Surya Singh

228 posts

You have $100K and must invest it in one of these options. You have access to Korean equities thru IBKR. Bonus points for intelligent comment justifying your vote.

English

@ParadisLabs How can 41 mil dollars be a record from their biggest customer at the same time you’re predicting 850 mil revenue .

English

Told you all that $AEHR looked cheap...

Up 17.28% today to $3.46B MC.

Basically a ~3x since my V1 post a couple months ago.

My personal estimation is $10B MC by around Q1 2027.

For very rough napkin maths from post-Earnings:

- $AEHR have new 240 systems/year capacity

- By hitting 30% consumables target, they can generate ~$850M+ rev

- Applying standard high growth 12x–15x P/S multiple = valuation range of $10B - $13B

And just to remind you:

They got a record $41M order from their lead hyperscaler customer.

With the CEO saying:

"We have significant additional customer demand forecasted over the next few months across multiple markets, including... photonics wafer-level burn-in, and SiC & GaN semis production burn-in"

And some of this demand converts into actual bookings by the end of the year.

Kinda bullishhh

Paradis Labs@ParadisLabs

And just like that. Markets front running a stellar earnings? Regardless, still looks "cheap" for a company sitting in such a crucial bottleneck w/ a massive order book.

English

@v3wanu There’s $DPRO as well which is I think 40-50 percent down

English

前面提到Serenity带单,但大家也别把他神话了,别光看他最近几个,跟单就要有被献祭的准备

比如他跌的最狠的 $DFLI ,做美国本土磷酸铁锂电池的,从他的喊单位,跌了差不多90%

他2025年10月8、9、10发了6条x,特别是其中一条: $DFLI 是一只有望暴涨十倍的妖股,目前市值仅8100万美元

他喊单前,这股已经从底部拉起来10倍了,喊单后第3天有一次跳空涨,然后开始无尽下跌

我就不揣测他更多了

中文

@Ren_aramb I’ve been in at 13 once and out at 13 when it retracted back from 20. Now have entered again few days back at 12 2/3 quantity but I’ll take it.

English

$TRT is up 17% and this time I think it will stick given the new information that has come up.

I shared this information with my subs on Saturday so that the could make the best informed decision.

Some stuff is hidden other is just waiting to be found in plain sight.

Hopefully we have a great community with eyes everywhere.

Credit where credit is due follow @athuinvests for great content and smart and precise information.

Ren@Ren_aramb

$TRT - TRT just got a lot more attention over the weekend, I am loading up. First, look at who is showing up in the filings. 26 hedge funds and institutions now hold positions as of Q1 2026, with 13 opening brand new positions -- a 550% jump in new money. Marshall Wace, Citadel Advisors, Renaissance Technologies, and Vanguard are all on the buyer list. When this many sophisticated funds open positions in a $140M micro cap at the same time, someone is usually positioning ahead of orders the rest of the market has not priced in yet. Now the business. Trio-Tech International is a semiconductor reliability testing and burn-in company. Singapore-based, back-end focused, 65 years operating through cycles. AI GPUs and EV chips cannot ship without rigorous reliability screening. $TRT runs the burn-in in Southeast Asia and sits exactly at that bottleneck. The numbers from the latest ER are accelerating, not just growing: Q1: +58% YoY. Q2: +82%. Q3: +124%. What caught my attention specifically: a $5.3M burn-in board order for a next-gen AI GPU platform shipping over the next 2-3 quarters, a $2.5M automotive IDM burn-in ramp through 2026, and $7.8M in confirmed orders total. Revenue run rate approaching $65M annualized. New 104K sqft facility coming online in Malaysia. Balance sheet clean -- $16.5M cash, $1M debt, debt-to-equity 0.11 on a $72M market cap. DSO dropped from 106 to 70 days during the ramp. The honest risk: gross margins compressed hard, 27% to 14% in SBS. Incremental revenue is lower-margin final testing work, so the earnings inflection has not matched the revenue inflection yet. One metric I am watching closely: SBS gross margin recovery toward 20%+. That single number determines whether this re-rates further or stalls. 237% in a year. Still early if margins follow revenue. When institutions load up, I listen. Do you? Bullish $TRT.

