Sabitlenmiş Tweet

ski.hl

409 posts

ski.hl

@skiBTFD

@HyperliquidX @LiquidLaunchHL @SaveTheWhal3s

Unentrenched Katılım Kasım 2020

583 Takip Edilen212 Takipçiler

ski.hl retweetledi

February 16, Hyperliquid hires @Sterling_hl as BD. Previously onchain lead at @circle.

3 months later, Coinbase becomes USDC treasury deployer, Circle becomes technical deployer, both staking HYPE.

Connect the dots.

Hyperliquid.

English

ski.hl retweetledi

Everyone is arguing about $USDH dying. They're missing the point entirely. What happened today is the single most important business move in Hyperliquid's history.

Let me explain. Revenue, liquidity, politics, lobby, and what it means for the USDH vote debate.

Coinbase is now the official treasury deployer of $USDC on Hyperliquid under AQAv2. Circle handles the technical side (CCTP, cross-chain infra). Both are staking hyperliquid:native. Native Markets agreed to sell the USDH brand assets to Coinbase.

$USDH is sunsetting. But the mechanics it pioneered are not. They just got applied to a $4.7B asset instead of a $100M one.

Let's break down why this is a win on every single front.

LIQUIDITY

The biggest complaint from traders and builders for months: fragmentation. $USDH had the alignment but not the liquidity. $USDC had the liquidity but not the alignment. You had to choose.

That choice is gone. One stablecoin. One orderbook per pair. No split liquidity. No confusion for HIP-3 deployers picking a quote asset. No friction for new users bridging in.

$4.7B in USDC on Hyperliquid, 2x year over year. That is the base generating yield now, not $100M.

REVENUE

Under AQAv2, the treasury deployer shares 90% of the reserve yield revenue with the protocol. Run the numbers on the current $USDC supply:

$4.7B at 3.8% interest rate, 90% shared with the Assistance Fund = $160M+ per year flowing directly into HYPE buybacks. That is $440K per day. Every day.

For context, USDH at peak supply was generating a fraction of this on $100M. The AQA model worked. It just needed to be applied at the right scale.

POLITICS AND LOBBYING

This is the angle most people are sleeping on. Coinbase is the largest publicly traded crypto company in the US. They spent over $100M on crypto lobbying and political action in the last cycle. They are the single most powerful voice for crypto regulation in Washington.

The CLARITY Act markup is happening today. Coinbase has been one of its strongest advocates. Having them financially aligned with Hyperliquid, staking HYPE, operating as treasury deployer, is not just a liquidity play. It is a regulatory shield.

Every conversation about "is Hyperliquid a US regulatory risk" just got a lot harder to make when Coinbase is literally staked into the network.

Circle staking 500K HYPE and moving toward becoming a validator. Jeremy Allaire posting "Hyperliquid." That is institutional endorsement at the highest level.

THE USDH QUESTION

"Was USDH a failure?" "Was the vote theater?" "Did Native Markets just flip an asset?"

No. USDH was a weapon. It was a credible threat that proved a protocol can demand yield sharing from stablecoin issuers. Before USDH, Hyperliquid had $5B+ in USDC generating $150-200M/year for Circle and Coinbase. The protocol saw none of it.

USDH launched. The AQA model proved that yield can be redirected onchain, transparently, back to the protocol. It only reached $100M in supply but that was never the point. The point was forcing incumbents to the table.

Basit said it best: the entire lifecycle of USDH from launch to sunset should be studied. Coinbase didn't come to Hyperliquid out of goodwill. They came because USDH proved they would lose the venue if they didn't align.

"But Paxos offered better economics during the vote." Maybe on paper. But 95-100% of a stablecoin that might have also struggled to reach $100M in supply is still less revenue than 90% of $4.7B. The vote was never about picking the best yield split on a small asset. It was about creating the leverage to capture yield on the dominant one.

