SimpleHuman2025

4K posts

SimpleHuman2025

@simplehuman2024

🇺🇸 is the greatest country on planet earth. you cannot convince me otherwise. critical thinker, simple life. 😊

Katılım Ağustos 2019

894 Takip Edilen256 Takipçiler

$100K invested in $VOO = $1,090/yr in Dividends

$100K invested in $SCHD = $3,410/yr in Dividends

$100K invested in $ICAP = $9,060/yr in Dividends

$100K invested in $OVL = $10,500/yr in Dividends

$100K invested in $QQQI = $13,960/yr in Dividends

Which do you prefer?

English

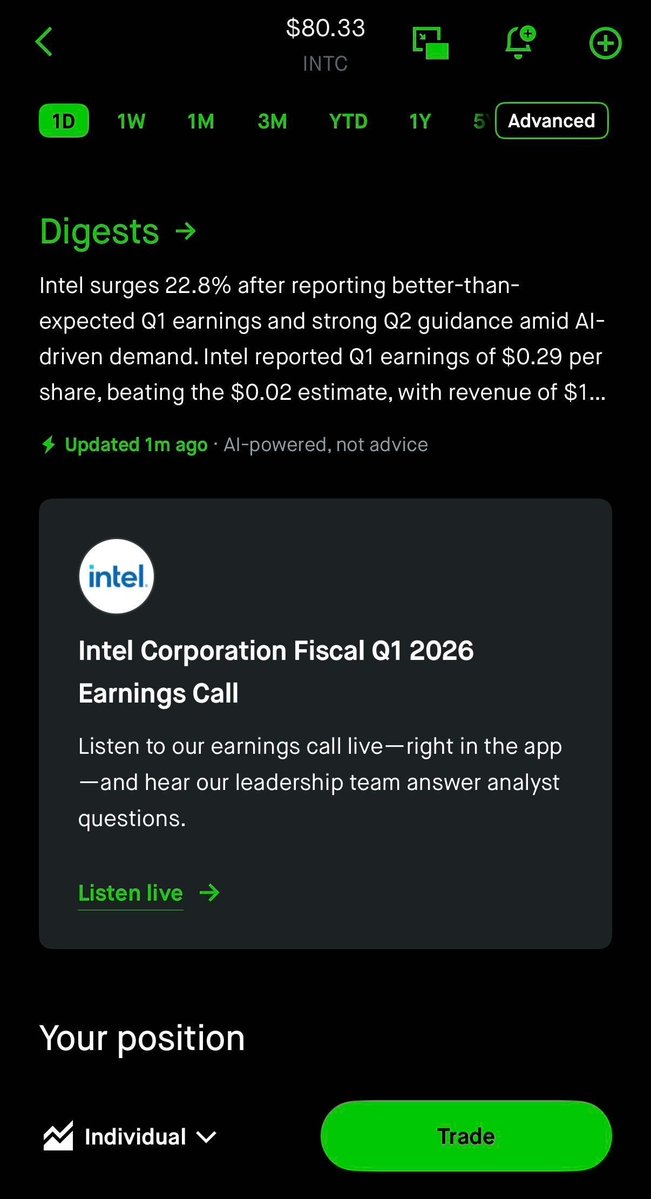

We've built a way to listen to earnings calls live, directly in the app. Check it out!

English

@AnthonyDo @Dr_Crossroads @rajuvamsi007 @grok CEO is clearly not confident about expansion anytime soon.

If & when that happens, one can always buy back in. Why to continue holding when one could make $ elsewhere?

Anyways, to each on its own. Good luck to you.

English

@simplehuman2024 @Dr_Crossroads @rajuvamsi007 @grok Sure but once Robotaxi takes off, the ROI will be more than the last decade of investments

English

@Dr_Crossroads @simplehuman2024 @rajuvamsi007 @grok 3 years from now none of them will outperform Tesla. You’re underestimating the Robotaxi

English

@Investanswers Stop pumping! Elon said it won’t be materially scalable in near future.

English

The future is here! 🚖🤖

No steering wheels.

No pedals.

Fully autonomous Cybercab right out of the gate.

Tesla@Tesla

Purpose-built for autonomy Cybercab in production now at Giga Texas

English

Elon just now: "limiting factor for FSD expansion is validation"

English

Hearing this same story since v11.

AJ Investment Research@alojoh

Elon just now: "FSD v15 will be a complete overhaul of the software architecture"

English

@aelluswamy Yesterday Elon said the software is not ready for volume scale up.

English

@rajuvamsi007 @Dr_Crossroads @grok If you had explored other options and invested with the companies I mentioned a year ago (thinking about going forward), you’d have made a lot more.

English

@simplehuman2024 @Dr_Crossroads @grok It's about going forward.

No one knows what's in the future.

Let's wait and see!

I for one will continue to invest in the smartest innovator of humanity!!

English

$TSLA I've sold the last of my Tesla position.

