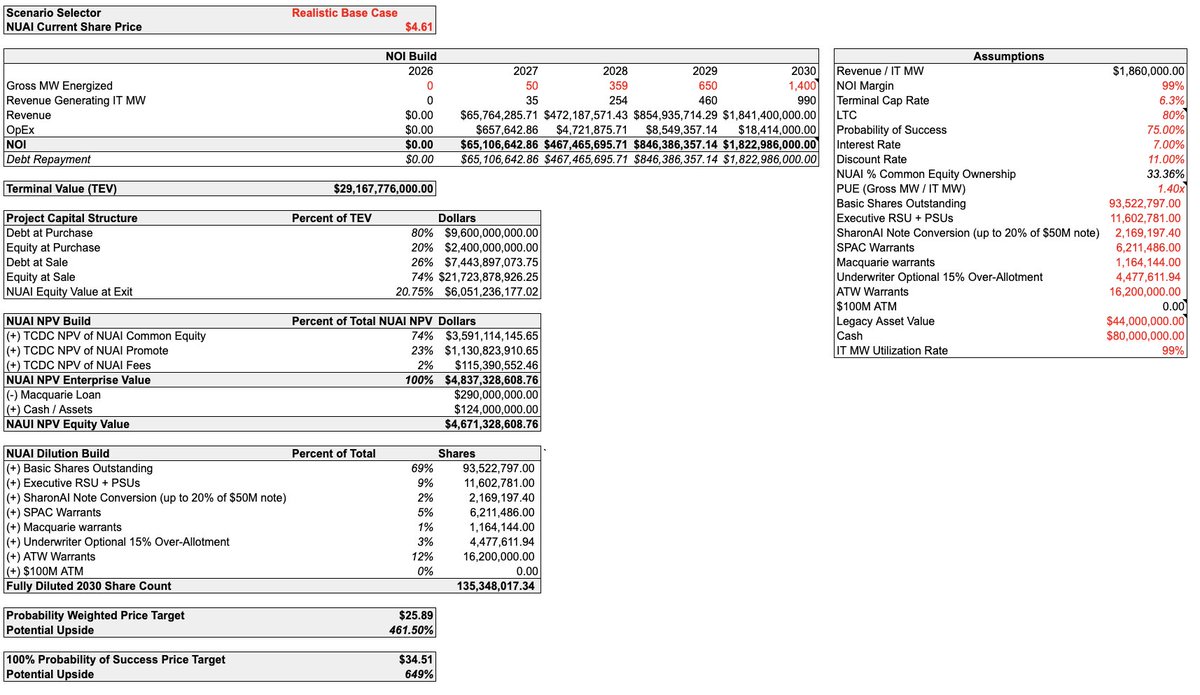

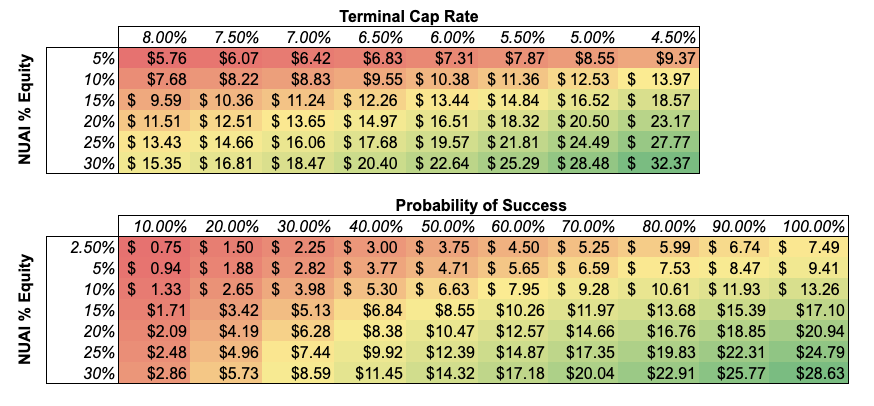

If they can fully execute on Phase 1, the full TCDC 1.4GW campus can be modeled out as done by @ThePrudentWhale

x.com/ThePrudentWhal…

• $34.51 Price Target in a 100% success case.

• $25.91 Probability-Weighted PT (applying a 25% execution risk haircut).

And here is super conservative bit of the model: this entirely excludes Behind-The-Meter power generation economics for phase 2+, GP stream revenues, 7 GW New Mexico development pipeline, and the reinvestment of cash flows into the futures phases of the projects for more equity.

English