WHAT THIS MEANS FOR BUILDERS

USDC becomes the canonical quote asset for HIP-4 outcome markets. No more guessing which stablecoin to build around. Hyper Foundation is issuing grants to HIP-3 and HIP-1 deployers who integrated USDH to cover migration costs. Feeless conversions from USDH to USDC during the transition.

For HIP-3 deployers running equity perps, commodity perps, outcome markets: one liquidity pool, one collateral asset, deeper books.

SECOND ORDER EFFECTS

Coinbase operating perps through Hyperliquid via builder codes? Not confirmed, but now structurally possible. Their existing perp product is weak. Hyperliquid's infrastructure is the best in crypto. The incentive alignment is there.

Tether now has a clear path to compete. AQAv2 is an open spec. Any stablecoin issuer can stake 500K HYPE and share yield to become an aligned quote asset. Competition is good.

AQAv2 becomes a blueprint for every other chain. Hyperliquid just proved that a protocol can force the largest stablecoin issuers in crypto to share revenue at the protocol level. No one has done this before.

Hyperliquid.

English

ski.hl retweetledi

ski.hl retweetledi

Real economics in a rapidly growing marketplace, not simply a store of value. That’s why $HYPE continues to outperform BTC

Hyperliquid.

English

ski.hl retweetledi

ski.hl retweetledi

Assets added to the roadmap today: Hyperliquid (HYPE)

coinbase.com/blog/increasin…

English

ski.hl retweetledi

A useful mental exercise is to treat your current holdings as the only reference point that matters and ask yourself a simple question: if everything I hold were liquidated to USD today, would I reallocate the capital in exactly the same way?

This reframe strips away the psychological weight of where you entered, what you paid, or how far you are from some previous peak. It forces you to evaluate each position on its present merits rather than on the sunk costs or emotional attachments you've accumulated along the way. Look up reference dependence.

Your portfolio's all-time high is just one data point on a longer equity curve, an arbitrary high-water mark that offers no actionable insight. Benchmarking your decisions against that fleeting peak only anchors you to a past outcome you cannot change, and worse, it distorts your judgment going forward.

What matters is optimizing your decision framework for the hand you hold right now. So, are you positioned because you're biased, or are you biased because you're positioned?

