SM

338 posts

$MU Good to see what some of the analysts are modeling. Wells base case has a longer term EPS of $40 but sees up to $85 next year. I think in time that $40 creeps up to $50+ maybe even $60 and this ends up teasing 1000 but that requires a lot of things to happen (war ending, bull market, rate cuts, capex continued growth, no recession). Always a risk, but MU is a good risk:reward on pullbacks for sure. Not going to be a top 3 position for me anymore(was #1 last year) but still bullish.

English

**Commentary**

💥 🦅 President Trump brilliantly exposed NATO's so-called allies as total freeloaders during the Iran operation. They refused to help and fell right into his trap. Now it's clear we don't need them dragging us down. Time to seriously rethink NATO and put America First like never before. The dominoes are falling on these one-sided deals!

Agree? Drop your take.

#PatriotsRise

English

🚨AMERICA'S SO CALLED "ALLIES" JUST FELL RIGHT INTO PRESIDENT TRUMP'S TRAP, EXPOSED AS TOTAL FREELOADERS

Time to leave and defund NATO.

English

@i9theghost5 their receivables are growing much faster than revenue - charge offs coming - should have sold at 85

English

Here’s what appears to be happening:

1. Tucker Carlson has allegedly been conducting his own foreign policy with Iran on behalf of the United States.

2. At some point, the CIA got wind of this and informed President Trump, who may then have used Tucker as an unwitting counterintelligence asset to feed faulty information to Iran. (BASED.)

3. Following the launch of Epic Fury, Tucker’s traitorous behavior may have finally caught up with him, as DOJ reportedly prepares a criminal complaint against him based on CIA intelligence.

🇮🇷 Bonus Round: An Example of Tucker Likely Parroting Iranian Regime Propaganda 🇮🇷

4. After the operation began, Iran sent IRGC agents to carry out attacks in Saudi Arabia and Qatar, but those plots were foiled.

5. Iran then told Tucker these were actually Mossad plots — a claim he pushed online and that spread like wildfire.

6. Saudi and Qatar had to publicly deny Tucker's fake news about the Mossad.

English

@cantonmeow it is amazing a clueless idiot always blames every else for his lack of maturity & intelligence - an ignorant stubborn child

English

If you believe the Fed runs the market

Unfollow me now

English

Hegseth: "Some in the press just can't stop. Allow me to make a few suggestions. People look at the TV and they see banners, headlines -- I used to be in that business, I know everything is written intentionally. For example, a banner -- 'Mideast War Intensifies.' What should the banner read instead? How about, 'Iran increasingly desperate,' because they are. Or more fake news from CNN. The sooner David Ellison takes over that network, the better."

English

@martypartymusic Right so with tariffs increasing the cost to US citizen and a lower dollar increasing costs/prices further - what gives - 94% of tariff costs thru higher prices and lower dollar value hit the us folks hard - inflation is falling due to rate of increase falling - Economic 101

English

Russia has sold 71% of their NWF Gold to fund Ukraine war

Percentage and Volume Reduction: Russia’s National Wealth Fund (NWF) gold holdings dropped by approximately 71% from May 2022 (shortly after the full-scale invasion began) to early 2025/January 2026.

English

@martypartymusic Jeez man - stop giving stupid tax cuts - that is the problem and people that benefit the most pay their fair share - tariffs are being funded by the poor/middle class in this country - wake up

English

SCOTUS tariff ruling adds $2.4 trillion to the US debt 💸

Who would want the national debt to increase to crisis level?

Hmm.