English

@SlarkTrader lol you literally said confirmed. It has been on my feed since last 2 days but nobody has any confirmation

All that has been said is “company with highest qualification requirements”

Anyway I’ll wait for the link

English

@singhsurya1012 no link yet, it was visually and verbally confirmed at the general meeting. Links and PM will follow soon

English

$NVDA Nvidia confirmed customer at this evenings general meeting ✅🚀

This can get HUGE

SlarkTrader@SlarkTrader

Here is my current gameplan after $SHT going parabolic reaching 75 SEK -> Position size -> Price target -> Profit taking -> Exit plan Everything shared in substack slarktrader.substack.com

English

Julius, please don’t let the LLM do all the thinking for you 🙏

I would love to address your concerns

Let me just answer them 1 by 1

1. Claude is confusing Grid to building power with Rack to chip power

The SST stage happens outside the server

Yes, Navitas sells industrial SiC there, but that is a highly competitive, commoditized market

POWI isn't trying to power the data center building, POWI lives directly inside the NVIDIA compute tray

My point is POWI's 1700V GaN bypasses SiC entirely

2. Just because an engineering workaround is "standard" doesn't mean it's optimal for a dense AI server

Yes, NVTS achieves 800V to 6V power delivery board with 650v but they have to use 16 separate FETs arranged in a stacked configuration (this is very bulky) in a data center that is deprived of space it’s more efficient to use a single chip

Which will you choose the single chip or a configuration of 16 stacked chips?

3. Claude actually just confirmed my thesis lol

Stages 1,3 & 4 is where all the competition is from, Infineon, TXN, VICR, and on semi which sacrifices margins

Stage 2, where POWI is a one man band

Every single kilowatt power supply brick must have an independent aux unit to run the internal processors, telemetry sensors, and liquid pumps safely

Since POWI owns the only single chip 1700V GaN solution that can safely tap the 800V line and drop it down to 12V/5V streams NATIVELY, they have an uncontested monopoly in that specific gatekeeper socket

4. Ask your LLM again if any of those companies listed offer a SINGLE chip, integrated 1700V GaN flyback switcher with multioutput regulation that’s actually in volume production

See what you get back

If you design a rack using Infineon or TI components, you have to buy a discrete high voltage switch, a separate driver chip, an isolation transformer, and external DC-DC post regulators

POWI’s InnoMux 2 consolidates all of those downstream stages onto a single piece of silicon

Lmk what you think brotha

English

Today I added to my $POWI (Power Integrations) position, planting my flag in what I believe will be a massive Capex wave transforming the entire power semi space

Currently, $NVTS is getting all the love which is fair, however...

With the release of the specs for the upcoming architecture of the 800V Data center for VR200 it is quite clear that there will be a huge demand for high voltage GaN rather than high speed integration GaN in which NVTS provides

The server rack will be scaling from 120 kW to 600 kW (!)

The core issue isn't going to be how fast a chip can switch, it will be about how much raw voltage can actually survive

Navitas flagship GaN tech (GaNFast and GaNSafe) maxes out at 650V

It was originally designed for high speed switching in consumer electronics and lower volt apps not not megawatt scale AI infrastructure

A 800V data center will instantly destroy a lone 650v chip. To participate, NVTS has to combine lower voltage components in a highly complex stacked build which creates clunky workarounds, wastes physical space, and introduces severe points of failure

POWI's chips doesn't require these unnecessary workarounds

Their InnoMux-2 is the ONLY chip on earth that features a 1700v switch on a single piece of silicon

When NVDA starts to roll out these high power racks, a single PowiGaN chip will be able to handle it natively with an integrated safety buffer to spare

Which is IMPORTANT because in the case of power spikes, POWI's voltage leaves a 900v buffer that is built to handle the power spikes without creating a power failure

Let me put this into context for you guys

If NVDA said F it let's skip 800v and go straight to 1200v DC POWI's 1700v chips are still able to handle the power consumption TODAY still with a SAFETY BUFFER

Here is why $POWI is still undervalued:

They didn't build the 1700v chip for AI

They originally built it to handle unstable power grids in developing markets and heavy electric vehicle architectures

When $NVDA shifted the Vera Rubin architecture to an 800V DC baseline, their engineers realized they needed a battle tested SINGLE chip solution to safely drive the background cooling infrastructure (fans, liquid pumps, and logic controllers)

POWI was the only company in the world that had spent decades perfecting single chip high volt integration.