Tesla has been in a weird place for me for a while. I love the product. I am enamored with how amazing FSD (in a HW4 stack) is, and how excellent the vehicle is. My wife and I aren't likely to buy any vehicle that isn't a Tesla, and I'm already thinking of that nice upgrade (3-4 years from now) for my '22 Model 3.

I also would love to own an Optimus at some point. I love the vision, the vertical integration, and wouldn't bet against Elon.

Yet the stock is not the company. Tesla has always traded at a premium, but that premium is increasing over time. That's fine if it's in anticipation of significant future acceleration, but it's questionable when that happens.

On the call, they stated, “over time, we expect our hardware-related profits to be accompanied by an acceleration of AI, software and fleet-based profits,” but were effusive on the dates. That's probably for the best, as Elon timelines usually need to be extended.

Gross margins have improved, and the P/FCF looks like it's improving, but with the CapEx they're needing to do, this ratio will soon be negative.

I don't mind buying a stock with extreme multiples, but I see easier opportunities with clearer runways for acceleration elsewhere.

Tesla hasn't been a meaningful position for me for over a year, but I'm out for now. I'll still be rooting for the company (and shareholders) even while hoping the stock comes down to more reasonable levels where the R/R fits my portfolio better.

English

@rajuvamsi007 @Dr_Crossroads @grok LMAO. Why wait till 2026? Just go back and compare past year’s performance.

English

@simplehuman2024 @Dr_Crossroads @grok At the end of 2026. Remind me how the above stocks will perform.

English

@rajuvamsi007 @Dr_Crossroads $MU

$ALAB

$BE

$GOOG

$MRVL

$ARM

I can keep going

English

@simplehuman2024 @Dr_Crossroads Which one?

Give me two of your best...

English

@rajuvamsi007 @Dr_Crossroads There’re plenty of stocks (from energy, networking, Chip, memory and so on) that’ll boom from AI acceleration. TSLA is not the ONLY ONE. 🤷🏻♂️

English

@Dr_Crossroads "I see easier Opportunities"

What are those? I don't see any!!

English

@bradsferguson That’s not what he said. LOL

He’s paving the way and explaining to everyone why merger is needed. Both will merge in couple years.

English

Elon to $TSLA shareholders,

‘You don’t get Terafab, SpaceX does.’

‘and Tesla is going to do the research for SpaceX.’

Doesn’t seem right.

AleXandra Merz 🇺🇲@TeslaBoomerMama

I just may have the solution to avoid in the future all these headaches ... 😏

English

@nerdalert My exact thought when I heard him say that. Long $MU

English

Elon saying memory is the key reason HW3 won’t work with FSD.

$MU and the other players are going to be beneficiaries of a secular increase in demand for memory. You don’t fix this bottleneck just with better algorithms.

English

@TSLAFanMtl 💯 the honesty. I can decide my investment strategy accordingly. 🤷🏻♂️

English

@mikepat711 And maps. They’ll finally fix the maps in V15 😄

English

I don't care about Tesla stock anymore this year because who the fuck knows, but I am excited to see what the V14.3 rewrite does to the next series of FSD updates.

And they said V15 is on another level? wtf does that even mean? 14.2-3 are already fuckin nuts. Does it mean it's going to understand signs better? because that's literally the only weakness I can think of at this point

English

My thoughts on Tesla’s Q1 2026 earnings:

It’s become clear that 2026 will not be the breakthrough year that Tesla investors would’ve hoped - at least from an earnings perspective.

There’s been a softening of language on the biggest levers that Tesla will pull to materially increase its valuation.

Robotaxi scale was softened to “depends on what you mean by scale”. Optimus in any meaningful volume is not happening until 2027 due to the time it takes to revamp the Fremont line (understandable). The showcase of the Bot is being reserved until summer of this year - which could get pushed out again.

On the positive end, demand for Tesla vehicles appears to be increasing, and adoption of FSD is accelerating. This can be seen in the auto margins, which allowed Tesla to have one of their best in a while in a seasonally depressed quarter.

What we should see is as Tesla’s production re-accelerates, the cost per unit of production will come down, while the net price per vehicle will go up as more and more people purchase FSD subscriptions. This means that margins on the auto business should continue to rise.

This should give Tesla the best large-scale auto margins in the world into 2027. This should materially increase again when Tesla releases Unsupervised FSD for the HW4 fleet, which my guess is will come at a premium. I find it hard to see Tesla charging $99 a month for a personal chauffeur where you no longer have to pay attention. The premium on that is far greater. Imagine being able to do whatever you want in your car while it takes you to point A to point B. Big deal!

Another positive (depending how you look at it) is that there’s maximum clarity on HW3 vehicles not achieving Unsupervised, and Tesla will a) offer a discounted trade-in rate on HW3 vehicles that purchased FSD outright and b) will work to upgrade the vehicles to HW4 so that they can be Unsupervised. This is because a car that is a Robotaxi is worth FAR MORE than one that isn’t, and even if the cost to retrofit a HW3 car was $10k+ or more, Tesla would make the money back (and then some) in fares.

Basically a no brainer, if the path for an upgrade actually exists, which now we’ve gotten confirmation that there is.

