@damnang2 Well written. I’ve enjoyed consuming your content. Keep it up.

English

Super Future Proof

80 posts

@sfproof

Former sell-side analyst; ex-partner at a $20B multi-strat hedge fund.

Maybe for them to announce that their "opportunity pipeline" expanded again while simultaneously missing on revenues. $SIVE

If it's not related to AI, the markets don't seem to care? This $NOW sell-off seems way too aggressive. They've got 600+ customers with an ACV over $5M lol (grew 22% YoY). You don't sign multi-year deals that big if the platform is getting disrupted by AI? Not sure what needs to happen for them to get re-rated. Maybe rebrand to NowAI? I don't have a position, but they're on the watchlist. Financials + guidance are too good to ignore.

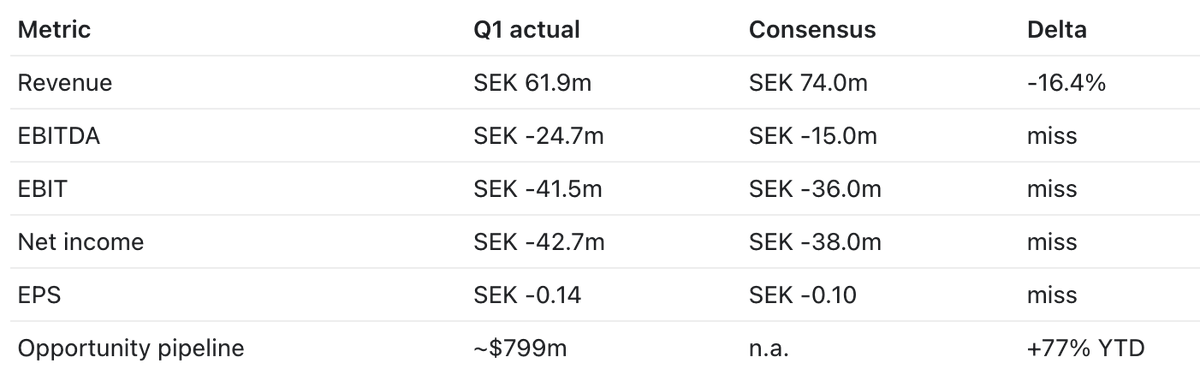

$SIVE earnings were a miss. Net sales fell 22% to SEK 61.9m, adjusted EBITDA was −13.8m and loss widened from −6.0m. That’s why the stock is down. Management blamed the US government shutdown, defense budget delays, and FX, and leaned on a 77% pipeline jump to $799M with 2027 ramps “on track.” Translation: zero current-quarter validation. The bull case is now entirely forward-looking TAM talk and future margins with no timeline.

$SIVE earnings were a miss. Net sales fell 22% to SEK 61.9m, adjusted EBITDA was −13.8m and loss widened from −6.0m. That’s why the stock is down. Management blamed the US government shutdown, defense budget delays, and FX, and leaned on a 77% pipeline jump to $799M with 2027 ramps “on track.” Translation: zero current-quarter validation. The bull case is now entirely forward-looking TAM talk and future margins with no timeline.

Sivers' CEO on the call, "We do not look at competitors when demand far outstrips supply." $SIVE

Holy crap, this is the most bullish thing I’ve heard from $SIVE so far. From earnings transcripts: “We do not look at competitors when demand far outstrips supply” (literally anything they make gets bought) Along with: “We see 60% gross margins in the future” (incredibly high) “We have two technologies that can feed into these three supercycles that are currently going on.” (Holy revenue opportunities) My high conviction CPO/photonics long is $SIVE for a reason.

$SIVE, now down a further 16% since I called the exact top. I have not bought back, I am expecting them to dilute to fund growth. Would be a heavy buyer following either dilution or a very good earnings report. The bull case is extraordinary though - this could very well pump on a bad earnings report.

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups. Don’t miss the next one, come join us for just a $1. milkroad.com/pro/?utm_mediu…

**Verified.** The TradingView charts do look remarkably similar: both show extended multi-year sideways consolidations/base-building, followed by a sharp vertical breakout candle on strong volume that clears long-term resistance (SIVE around March at ~9-10 SEK; CPSH today around $10-11). $SIVE (Sivers Semiconductors) specializes in high-power laser chips for AI data center optical interconnects — a clear tech chokepoint. $CPSH (CPS Technologies) makes specialized metal-matrix composites for thermal/power management in electrification (EVs, renewables) — a supply-chain chokepoint. The technical analogy and thematic parallel both check out.

@AlmaCap114204 I expect it to trade low $60s post earnings unless $SIVE fundamentally reframes earnings pipeline

$SIVE down 11% since I called to trim and rotate to IQE yesterday (up massively today). Could go lower but I’m rotating back a bit today to rebalance my portfolio. Other picks are all also up massively $MDA (did an article on them), $FLY and $ASTS Ps. I expected a pullback on SIVE albeit not this fast, always good to take advantage of the volatility.