That deep reliability is why they are co-designing power blueprints alongside NVIDIA TODAY

If you track the projected power infrastructure spend per AI rack, the metrics are going vertical:

Current (GB200): $36,000 per rack

2026 (Vera Rubin): $76,000 per rack

2027 (Vera Rubin Ultra / Kyber): >10x increase (Over $360,000 to $398,000+ per rack)

POWI's TAM is literally multiplying right before our eyes

Currently, their entire business is still being dragged down by legacy

When you look at $POWI at surface level, you see flat YoY revenue, lower GAAP margins, and a high P/E ratio

but don't be fooled, their PowiGaN product division is growing at over 40% annually and will continue to accelerate as the VR is deployed

In February 2026, POWI even did a 7% workforce reduction to reallocate that money toward scaling DC revenue

You are essentially paying a cyclical multiple for a boring legacy appliance business, and getting a structurally protected, high voltage AI pure play for free even after the initial move

From a TA perspective, just look how coiled it is. Currently trading under it's HTF downtrend line while simultaneously allowing moving averages to play catch up

It's only a matter of when not if imo this breaks out

NFA. Research purposes only.

bryan@BryzonX

One of my fav new finds is $POWI An Energy + Data Center company with an existing $NVDA partnership/design win for the Rubin deployment Here is what caught my attention: The new chip cycle now requires so much electricity that existing systems can barely handle the load with how much compute a GPU demands. To survive, all data centers are upgrading to a new 800V system, a massive electricity intensive buildout. $POWI is currently the ONLY company in the world that has the tech to offer 1700V GaN chips giving them a huge moat. These chips allow these 800V super racks to run smoothly requiring less copper and more space meaning lower upfront costs and more revenue per square foot for hyperscalers like $META and $GOOG One of my favorite reasons why I'm confident they can deliver is because their GaN chips have already been proven in the harshest environments on earth in automotive, so hyperscalers ( $META, $GOOG, $AMZN ) can skip the years of testing and plug POWI’s tech directly into their multi-billion dollar data centers today. The "closest" competitor is $NVTS but they have to stack multiple smaller 650V chips together to handle the new 800V data center standard, which multiplies uneccessary points of failure. POWI's GaN single chip makes their power systems 50% smaller, more reliable, and more convenient for $NVDA to build into their racks. The reason for the current mispricing is because they are at an inflection point transitioning their legacy appliance business to an AI data center infra business. Confirmed by cutting 7% of employees to reallocate capital to their growing data center business, Under the surface, you will see slowing growth, however their industrial business is growing 40% YoY which is expanding their margins and I expect this to keep revving up as a higher % of revenue as Rubin starts to deliver to customers bringing in some serious $$ that i believe will demand a complete rerating. Currently has a $2.6B MC, zero debt with $250M in cash and multiple analysts believe that they have a 313 day supply of existing chips that were meant for appliances, but are being strategically gatekept for the potential data center demand in the back half of 26'. This would be huge because they expect a lot of demand coming their way. Plus they have a 1.81% dividend so they are already cash flow positive! I started a position today with a solid weighting. NFA. DYOR.

English

@Million_Sancet Reminded me of this very good company “Aerotyne International”

It is a cutting edge high-tech firm out of the Midwest awaiting imminent patent approval on the next generation of radar detectors that have both huge military and civilian applications now

Everyday new company

English

New quite speculative idea but with an absurdly large potential

Of course, it is Swedish, taking advantage of the boom of the US MOU

That makes 4 Swedish companies that I own hahaha

The company is $OBDUb Obducat and its thesis is as simple as it gets

$OBDU positions itself as a key equipment manufacturer for the scaling of Co-Packaged Optics (CPO) in AI data centers

It uses NIL (Nanoimprint Lithography), a technology that physically “stamps” nanoscale optical structures (waveguides, lenses, etc.)