English

ski.hl retweetledi

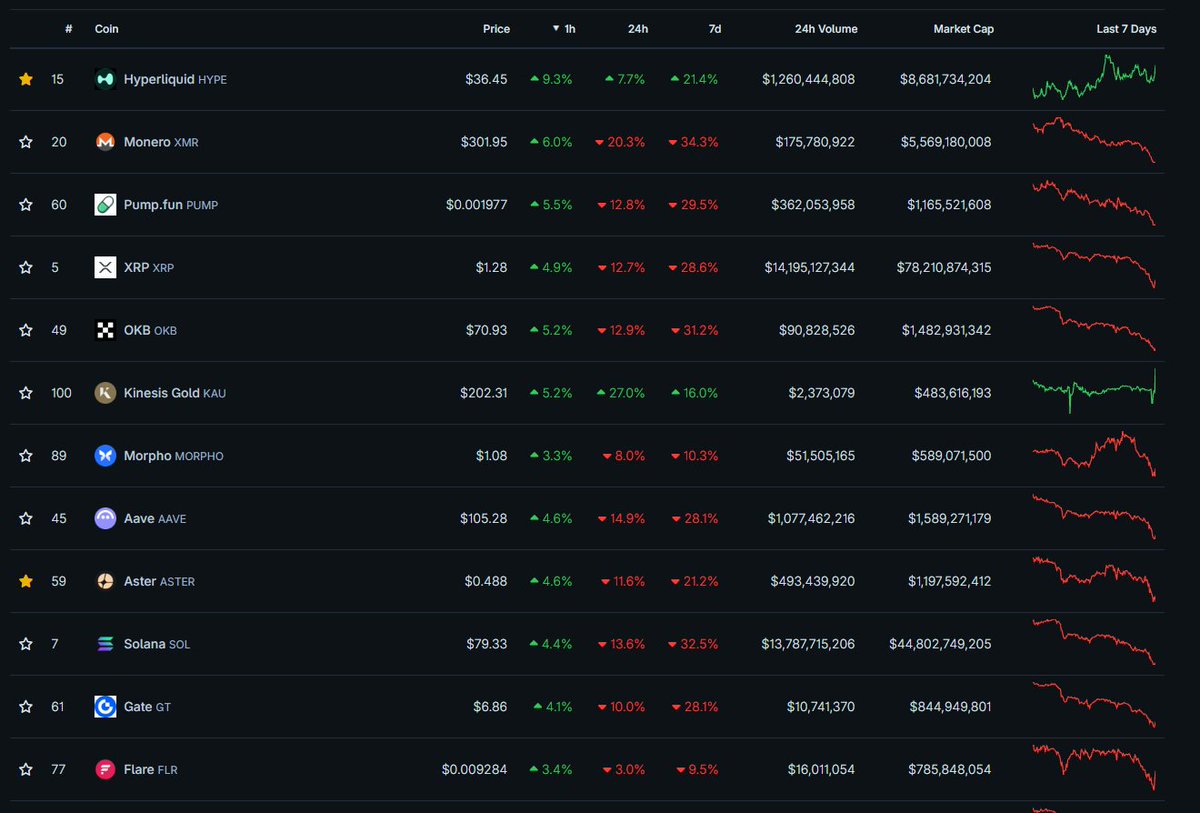

HIP-3 open interest reached an all-time high of $790M, driven recently by a surge in commodities trading.

HIP-3 OI has been hitting new ATHs each week. A month ago, HIP-3 OI was $260M.

English

@vnovakovski @aaalexhl Platforms with "low cost" and "no fees" sounds very attractive to the inexperienced trader, but the caveat is that you’re actually indirectly paying way more fees because of shallower liquidity and worse spread.

English

@aaalexhl By that logic, Hyperliquid is implementing everything that Binance already had 6 years ago. The basics of perps trading have been table stakes for a long time.

Where we are innovating is 1) low cost, 2) low latency, 3) secure, 4) verifiable, 5) composable.

English

Seems we have moved from "first they ignore you" to "then they fight you" in the FUD cycle.

Not sure if these guys know ZK proofs work or read the whitepaper, but let's see what new attack they come back with once the circuits are public this week.