English

@weary_centurion What is the reason for $800M in debt if they do not hold loans - it is not a capital light company

English

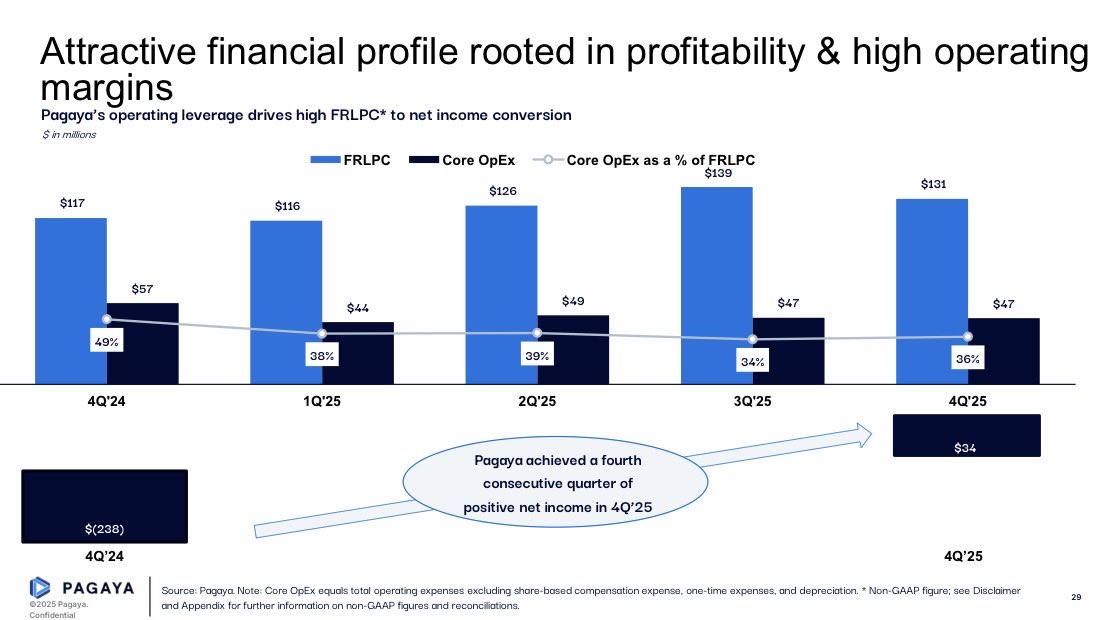

12. VALUATION

Here is where it gets very interesting.

After the Q4 sell off, $PGY now sits in the $12-13 range.

Around $1B market cap.

• TTM PE - 12x

• Forward PE - 5x

• Forward EV/EBITDA - 3x

• P/S - 0.6

This is for a company that grew revenue 26% in 2025 and flipped from a $401M loss to $81M profit with 29% EBITDA margin.

They are comfortably above the rule of 40 and have been for several quarters.

This is laughable quite frankly.

$UPST has the following:

• TTM PE - 60x

• Forward PE - 20.5x

• Forward EV/EBITDA - 14.2x

• P/S - 2.4x

• EBITDA margin - 22%

Upstart is growing revenue 35%+ but it is less profitable and higher risk.

Upstart is currently doing $1B revenue and 54M net income with only $230M in EBITDA compared to $PGYs $371M.

Yet, they trade at a market cap of $3B and are valued around 3-5x more expensive across multiple metrics

Their balance sheet is also more leveraged than $PGY with $1.9B in debt and almost $1B of loans directly on their balance sheet. Debt to equity is 234%.

$PGY has a 110% debt to equity but with less than half the debt and very minimal loans on the balance sheet as most of their loans are securitised.

So if $UPST is any sort of benchmark for where $PGY should be trading at, it’s a lot more than where it is now.

$UPST trades at a hefty premium. I honestly struggle to understand why.

For me the $PGY business model is far higher quality and more durable.

Even a modest re-rating to a fair PE of 25x is likely a 2x from where it is now.

$PGY is valued as a dying, financially distressed asset. The opposite is true.

Either I am wrong, or this is one of the cheapest stocks on the market.

Look at the chart below and explain to me why this is valued as such?

English

$PGY DEEP DIVE 🧵

The technology company revolutionising the U.S. financial credit sector

“Delivering more financial opportunity to more people, more often”

English

@weary_centurion So what is the $800M in long term debt - do not understand that - unless it is on their books for a very short period - then it should come under short-term liabilities. They have $1.18B in cash + other short term assets makes it almost $12+ in cash receivables - am I wrong?