In a much faster, cheaper, and more scalable way than traditional semiconductor lithography

It is specially designed to produce photonics in large volumes

The imminent PFAS restriction by the ECHA

Will force the semiconductor and lithography industry to stop using traditional coatings

This directly affects critical processes such as the manufacturing of InP lasers

From companies like $SIVE and essential for the AI data center infrastructure like $NVDA, Ayar Labs etc

While the sector looks for solutions for the 2026–2027 period, $OBDU has a mature and proven technology

They signed a 3 year Foundry Services contract for a minimum of SEK 115M, almost 4x the previous contract in defense photonics

This transforms them from machine sellers to direct component producers, generating recurring revenue and positioning them as a strategic bottleneck in the optical supply chain

The risk here is execution and market capture

It is also worth noting that being so small, it will require repeated dilution to raise capital for scaling

But as a more speculative play with a lower % of capital, the potential is more than worth it

English

@Ren_aramb Fair enough. My biggest struggle has been reducing the number of stocks.

English

$NVTS I’m almost 150% up in this position in less than a month.

But it’s not just $NVTS. I was telling my subs yesterday that today every power semi under the sun would be moving up. You can make smart money even if you don’t pick the “best” stock when a whole sector is ripping.

$NVTS -- Next-generation GaN/SiC power semis for AI data centers

$AOSL -- AI and EV power semis, broad end-market exposure

$POWI -- Efficient AC-DC power conversion semis

$WOLF -- Silicon carbide wafers and power devices for EV/industrial

$VICR -- Ultra-high-density power modules for AI servers

$VSH -- Discrete MOSFETs, SiC modules, and passive components for auto/industrial/defense

Bullish Power Semis

Bullish $NVTS

Ren@Ren_aramb

I’m now long $NVTS Navitas is one of the more interesting power semiconductor re-ratings happening right now. Rewind to early 2025. NVTS was a sub-$2 stock. Mobile charger revenue collapsing, FY2025 revenue fell to $45.9M from $83.3M the year before. Gross margins underwater on a GAAP basis. Legacy business in secular decline. Management quietly built the pivot through 2025 and Q1 2026: 1) May 2025: NVIDIA 800V HVDC collaboration for Kyber racks and Rubin Ultra 2) Q4 2025: $237M cash on the balance sheet, minimal debt 3) March 11: New CFO from Lattice Semi, mandate to reach profitability 4) March 16: 800V to 6V GaNFast power delivery board unveiled at NVIDIA GTC 2026, eliminates the 48V IBC stage for MGX racks 5) April 13: Ex-Broadcom SVP joined the board (compensation + steering committees) 6) $450M design-win backlog NVTS is embedded in AI rack power delivery, solving the hardest efficiency problems in data center design. +55% in 5 days. Still early in the re-rate if the AI power thesis holds.

English

@athuinvests Jabil was not vertically dependent on a single laser supplier at 800G. What makes you think they will for 1.6G?

To depend on one supplier is a stupidity no mature company will do that we both know this

Its a codevelopment announcement not an approval but soon revenue will speak

English

@singhsurya1012 They are the only ones in the program bro. Chill… and yeah, when ramps start scaling, the revenues will kick in.

English

People underestimate how bullish $SIVE x $JBL tie is for their 1.6T optical transceiver program and the overall industry.

They selected $SIVE as their primary laser supplier for the program, mentioning that these transceivers are going to provide them with a “dramatic moat” & incremental opportunities with hyperscalers.

Jabil has connections across the semiconductor industry as an EMS company. 100 sites in 25+ countries & 400+ brands as customers for manufacturing.

End-users (potential):

- $GOOGL, $MSFT, $META, $AMZN (Hyperscalers)

- $CSCO, $ANET, $NOK (OEMs)

English

@asianinvestors TRT is speculative after investing in SIVE. What a funny guy

English

After doing a bit of DD, I have just initiated a small position on $TRT pre market.

Thesis is strong, but still a speculative buy. I'll be digging into it deeper this week.

Trading about 2.5x P/S, 140M MC

Revenue growth accelerating rapidly. And I don't have any positions in OSAT sector. Only about 2% of port.