x.com/HyperliquidX/s…

Hyperliquid@HyperliquidX

Hyperliquid is built on a foundation of onchain transparency. A recent article made several claims that are factually incorrect: + Solvency: Every dollar is accounted for; the author failed to count native HyperEVM USDC. + Integrity: Testnet functions are exactly that - testnet only for testing. They cannot be executed on mainnet. + Transparency: Hyperliquid is more transparent and decentralized than all other major venues for perps trading. The entire state is independently maintained by a permissionless validator set and verified through BFT proof-of-stake consensus by each node. Every order, trade, and liquidation is available in real time during execution. Anyone can run a node and index the chain’s state and transitions. No major perps platform comes close to this guarantee for users. See our response to the writer’s individual points below. Claim: The system is undercollateralized by $362M False: The Hyperliquid blockchain state is fully and verifiably solvent. The author excluded the HyperEVM USDC (a publicly announced and much anticipated integration), which exists in parallel to the Arbitrum bridge. Every USDC in circulation on HyperCore is accounted for transparently, by summing up the balances of arbiscan.io/address/0x2df1… and hyperevmscan.io/address/0x6b9e…. At the time of writing, this amounts to 3.989B + 362M = 4.351B USDC on HyperCore. USDC on the HyperEVM can be computed by subtracting 362M from the 421M on the HyperEVM USDC contract (hyperevmscan.io/token/0xb88339…), totaling another 59M USDC on HyperEVM. The sum of the Arbitrum bridge and native USDC balances can be compared against the sum of user balances on HyperCore. As highlighted in the introduction, this exercise of verifying complete system solvency against user balances is uniquely possible on Hyperliquid compared to competitors. The current Arbitrum bridge was an important stepping stone in bootstrapping the Hyperliquid network and will be deprecated as the migration to native USDC is complete, bringing Hyperliquid to parity with other major L1s. Claim: There is retroactive volume manipulation via TestnetSetYesterdayUserVlm False: This is a testnet-only function to allow for comprehensive testing. The author states that “the function’s presence is the problem…capability alone violates the trust model.” Testnet-only features that enable more rigorous testing of edge cases do not undermine the chain’s integrity. The fee schedule on Hyperliquid interacts in a complex way with inputs: user volume, aligned quote token status, maker vs taker, HIP-3, etc. It’s important to test these interactions on testnet, and therefore the testnet chain has a set of admin testing functions that do not exist on mainnet. The related TestnetAddMainnetUser action is to mark a testnet user as having corresponding mainnet state, to avoid DDOS and other attacks that are “free” on testnet. None of these functions are callable on the mainnet state. While the execution source is not available, anyone can verify every trade onchain by running a node, and sum up the values to confirm that volume numbers are reflected accurately in onchain state. Similar to onchain solvency verification against the sum of all user account values, this is possible on Hyperliquid but not on most competitive platforms. Given that this code path is entirely unreachable on mainnet, future development work will entirely compile out this testnet-only logic on mainnet nodes to avoid any possible misunderstanding or misinterpretation. Claim: Some users have special privileges such as fee exemptions or retroactive volume manipulation used to influence the airdrop False: Like system solvency, user balances, and individual trades, the fees paid by any address is available onchain. Each trade along with its fees paid or rebates received are transparently indexed by nodes, API servers, and third party analytics providers. There are no such mechanisms to distort fees, and no such mechanisms could have influenced the HYPE airdrop. Furthermore, the genesis distribution of HYPE is fully available onchain, and users can verify the historical behavior of every such address. Claim: “CoreWriter” godmode can mint tokens, move user funds without signatures, crash random validators and basically do whatever it wants False: The CoreWriter spec is fully documented here hyperliquid.gitbook.io/hyperliquid-do… and replicable in the open source HyperEVM execution. CoreWriter is a way for smart contracts on HyperEVM to send HyperCore actions as part of HyperEVM block execution. It supports various actions that are normally sent by EOAs such as staking and placing orders, but has no such features to “mint tokens, move user funds without signatures, crash random validators and basically do whatever it wants.” This is a fundamental misunderstanding of how HyperCore interacts with the HyperEVM. Claim: Chain can freeze via governance, and no undo function exists Misinterpreted: The chain freezes during network upgrades. There is no undo function because the validators adopt a new binary at that height. This is analogous to how other networks perform hard forks at future heights determined by social consensus. Suspicious activity on POPCAT in Nov 2025 did not cause the L1 to freeze, nor were any user funds frozen. The L1 was entirely operational, and any observer can see the blocks that were produced during this time. The Arbitrum bridge was automatically locked after the incident due to abnormal variation in account balances. As explained above, the Arbitrum bridge is not as secure as natively minted USDC, and therefore requires several conservative automated locking mechanisms as safeguards. The Arbitrum