English

11. COMPETITORS

Here’s the funny thing. Pagaya doesn’t really have any true competitors.

No other fintech is embedded within the U.S. financial ecosystem like they are. Nobody else has an equivalent AI model with access to such an astonishing amount of vaulted financial data.

Their closest thing to a competitor is probably $UPST.

UPSTART

Upstart is a direct competitor in AI credit, but their model is different.

Upstart is direct to consumer. People go to their website directly to obtain loans.

Upstart relies heavily on marketing and small banks/credit unions to buy their loans. They also hold loans on their own balance sheet.

Upstart grows faster but with far higher risks. They are incredibly vulnerable to macro economic turbulence and could quickly be in a position where they would struggle to sell loans to the small banks/credit unions they work with.

In a recession they would take a massive hit and be forced to hold most or all of their loans on their own balance sheet, increasing risks of financial distress.

PAGAYA

In comparison, Pagaya has ZERO marketing costs. Yes that’s right. They don’t need to do any marketing.

They are the rails on the back end. Consumers do not knowingly do business with Pagaya or visit their website.

They work with major financial institutions like $SOFI, not small banks and credit unions. This gives them a far bigger cushion during economic turbulence.

Pair that with the fact they do not hold the vast majority of loans on their balance sheet and you have two completely different risk profiles.

And also two completely different businesses.

They both have AI driven lending models yes. But they are focussed on completely different things.

Pagaya is embedded within and works with the big boys on Wall St.

Upstart works with small time banks and credit unions in order to drive their own loan volume.

Not competitors, but probably the only company which is remotely comparable.

English

@KairosPraxis New technologies - ALCs and OmniConnect for GPU to memory are coming up - can you name the companies working on this and getting close

English

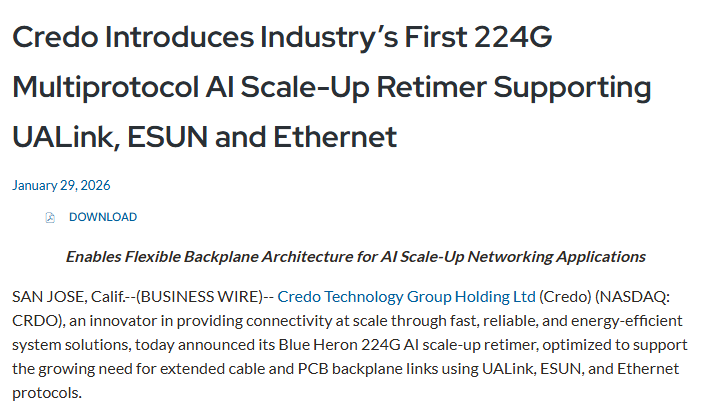

Market is punishing $CRDO because optics... but I really like how the business is positioning itself for the future.

First, AECs aren't going anywhere (copper if you can, fiber if you must). New technologies - ALCs and OmniConnect for GPU to memory are coming up.

The new retimer for scale-up networking (GPUs to GPUs) could be a big deal. NVLink is obviously the boss right now, but as more and more asics come online (or more AMD) hyperscalers will shift to UALink. $CRDO's retimers could become the standard as UALink connects larger and larger racks.

The Scale-up Retimer could end up being a nothing burger (lots of competition) but worth keeping an eye on.

I added to my position at $120, think we're going to have another crazy quarter.

English

@aleabitoreddit My understanding optical cannot handle in GPU/across GPUs at a cost effective/fast way - is any company close to solving this problem using photonic

English

Imagine panicking with $CRDO at $95 ($17B MC).

If you bought then it would be a 52.6%+ gain in a week after today's preliminary ER.

Mid-term fears were overblown. 200%+ YoY revenue growth for this year. $340M guidance -> $406M (huge beat) for Q3 2026 guidance.

That being said, long term risks are still with photonics transitions (since this is medium term guidance).

