@aleabitoreddit I see high volumes on SIVE.SK (35M-55M) so institutions are definitely buying, some might hold short term, some longer term, uptrend still intact.

English

siflower

314 posts

@siflower

economics/finance enthusiast, tennis player, piano student, francophone

This has become one of my favorite photonics plays $CIEN $AAOI $LITE $COHR $LWLG Ciena’s core business is in high-speed optical networking. One of the most important AI opportunities for them right now is scale-across networking. Think connecting data center to data center so they can operate like one larger training cluster without being limited by physical walls or local power constraints. Ciena is already seeing extraordinary demand here. Management said three major hyperscalers are deploying its optical solutions for these distributed training environments. But they are not stopping at scale-across. They recently announced the Vesta 200 6.4T optical engine, a new high-density, low-power optical product aimed at scale-out and next-generation scale-up architectures inside and around the data center. If they execute, that expands the story well beyond traditional WAN/DCI and pushes them further into the AI data center buildout. They gave a really nice post-earnings opportunity around the mid-270s. Now the stock is back around 360. There are always opportunities out there.

$SIVE is the upstream laser supplier for CPO and Silicon Photonics. They're the likely $COHR / $LITE type future light source for: - $AMZN Trainium Clusters - $MSFT Maia Clusters and possibly other hyperscalers like $META MTAI and $GOOGL TPU clusters. At a ~$200M MC. Relational Mapping (speculative): $SIVE (light source) -> $POET (optical interposers) -> $MRVL (Likely Celestial Captive) -> $MSFT Maia + $AMZN Trainium. $SIVE (light source) -> Ayar -> AiChip -> $AMZN Inferentia/Trainium $SIVE (light source) -> Enablence -> O-Net -> ? Asia Hyperscalers _ Ongoing: $SIVE (light source) -> Ayar -> GUC -> ? (Google $TPU) $SIVE (light source) -> Ayar (TeraPHY/SuperNova)-> Wiwynn (captive CPO) -> ? ( $MSFT, $META historically Wiwynn's largest clients). Because of captive models like $MRVL Celestial, they get a free ride. However, they do compete multi-source ELS against Lumentum, Coherent, and $MTSI with Ayar and win anyway in merchant models. But they win either way. For high-volume production ramp up, a large part of it depends on the ongoing Win semi qualification, but this will likely be a large indicator. Again supply chain BOM is extremely confidential. $AMZN will never tell anyone "Hey, we use $SIVE ". But if you put 1+1+1+1+1 together, you can piece together the likely suppliers. Most people see "Poet Starlight" uses $SIVE. Or Ayar uses $SIVE. But don't map all the multi-hop relations to see where they end up. I do think $SIVE is an extremely undiscovered opportunity as the next possible mini $LITE for Silicon Photonics at $200m MC. As they're the likely upstream laser supplier for hyperscaler supply chains for future CPO/Silicon Photonics scale up with cw dfb lasers and scale out with laser arrays.

The upcoming CPO / Silicon Photonics Bottleneck Cheat Sheet: $SIVE, Sumitomo, $LITE, $COHR, $AVGO, $MTSI, $AAOI - Light Source (CW DFB Lasers) $TSEM, $GFS, $UMC, $TSM, $INTC - SiPh foundry $NOK, $CIEN, $CSCO, $COHR - DCO $HIMX, FOCI (3363.TWO) - Micro-lens + Fiber Arrays $POET - Optical Interposers $SOI, $AXTI, Shin-Etsu - Substrates $FN, $ASX, Innolight, Eoptolink - Optical Packaging and Assembly $MTSI, $SMTC, $MRVL, $MXL - Analog/Mixed-Signal ICs $LWLG - Speculative Modulator Materials. $GLW, $APH, $TEL, $FIT, Fujikura - Connectors and Fibers $FORM, $KEYS, $VIAV, $AEHR- Test & Measurement $BESI, $SMHN, $ONTO, $CAMT - Advanced Packaging & Hybrid Bonding Many are private companies from Lightmatter, Ayar, Ranovus and others. Now... Everyone is asking... How do you profit? If you look at the forecast for CPO TAM, it's a straight line up, and next year is inflection point for CPO mass deployment. The alpha is capturing the rotation: From the current EML bottlenecks ( $LITE, $COHR type) to SiPh / CW DFB architectural winners for CPO. Highest upside potential are the ones that aren't included in current cycles. But that are in the next. Companies like $SOI, $SIVE, or $AEHR are perfect examples. Ride the current pluggable bottleneck like $AAOI. But the alpha is frontrunning institutions with the next CPO bottleneck. The capital rotation is inevitable.