bridge’s locking mechanism is audited and open sourced, and the bridge is being deprecated with the transition to native USDC. Claim: A single private key can set any oracle price instantly: no timelock, no limits Misinterpreted: The author is likely mistaking the HIP-3 oracle updater logic with the validator-operated perps. HIP-3 oracle updates are indeed set by a single address, but this is up to the deployer to configure. The updater address need not be an EOA. For example, current HIP-3 deployers use a combination of MPC and CoreWriter architecture. For validator-operated perps, multiple validators can submit oracle price updates. The final prices are a robust weighted median across major centralized exchanges. There is no timelock and no limits explicitly because these limits make the system less, not more, safe. The events of 10/10 show the danger to solvency if ADL is not accurately triggered in a timely manner during high volatility. Hyperliquid was one of the only venues without performance degradation or a network outage during this time. If Mango Markets or a similar protocol with oracle rate limits were active during 10/10, they would have likely accrued bad debt. Further decentralization will involve other validators actively running independent and open-sourced oracle update binaries. Claim: 8 undisclosed addresses control all transaction submission False: Some transactions are already sent directly from the validators. Some such as orders are not, in order to minimize MEV, but a future upgrade will incorporate this logic for all transactions in a mechanism that is both MEV- and censorship-resistant. The careful consideration of MEV is in response to trader and researcher feedback based on predatory behavior observed on other chains. There is almost unanimous agreement that toxic transaction ordering degrades the end user experience. Ultimately, the validator set is permissionless, and there is no guarantee that validators in the mainnet set are always fully aligned with the ecosystem. A major milestone in decentralization will be solving this problem, including a multiple-proposer block building setup. Claim: There is a liquidation cartel with unfair advantages Misinterpreted: Only HLP may backstop liquidate users, and HLP subvaults are the only addresses in this set. However, depositing into HLP is permissionless, so HLP is a community-owned liquidity vault supporting the protocol. The fact that HLP has privileges is no different from other protocol liquidity vaults. Relatedly, all liquidations are first attempted against the order book, which handles the vast majority of liquidated positions without backstop liquidation. This allows users to keep any remaining collateral, and allows all other users to compete in providing the best price to the liquidation flow, benefitting the liquidated user. Claim: There is a hidden lending protocol with $1M+ supplied and no documentation False: Portfolio margin, borrow lend, and the HLP supplied value were all publicly announced and are currently in pre-alpha rollout. The current documentation can be found at hyperliquid.gitbook.io/hyperliquid-do… and has been progressively fleshed out over the past several weeks. Claim: ModifyNonCirculatingSupply allows changes to token supply False: The full supply of HIP-1 tokens on HyperCore is fixed at deployment. The non-circulating supply is a purely informational number that can optionally mark addresses as “non-circulating” for display purposes. Whether an address is marked as “non-circulating” does not affect execution. This is an example of onchain information that might make more sense offchain, but is not a vulnerability. Thank you to the author for spending the time to verify the execution of Hyperliquid. The fact that this investigation could be done at all proves the transparency and decentralization that Hyperliquid has already achieved. Concretely, Hyperliquid is the only major perps venue where the entire state and every input diff is transparently available to anyone running a node. A similar analysis on any of the other top perp DEXs is impossible. For example, Lighter uses a single centralized sequencer whose execution logic and ZK circuits are unavailable. Aster uses centralized matching and even offers dark pool trading, which is only possible with a single centralized sequencer without verifiable execution. Other protocols with some open source contracts do not have a verifiable sequencer. On Binance, Lighter, Aster, or similar exchanges, it is impossible for anyone other than the sequencer to see a full snapshot of onchain state including order books, positions, and other user information. The centralized sequencer can also upgrade its software without any constraints. On Hyperliquid, the entire state is onchain, which means there are 24 validators executing the same state machine under BFT consensus rules. There is plenty left to do on the journey towards greater decentralization, but it’s important to highlight just how far Hyperliquid and its ecosystem have come compared to competitors. Decentralization is progressive, and Hyperliquid will ultimately be fully open sourced. Hyperliquid is the most transparent of all major venues, even though this leaks advantages to competitors (all of whom are closed source), who can copy Hyperliquid’s innovations more easily. We think this is the correct tradeoff to balance value accrual to the community, speed of innovation, and upholding the values of defi. The HyperEVM execution is open source, and Sprites, an independent community member, maintains a full archival node that powers many important integrations. HyperCore will follow the same path as soon as it reaches feature completion.

