#DEEDEV - DEE Development Engineers Ltd

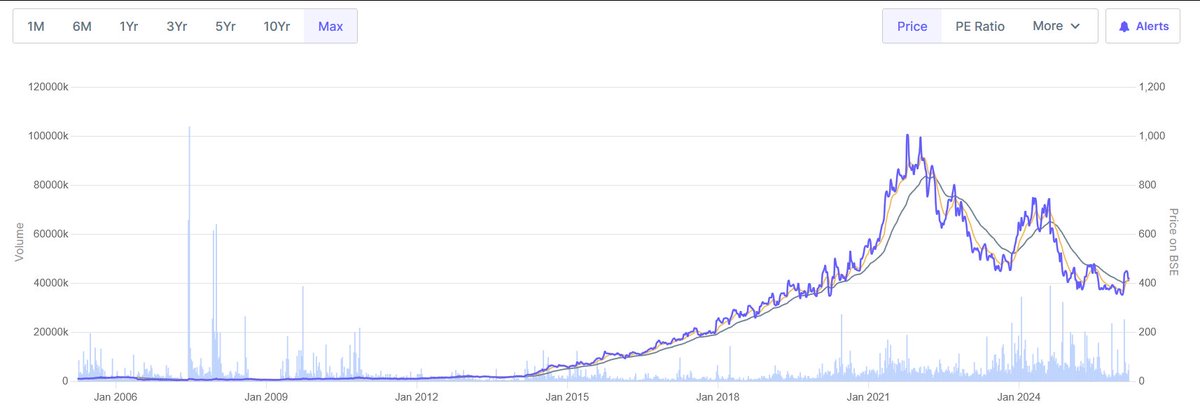

DEE Development is India’s largest manufacturer of specialized process piping solutions by installed capacity. The core narrative here is a financial turnaround fueled by India's accelerating capex cycle, coupled with an aggressive backward integration strategy that is structurally expanding margins. The Q3 FY26 numbers validate a massive inflection point: Consolidated revenue surged 77% YoY to ₹286.7 Cr, and PAT flipped from a ₹13.3 Cr loss last year to a robust ₹18.55 Cr profit. Operating EBITDA margins expanded significantly to 16.6% in Q3 FY26, up from a suppressed 3.5% in the same quarter last year.

-> If execution sustains and margins stabilize at these expanded levels, DEEDEV is poised to transition from a pure turnaround story into a structurally higher-margin, compounding engineering play.

Growth Catalysts & Triggers

1. Backward Integration (The Margin Multiplier):

The biggest structural catalyst occurred just days ago. On March 19, 2026, DEEDEV commenced commercial production at its new ₹89 Cr, 7,000 MTPA Seamless Pipe plant in Anjar, Gujarat. Previously, the company had to import these high-wall-thickness alloy pipes to use as raw materials. Manufacturing them in-house is expected to improve EBITDA margins by reducing imported seamless pipe costs and freight dependency. The market validation was immediate: they secured a ₹58 Cr seamless pipe order from a power sector JV before the plant was even fully commissioned.

2. Explosive Order Book Momentum:

The company's order book is expanding aggressively, jumping from ₹1,319 Cr at the start of February to ₹1,913 Cr by February 28, 2026. This was driven by a massive ₹754 Cr inflow in February alone, highlighted by a $40+ million export order for Heat Recovery Steam Generator (HRSG) piping from a US-based OEM and strong domestic traction from PSU giants like BHEL. Execution is scaling concurrently; the Anjar facility’s base process piping capacity was recently doubled to 30,000 MTPA to handle this influx, with a large portion of this ₹1,913 Cr order book expected to execute over the next 2–3 years (FY26–FY28).

3. Long-Duration Optionality (Hydrogen & Pilot Plants):

While thermal power and oil & gas pay the bills today, DEEDEV is building early optionality in emerging hydrogen infrastructure. They have strategically entered the hydrogen sector via an MoU with an International Clean-Tech partner to build modular hydrogen production systems in India and Thailand. Additionally, they have opened a new, high-margin vertical: designing and fabricating small-scale "pilot plants" for chemical and nuclear companies to test R&D processes before full-scale commercialization.

Key Risks:

Biomass power segment litigation continues to drag consolidated margins. Long-gestation international HRSG orders expose the company to raw material price volatility and execution risks. The business remains working-capital intensive, and growth is highly dependent on sustained capex cycles in the Oil & Gas and Power sectors.

English