Sabitlenmiş Tweet

I've decided to go "ALL IN" on Global Atomic. Beginning today and into the new year I'll be buying as much stock as I can afford. This will be life changing. $GLO $GLATF #Uranium

English

Stephen Satkowski

334 posts

"Confidence is increasing that we now have one of the largest #uranium projects in the United States.” With strong validation from initial drilling and historic work at Copper Mountain, the scale potential is becoming clear. ⚡ Growing land position ⚡ Historic + new data alignment ⚡ Increasing confidence in core deposits Learn more: myriaduranium.com

2026 is shaping up to be Skyharbour’s largest exploration year to date⚛️ Following the closing of our $61.5 million joint venture with Denison Mines at the Russell Lake Project, more than 15,000 metres of drilling are planned, all fully-funded. $SYH.v | $SYHBF Full Interview🎥: youtube.com/watch?v=XO59TN…

YEMEN HOUTHI INFORMATION MINISTER: WE ARE CONSIDERING CLOSING THE BAB EL MANDEB STRAIT

🚨 OIL TO $200? Here’s why it’s EXTREMELY BULLISH for #Silver & #Uranium! 🔥 Skyrocketing oil = massive cost-push inflation + rising stagflation fears. Central banks may be forced to keep rates higher for longer. But smart money rotates HARD into: • Silver → an industrial powerhouse (solar, EVs, electronics) + a proven inflation hedge. History shows it explodes during commodity booms. • Uranium → nuclear becomes the ultimate winner as nations scramble for energy security and alternatives to oil. Demand surge incoming. Are we heading for a 1970s repeat? Silver and uranium were massive winners back then. The initial fear-driven dip has created a great opportunity to position now, before the rocket takes off. Where to invest? Silver: Established miners like $HL, $AG, and $PAAS should perform well. I also like $HYMC, currently drilling one of the largest deposits in the world, and Southern Silver $SSV, which has strong upside potential. $JTWO is my wildcard, a low-cap company that recently reported bonanza-grade silver samples. Uranium: Major producers $CCJ and $KAP should benefit significantly. $DNN and $NXE are now permitted but may face rising capex due to inflation, still solid picks in my view. $UUUU and $EU could be safer options given current production. Among explorers, I like Skyharbour $SYH, drilling near Denison’s Wheeler River; Myriad Uranium $M.CN, a low-cap company with a project that could host one of the largest deposits in the U.S. based on historic results; and Noble Plains $NOBL, a tiny explorer that recently drilled up to 1.5% grades on a textbook ISR project. Just my thoughts, there are many other companies that could also perform very well. Feel free to share your favorites below. Disclosure: I am a shareholder in most of the companies mentioned. $M.CN, $SYH, $JTWO, and $NOBL are sponsors.

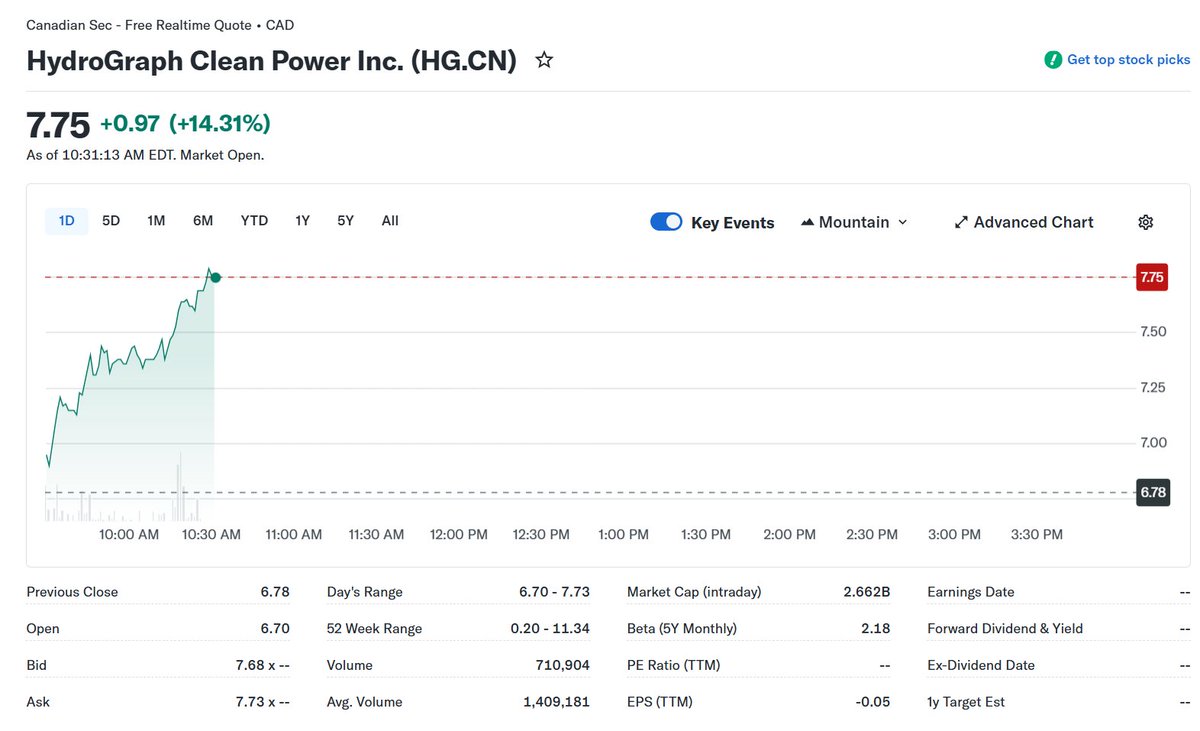

As @elonmusk loves to point out, solving hard problems creates incredible value. This is likely the world’s hardest problem. I think we may solve it and that solution will come from innovating with $hg $hgraf and its Turbostratic Fractal Graphene variants.

$CCJ's Grant Isaac on M&A: He doesn't see anything out there worth acquiring right now. He sees a bunch of overvalued DFS projects that won't come online on schedule or on budget, and "there's a lot of hurt coming to those investors," and valuations will finally make sense again.

Myriad Uranium has earned 75% of Copper Mountain and is advancing a transaction to acquire the remaining 25%. Nearly doubling its land position, consolidating historic deposits across one of the largest U.S. uranium districts. Explore more: ow.ly/6LVu50Ysl27 CSE: $M.CN | OTC: $MYRUF | FRA: $C3Q

Skyharbour’s prospect generator model continues to advance multiple projects across the Athabasca Basin📍 At Preston, Orano is planning another 3,500m of drilling following Skyharbour consolidating ownership, with the project operated by Orano. Exploration is targeting conductive corridors extending from the Arrow trend on the Basin’s west side. Additional work is also expected this year at South Falcon East with Terra Clean Energy and at the Falcon Project with North Shore. $SYH.v $SYHBF Watch the full interview📽️: youtu.be/6q9DDCB3gNA

@umesh_gandhi007 @devengandhi Oh I completely agree about investor sentiment, at least for some. Look at all the folks that claimed they would be patient, now demanding news. This has happened on every run up. Those who really believe stay. Those who need a fix get bored and leave. Doesn't change anything.