English

Hyperliquid is built on a foundation of onchain transparency. A recent article made several claims that are factually incorrect:

+ Solvency: Every dollar is accounted for; the author failed to count native HyperEVM USDC.

+ Integrity: Testnet functions are exactly that - testnet only for testing. They cannot be executed on mainnet.

+ Transparency: Hyperliquid is more transparent and decentralized than all other major venues for perps trading. The entire state is independently maintained by a permissionless validator set and verified through BFT proof-of-stake consensus by each node. Every order, trade, and liquidation is available in real time during execution. Anyone can run a node and index the chain’s state and transitions. No major perps platform comes close to this guarantee for users.

See our response to the writer’s individual points below.

Claim: The system is undercollateralized by $362M

False: The Hyperliquid blockchain state is fully and verifiably solvent. The author excluded the HyperEVM USDC (a publicly announced and much anticipated integration), which exists in parallel to the Arbitrum bridge. Every USDC in circulation on HyperCore is accounted for transparently, by summing up the balances of arbiscan.io/address/0x2df1… and hyperevmscan.io/address/0x6b9e…. At the time of writing, this amounts to 3.989B + 362M = 4.351B USDC on HyperCore. USDC on the HyperEVM can be computed by subtracting 362M from the 421M on the HyperEVM USDC contract (hyperevmscan.io/token/0xb88339…), totaling another 59M USDC on HyperEVM.

The sum of the Arbitrum bridge and native USDC balances can be compared against the sum of user balances on HyperCore. As highlighted in the introduction, this exercise of verifying complete system solvency against user balances is uniquely possible on Hyperliquid compared to competitors.

The current Arbitrum bridge was an important stepping stone in bootstrapping the Hyperliquid network and will be deprecated as the migration to native USDC is complete, bringing Hyperliquid to parity with other major L1s.

Claim: There is retroactive volume manipulation via TestnetSetYesterdayUserVlm

False: This is a testnet-only function to allow for comprehensive testing. The author states that “the function’s presence is the problem…capability alone violates the trust model.” Testnet-only features that enable more rigorous testing of edge cases do not undermine the chain’s integrity. The fee schedule on Hyperliquid interacts in a complex way with inputs: user volume, aligned quote token status, maker vs taker, HIP-3, etc. It’s important to test these interactions on testnet, and therefore the testnet chain has a set of admin testing functions that do not exist on mainnet. The related TestnetAddMainnetUser action is to mark a testnet user as having corresponding mainnet state, to avoid DDOS and other attacks that are “free” on testnet. None of these functions are callable on the mainnet state.

While the execution source is not available, anyone can verify every trade onchain by running a node, and sum up the values to confirm that volume numbers are reflected accurately in onchain state. Similar to onchain solvency verification against the sum of all user account values, this is possible on Hyperliquid but not on most competitive platforms.

Given that this code path is entirely unreachable on mainnet, future development work will entirely compile out this testnet-only logic on mainnet nodes to avoid any possible misunderstanding or misinterpretation.

Claim: Some users have special privileges such as fee exemptions or retroactive volume manipulation used to influence the airdrop

False: Like system solvency, user balances, and individual trades, the fees paid by any address is available onchain. Each trade along with its fees paid or rebates received are transparently indexed by nodes, API servers, and third party analytics providers. There are no such mechanisms to distort fees, and no such mechanisms could have influenced the HYPE airdrop. Furthermore, the genesis distribution of HYPE is fully available onchain, and users can verify the historical behavior of every such address.

Claim: “CoreWriter” godmode can mint tokens, move user funds without signatures, crash random validators and basically do whatever it wants

False: The CoreWriter spec is fully documented here hyperliquid.gitbook.io/hyperliquid-do… and replicable in the open source HyperEVM execution. CoreWriter is a way for smart contracts on HyperEVM to send HyperCore actions as part of HyperEVM block execution. It supports various actions that are normally sent by EOAs such as staking and placing orders, but has no such features to “mint tokens, move user funds without signatures, crash random validators and basically do whatever it wants.” This is a fundamental misunderstanding of how HyperCore interacts with the HyperEVM.