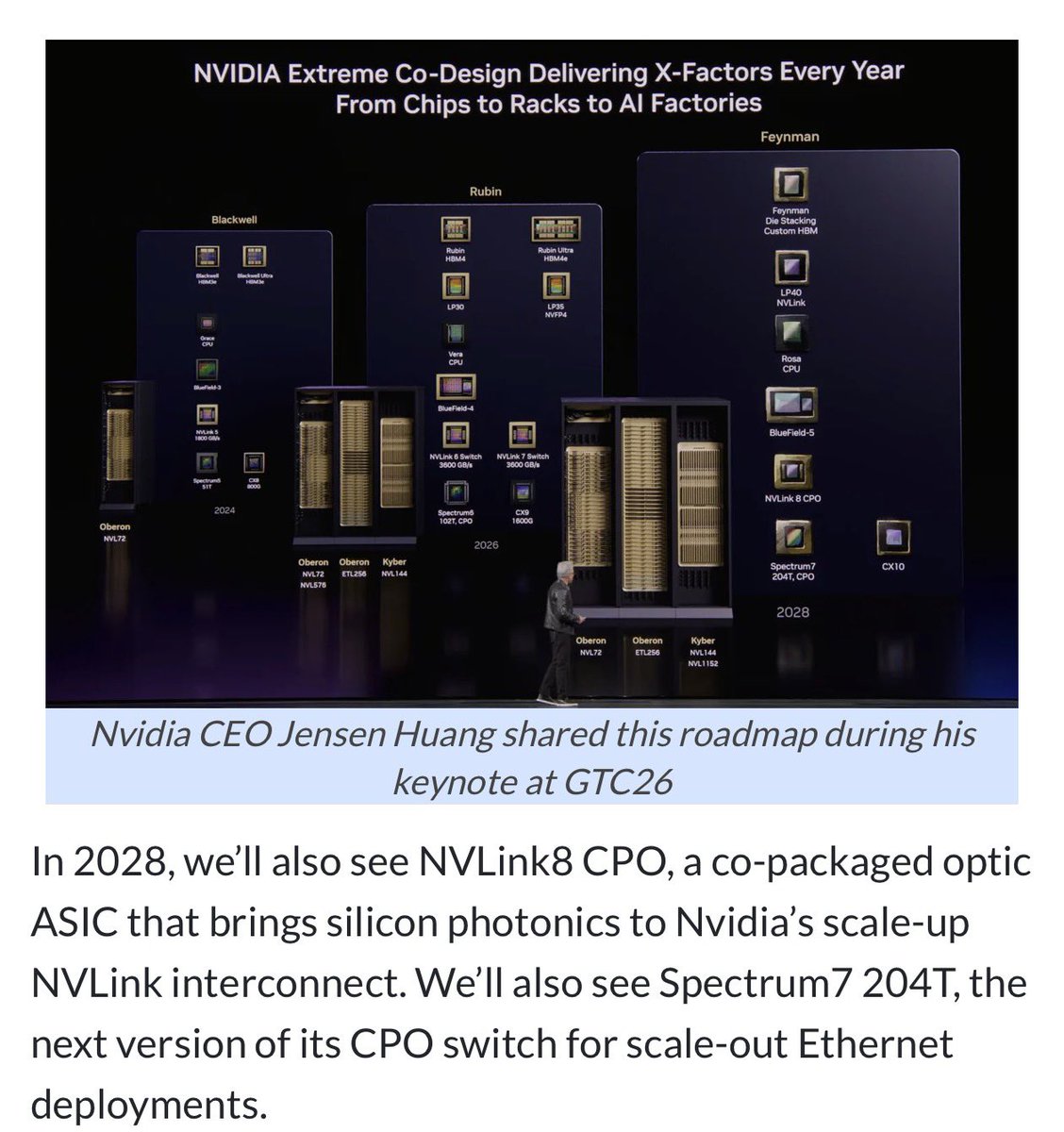

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.