I heard about it from @athuinvests so check his page out for full thesis

English

@BlockFlow_News I doubt any of these will hold it till the end of 2026. These are smart people who don’t hold bags they just past it to the next retailer

English

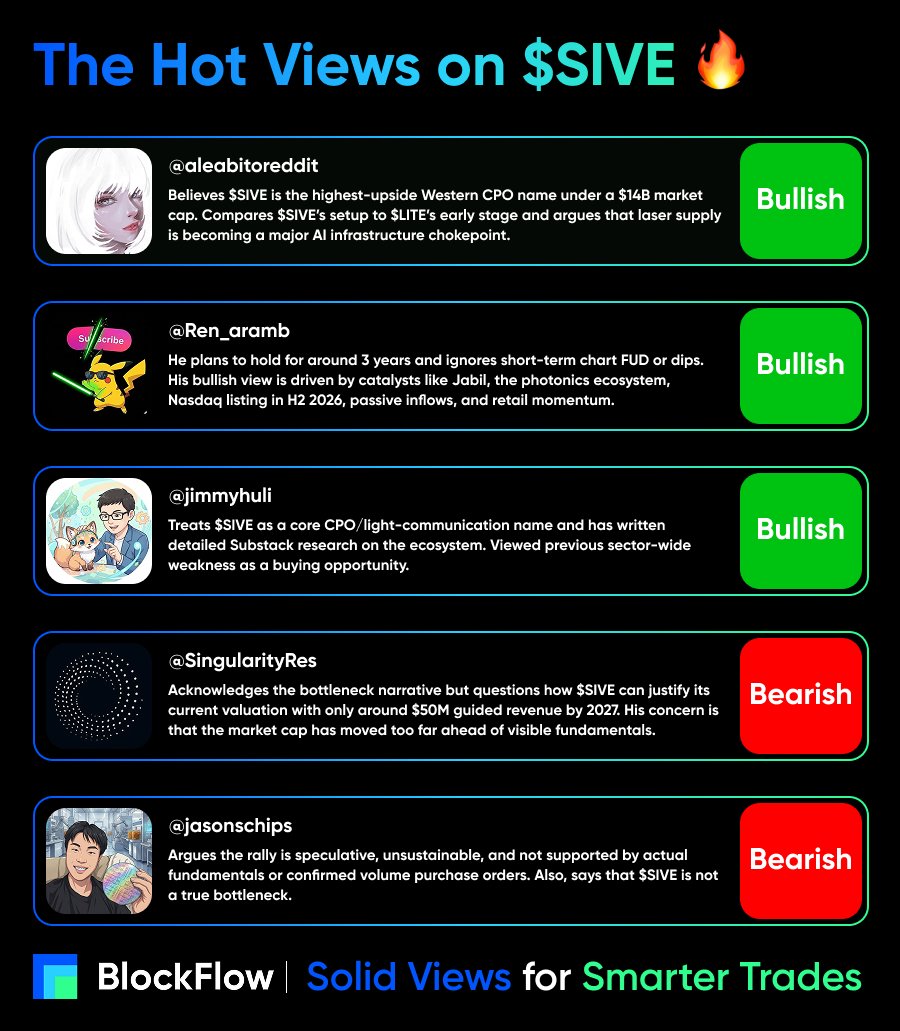

$SIVE is now up +1,857% YTD 🚀

The Swedish-listed AI photonics stock is becoming one of the hottest names in the CPO trade, with a potential Nasdaq US listing now acting as the next major catalyst.

Because of this, its financial report was pushed from May 20 to May 29.

Narrative-wise, bulls see $SIVE as a possible bottleneck in AI infrastructure, supplying laser tech for the next wave of optical data centers.

But after an insane run, the debate is getting louder.

> Some see an early AI photonics winner before US institutions enter.

> Others see a momentum trade priced way ahead of fundamentals.

Here are the hottest bullish and bearish views on SIVE right now:

🟢 @Ren_aramb

Plans to hold for around 3 years and ignores short-term chart FUD or dips.

His bullish view is driven by catalysts like Jabil, the photonics ecosystem, Nasdaq listing in H2 2026, passive inflows, and retail momentum.

🟢 @aleabitoreddit

Serenity is the loudest and highest-conviction SIVE bull, known as one of the original callers on WSB/X.