Claim: Chain can freeze via governance, and no undo function exists

Misinterpreted: The chain freezes during network upgrades. There is no undo function because the validators adopt a new binary at that height. This is analogous to how other networks perform hard forks at future heights determined by social consensus.

Suspicious activity on POPCAT in Nov 2025 did not cause the L1 to freeze, nor were any user funds frozen. The L1 was entirely operational, and any observer can see the blocks that were produced during this time. The Arbitrum bridge was automatically locked after the incident due to abnormal variation in account balances. As explained above, the Arbitrum bridge is not as secure as natively minted USDC, and therefore requires several conservative automated locking mechanisms as safeguards. The Arbitrum bridge’s locking mechanism is audited and open sourced, and the bridge is being deprecated with the transition to native USDC.

Claim: A single private key can set any oracle price instantly: no timelock, no limits

Misinterpreted: The author is likely mistaking the HIP-3 oracle updater logic with the validator-operated perps. HIP-3 oracle updates are indeed set by a single address, but this is up to the deployer to configure. The updater address need not be an EOA. For example, current HIP-3 deployers use a combination of MPC and CoreWriter architecture.

For validator-operated perps, multiple validators can submit oracle price updates. The final prices are a robust weighted median across major centralized exchanges. There is no timelock and no limits explicitly because these limits make the system less, not more, safe. The events of 10/10 show the danger to solvency if ADL is not accurately triggered in a timely manner during high volatility. Hyperliquid was one of the only venues without performance degradation or a network outage during this time. If Mango Markets or a similar protocol with oracle rate limits were active during 10/10, they would have likely accrued bad debt. Further decentralization will involve other validators actively running independent and open-sourced oracle update binaries.

Claim: 8 undisclosed addresses control all transaction submission

False: Some transactions are already sent directly from the validators. Some such as orders are not, in order to minimize MEV, but a future upgrade will incorporate this logic for all transactions in a mechanism that is both MEV- and censorship-resistant. The careful consideration of MEV is in response to trader and researcher feedback based on predatory behavior observed on other chains. There is almost unanimous agreement that toxic transaction ordering degrades the end user experience. Ultimately, the validator set is permissionless, and there is no guarantee that validators in the mainnet set are always fully aligned with the ecosystem. A major milestone in decentralization will be solving this problem, including a multiple-proposer block building setup.

Claim: There is a liquidation cartel with unfair advantages

Misinterpreted: Only HLP may backstop liquidate users, and HLP subvaults are the only addresses in this set. However, depositing into HLP is permissionless, so HLP is a community-owned liquidity vault supporting the protocol. The fact that HLP has privileges is no different from other protocol liquidity vaults.

Relatedly, all liquidations are first attempted against the order book, which handles the vast majority of liquidated positions without backstop liquidation. This allows users to keep any remaining collateral, and allows all other users to compete in providing the best price to the liquidation flow, benefitting the liquidated user.

Claim: There is a hidden lending protocol with $1M+ supplied and no documentation

False: Portfolio margin, borrow lend, and the HLP supplied value were all publicly announced and are currently in pre-alpha rollout. The current documentation can be found at hyperliquid.gitbook.io/hyperliquid-do… and has been progressively fleshed out over the past several weeks.

Claim: ModifyNonCirculatingSupply allows changes to token supply

False: The full supply of HIP-1 tokens on HyperCore is fixed at deployment. The non-circulating supply is a purely informational number that can optionally mark addresses as “non-circulating” for display purposes. Whether an address is marked as “non-circulating” does not affect execution. This is an example of onchain information that might make more sense offchain, but is not a vulnerability.

