@WillBiddy_ For anyone wondering how cprt could be ai beneficiary here's what grok says about it

x.com/i/grok/share/b…

English

seal

899 posts

@sealcap

Mostly stocks, 20% hurdle + some trades on the side

most of you aren't ready for this conversation but $wu looks like it bottomed

$RDDT -- just finished reading a expert network transcript from one of the services we use. This expert thinks $RDDT will move to usage based pricing for the LLMs (ChatGPT, Gemini, etc) when they re-negotiate their current licensing deals which expire in the next 6-12 months. Right now $GOOG is paying $60M per year... this expert thinks $GOOG (ie Gemini) might end up paying $300-400M per year in a new licensing deal with usage/dynamic pricing. I know for a fact the sell side is not modeling any of these new LLM licensing deals into their forward estimates so this is a major catalyst if/when it happens. Right now $RDDT is making $130M per year from Gemini and ChatGPT, it's possible that number could be $600-800M in the next 12-24 months at approximately 100% profit margins. Currently the sell side is looking for $4.1B of revenues in CY2027 with 41.5% net income margins.. which is $1.7B of net income. Even without these new deals, I think $RDDT does $4.6B of revenues in CY2027 with 43% net income margins... which is $2.0B of net income. Now let's assume we get these bigger LLM licensing deals... it's possible that CY2027 revenues are $5.0B to $5.4B but net income margins would be more like 52-54%.. which implies $2.75B of net income. In this last scenario (if it plays out the way I suggest)... then it means you'd be buying $RDDT today at 9x CY2027 net income. NFA. DYOR. **I own $RDDT personally and we own $RDDT at @FirstWaveFund