Believes SIVE is the highest-upside Western CPO name under a $14B market cap.

Compares SIVE’s setup to $LITE’s early stage and argues that laser supply is becoming a major AI infrastructure chokepoint.

🟢 @jimmyhuli

Treats SIVE as a core CPO/light-communication name and has written detailed Substack research on the ecosystem.

He viewed previous sector-wide weakness as a buying opportunity and said POET-related concerns would not materially hurt SIVE’s fundamentals.

🔴 @SingularityRes

Acknowledges the bottleneck narrative but questions how SIVE can justify its current valuation with only around $50M guided revenue by 2027.

His concern is that the market cap has moved too far ahead of visible fundamentals.

🔴 @jasonschips

The most openly bearish voice and is actively pushing back against the SIVE bull thesis.

He argues the rally is speculative, unsustainable, and not supported by actual fundamentals or confirmed volume purchase orders.

DYOR, NFA.

English

@asianinvestors I think it’s the right time you average it down. Market might not give you another chance

English

I know many investors of $SIVE are getting worried about risk profile after such a large rally.

And also due to the amount of bear posting on X recently, saying it's way overvalued, and correction will come in after earnings.

I urge you to conduct your own research into the stock. Understand the business, the industry and the numbers. Once you grow convicted with your thesis, no one can spread FUD.

Don't panic sell over some fake rumour

English

@Million_Sancet Can you tell me where does it say Nvidia ? Or largest AI company ?

English

It seems like yesterday's 61% wasn't enough for $SHT, it wants another 23%

I think the market is finally realizing that such a small Swedish company, which only MisterCap and I had been covering for months, is landing $NVDA as a client

It was pretty obvious in hindsight when they got confirmation of receiving orders from major players

Even so, it stayed flat and even had slight drops

This explains the importance of knowing the thesis and having conviction

The catalyst happened weeks ago

The price just started moving yesterday

Remember that with the market, you either scream in its face that you are making money, or nobody sees the things I’ve been talking about for weeks regarding $SHT

The price seems a bit frozen, similar to $SMOL yesterday when it was around 15% and ended the day at 45%, so I expect more upside

English

@BrueghelElder87 @TheBigBerbowski Yes it does especially the breakup of the revenue.

Also the guidance for 2027 and any partnership.

Ask yourself they had the last order with Ayar in 2024 if I’m not wrong and it’s 2026

Company projects 50mil revenue in 2027. And you think people on twitter know more than company

English

@singhsurya1012 @TheBigBerbowski Do the next earnings numbers matter to you? If so, why?

English

My $SIVE investors will get more and more questions. I hope you'll not see them all as bearish.

As the stock grows there will be more and more focus on it, which on one side might be good (more buys) but also might be bad (analysts' opinions, flaws, sell offs).

In any case, questions are good.

Singularity Research@SingularityRes

Can anyone tell me how $SIVE grows into the current valuation? I understand it’s a bottleneck But they guided for $50m in revenue by 2027 Will they jack up the prices just like memory companies or something that I’m missing Because if there is no path of it growing into the valuation of $1.5B - it could crash badly. Just don’t know when.