Thank you to the author for spending the time to verify the execution of Hyperliquid. The fact that this investigation could be done at all proves the transparency and decentralization that Hyperliquid has already achieved. Concretely, Hyperliquid is the only major perps venue where the entire state and every input diff is transparently available to anyone running a node.

A similar analysis on any of the other top perp DEXs is impossible. For example, Lighter uses a single centralized sequencer whose execution logic and ZK circuits are unavailable. Aster uses centralized matching and even offers dark pool trading, which is only possible with a single centralized sequencer without verifiable execution. Other protocols with some open source contracts do not have a verifiable sequencer.

On Binance, Lighter, Aster, or similar exchanges, it is impossible for anyone other than the sequencer to see a full snapshot of onchain state including order books, positions, and other user information. The centralized sequencer can also upgrade its software without any constraints. On Hyperliquid, the entire state is onchain, which means there are 24 validators executing the same state machine under BFT consensus rules. There is plenty left to do on the journey towards greater decentralization, but it’s important to highlight just how far Hyperliquid and its ecosystem have come compared to competitors.

Decentralization is progressive, and Hyperliquid will ultimately be fully open sourced. Hyperliquid is the most transparent of all major venues, even though this leaks advantages to competitors (all of whom are closed source), who can copy Hyperliquid’s innovations more easily. We think this is the correct tradeoff to balance value accrual to the community, speed of innovation, and upholding the values of defi.

The HyperEVM execution is open source, and Sprites, an independent community member, maintains a full archival node that powers many important integrations. HyperCore will follow the same path as soon as it reaches feature completion.

English

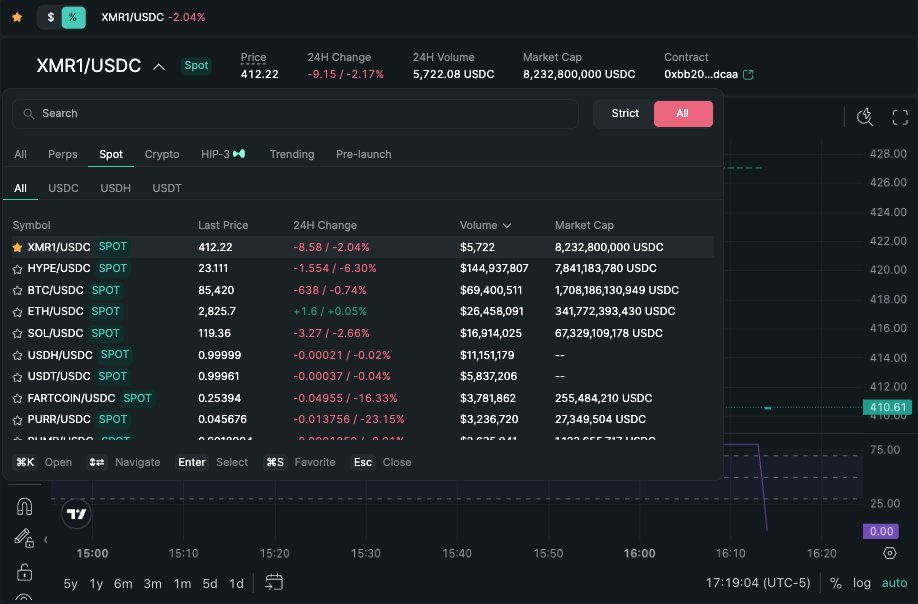

@gialloxmr it is kinda how the foundation chose to label the Hyperunit spot assets with the canonical ticker instead of the initially acquired on-chain ticker with the «u» in front of them (uBTC, uSOL etc.)

English

perps show the canonical XMR ticker because theyre cash-settled derivatives that reference an oracle price of XMR. Spot shows XMR1 because it is not native Monero, but a custodial IOU.

what is important to keep in mind though is that the Hyperliquid frontend itself is centralized and run by the foundation, and how assets are labeled there is opinionated

English

ski.hl retweetledi