In the next 12 months, I think Tesla’s biggest catalyst (by far) is the adoption of FSD on a growing fleet of vehicles that will eventually go unsupervised, which will give Tesla recurring revenue at 80%+ margin on a fleet of vehicles that will continue to grow over time, and as regulations allow it.

If you fast forward to the end of 2027, Tesla should be able to have over 5 million cars generating at least $99 per month in recurring monthly revenue, almost all of which drops down to the bottom line, because the cost of the hardware and compute is already baked into the business. That’s roughly $6 billion in net income per year added to the bottom line, and growing. That’s ~166 P/E at a $1T valuation on growing software revenue AND margins. To me, that seems pretty fair. Honestly, might even be undervalued. Just look at Palantir.

This is while the company needs to invest heavily on CAPEX for Optimus, Cybercab, and Terafab, all of which are extremely important for the company’s long-term trajectory.

The question now becomes how fast can Tesla materially increase FSD revenue at 80%+ while it waits to ramp Robotaxi & Optimus.

Overall, IMO, very good quarter for the long term prospects. The acceleration in FSD adoption is a big signal that says Tesla is capable of capitalizing on recurring revenue, and as the software gets to unsupervised, it should increase materially in the coming quarters.

But as far as the next 12 months go, it continues to be a waiting game on the biggest levers for Tesla.

NFA.

$TSLA

English

English

English

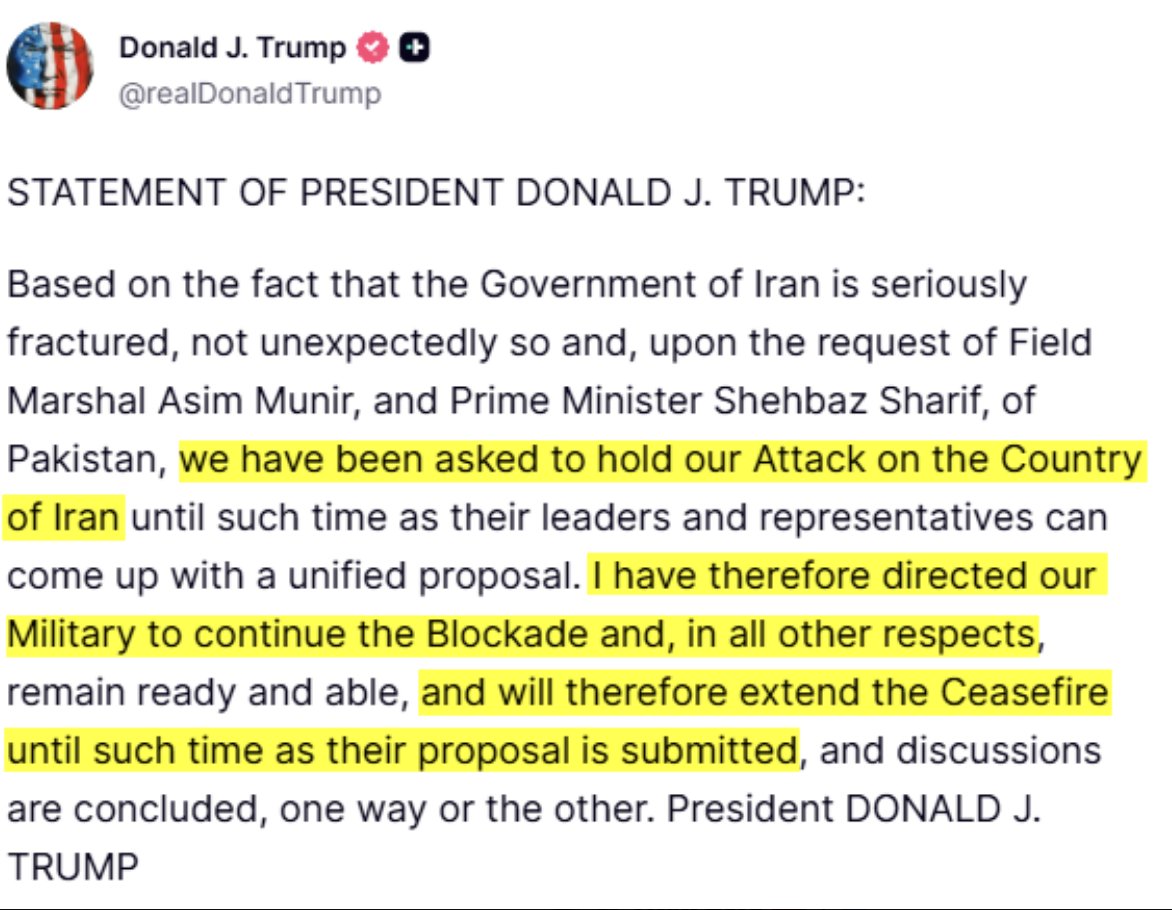

Trump Always TACOs on a Tuesday.

Amazing!

He just extended the ceasefire. There are no Red lines.

English