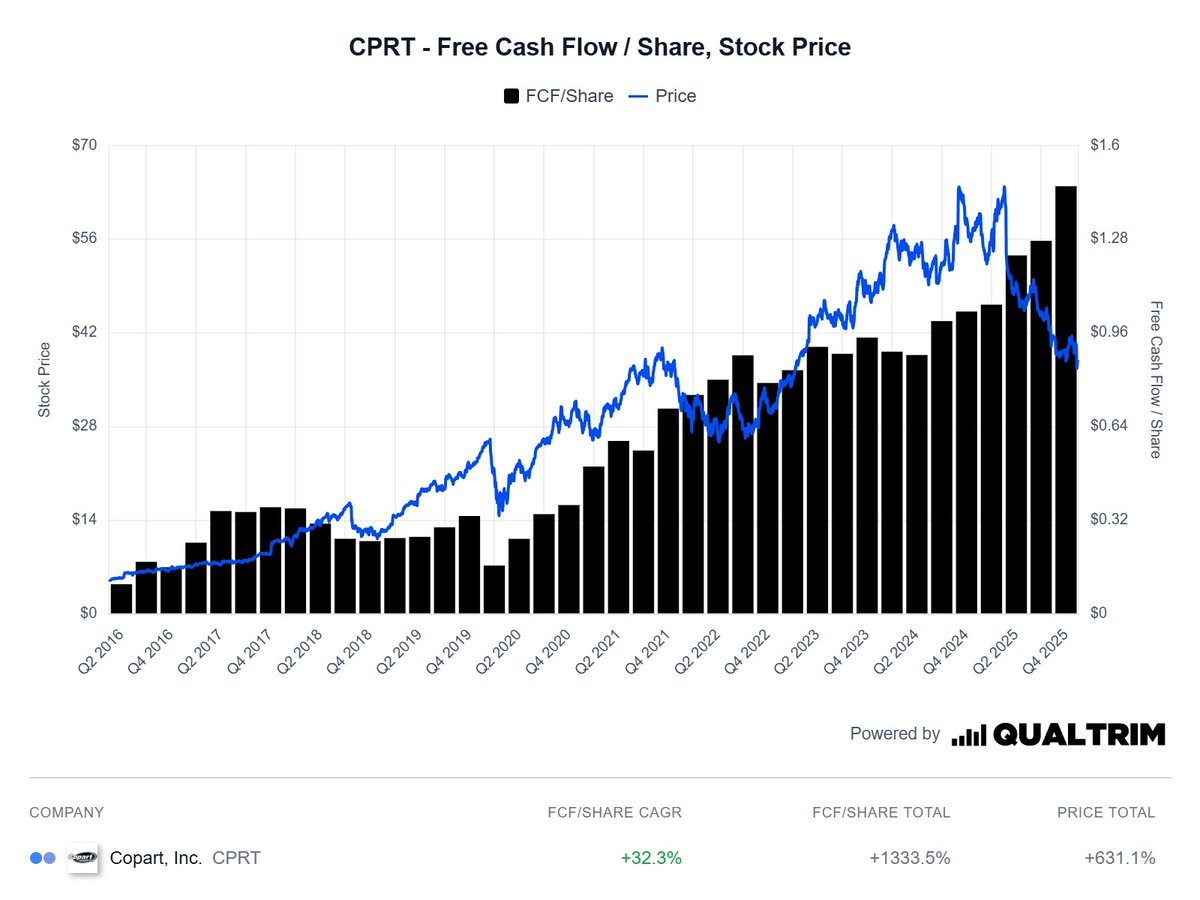

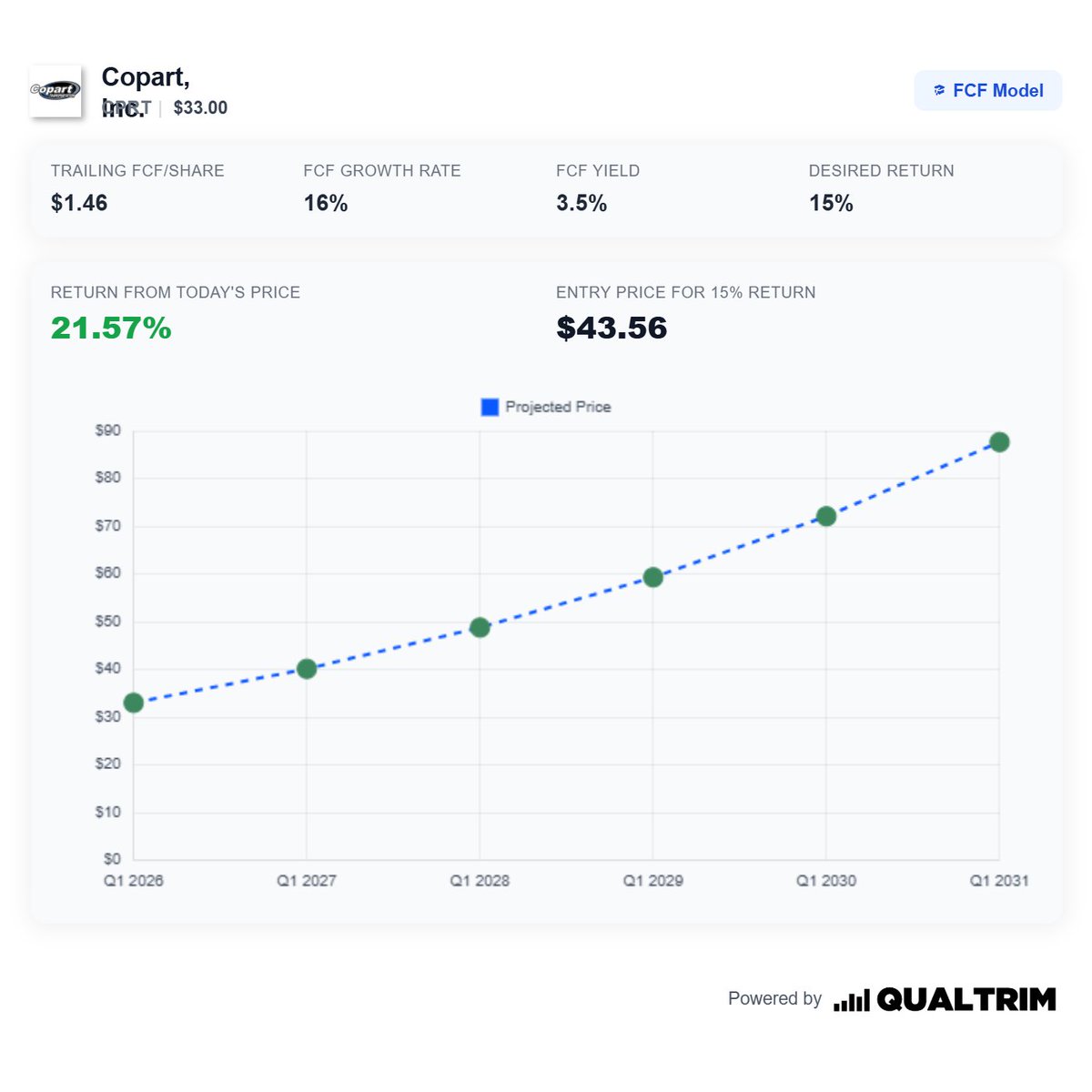

I asked for $CPRT at 20x. I got what I asked for. Now it's up to me to act on it. x.com/i/status/15719…

Are you bullish?

Reddit might be the worlds fastest growing social media platform. - Total Advertiser Accounts: +75% YoY - Advertising business: +75% YoY - U.S. Revenues: +68% YoY - Intl Revenues: +78% YoY $RDDT

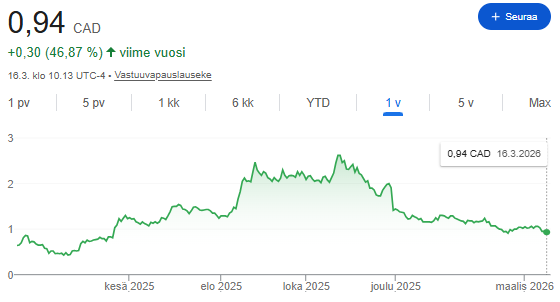

Sold $zomd.v at the average price of 1.57$, up +104% from my cost-basis. Half straight after Q3 earnings were released at 1.63$ and the second half after the earnings call at 1.51$. The thesis was profitable growth, and now the thesis and momentum have been damaged until they return to growth, and they likely will eventually, but I’m not interested in waiting around when there are VSTs and LODEs available. When I got into the stock, it was 50m USD market cap with Q1 being 18.2m and 4.8m of net income, and growing y-o-y and q-o-q, and management was indicating more near-term growth. Insane set-up, only made possible by the heightened tariff fears at the time. And now it’s 109M USD market cap with Q3 revenue at 16.1m and net income at 3.8m, and falling revenue y-o-y and q-o-q, management being hesitant in the earnings call. It’s still cheap based on the P/E and the potential LT growth case, but not among the best R/Rs anymore IMO.

New writeup: Shift4 Payments: A Fintech Compounder Trading Like a Melting Ice Cube 7x free cash flow for a business compounding at 20%+ $FOUR Link in bio