English

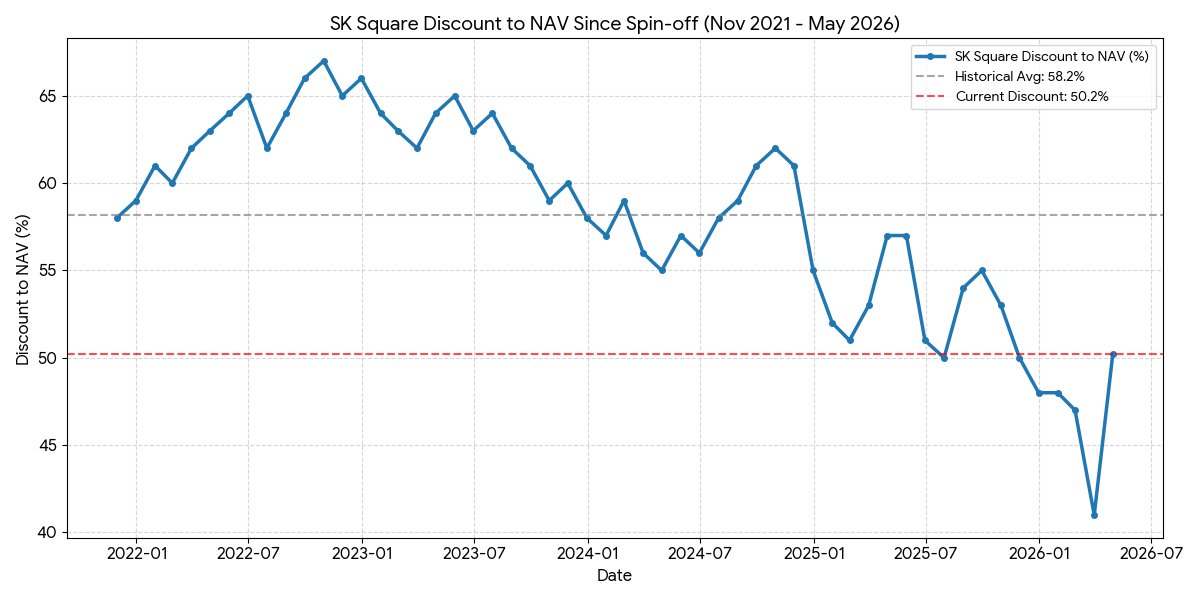

@babyfolio I took a position today. Just wondering have you seen days where sk square closed more positive compared to sk Hynix. It could be that both close negative but sk square being down less ?

English

SK Hynix ($000660) rips +7% while its holding company, SK Square ($402340), drops 1%.

This is exactly why you don't trade the daily noise on a structural arbitrage play.

The thesis takes time to unfold, and the chart will always have its swings.

The only metric that matters long-term is the NAV discount closing.

Let it play out.

Babyfolio@babyfolio

English

$SHT completes it’s first order to worlds largest AI-hardware company

Amazing start of the week. They are now aproved to take larger orders which I think will happen very soon

Everything is playing out at planned

English

The ultimate $SHT Smart High Tech report

I have been writing about this company the last 2 months. I have been buying since 2023 but didn’t size up until April 2026 and I now hold a heavy position AVG 18 SEK and own around 0.2% of the company

Here is my full analysis from where we are today after just ripping 65% and closing at 40 SEK👇

$SHT is a pure play on solving one of AI’s hardest bottlenecks (cooling and thermal management) with a superior patented nanotechnology solution. Todays delivery to the world leading AI-customer (99% sure $NVDA) and Henkel partnership mark the transition from R&D/prototyping to commercial scaling

In a time where AI demand more powerful chips running hotter than ever, companies that enable more compute per watt and reliable high-density operation will be highly rewarded. $SHT still has such a small MCAP of just €130MUSD which gives this play a crazy upside and growth opportunity. They have the technology, validation, and partnerships to become a critical supplier in the MULTI-billion dollar thermal management market.

The AI boom is driving CRAZY demand for advanced cooling and the tail-wind for $SHT from the whole sector is explosive

—> Global semiconductor industry projected to hit ~$975B in 2026, with AI chips alone approaching half of revenues

—> Hyperscalers and AI leaders are pouring hundreds of billions into data centers, where thermal management is a bottleneck.

—> $SHT recently completed its first delivery to the world’s largest AI hardware player, qualifying it for further orders in AI, data centers, and semiconductors

This validation from $NVDA is a major de-risking event and opens doors to substantial follow-on business.

Why would Henkel and $NVDA navigate $SHT and adjust their production line to fit their demands, for them to not take advantage of it? That doesn’t make sense. Everything is aproved and I am very confident large orders will flow in during the summer

It’s crazy for me that @Serenity and her american soldiers haven’t found this gem. Sweden 🇸🇪 is a world leading tech and AI country and there is so many promising companies coming up such as $SIVE, $SMOL and not least the telecom giant $ERIC

$SHT is the one with the highest upside in my opinion

The risk will always be there with a small cap company but for an AI-investor with a little bit risk tolerance the risk:reward points heavily bullish here!!! This is in my opinion an amazing play in the AI gold rush and a completely hidden gem

//Slark

English