But, Credo will be a core part of the AI buildout in the future, it just loses it's defacto "leader" status.

The selloff to $95 was may have been one of the biggest dip-buying opportunities this year.

English

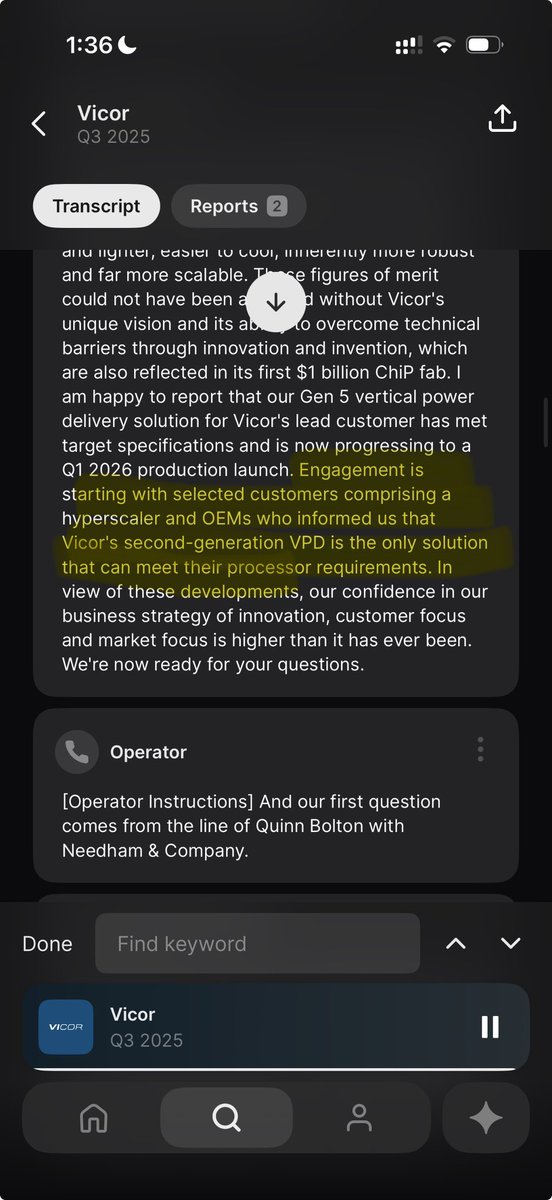

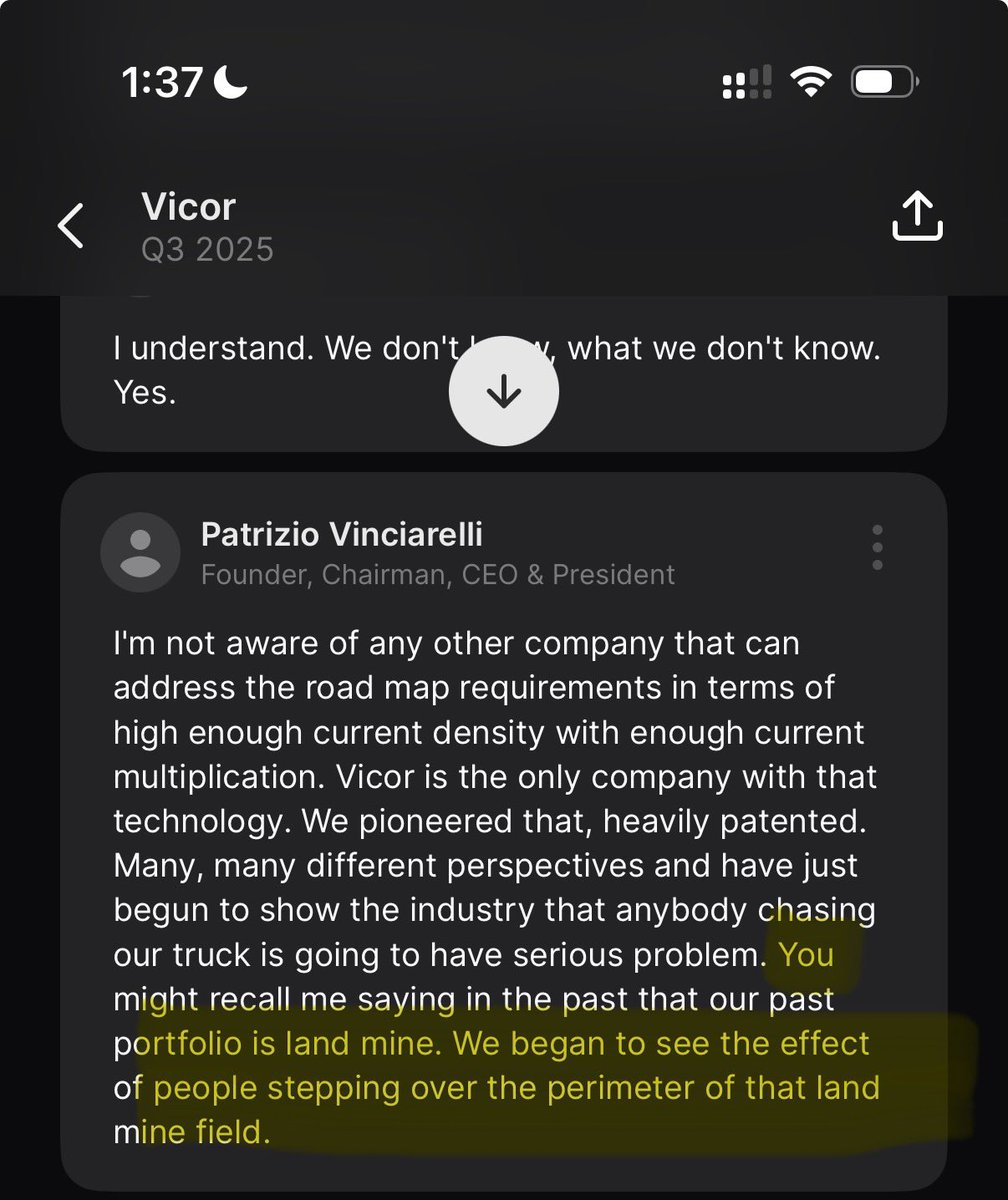

Never heard of Kathmandu Capital but they def know what theyre talking about out when it comes to $VICR.

see what they say and what the ceo/founder who owns damn near half the company was saying on their last call regarding talks with $NVDA $GOOG $AMD $AMZN

Capital Employed@capitalemployed

Vicor $VICR pitch by Kathmandu Capital - leading U.S. designer and manufacturer of high performance power modules. - positioned to benefit from rising AI-driven power requirements and the transition toward HVDC architectures. - offers meaningful margin expansion opportunity.

English

@assface_burner And no rare earth materials - which would have been a real benefit - if he just worked with our allies - it is actually a big loss - another base vs rare materials - think long term

English

Trump is a pedophile rapist

Having said that, the fact that he pulled off this Greenland thing is pretty fucking impressive

English

@assface_burner Greenland has always been open to USA bases - we have one there - no change

English

@assface_burner What did this charade cost? - Credibility. - Trust. - Money. - Reputation. - Friendships. - Alliances. Some costs are still accruing. Some consequences have not yet surfaced. Others will only appear on the global stage, where memory is long and forgiveness is rare.

English

@HenrikZeberg What these Republican morons do not realize is that we have crony feudalism in America and Reagan was the one that killed MFG in this country by shipping jobs to China and ended up creating China - and now they bitch about what they created - selling out labor in US

English

This shows how little you know about Greenland.

What does the US have for Puerto Rico...? Or for the indigenous of America? Or just for the lower middle class in America.

Yeah - wonder why everybody do not want to be American.

Denmark has an intact Social Contract - for starters! Free healthcare. Free education. 5-6 weeks of paid vacation (already from year 1). And a stable society!

You really sure you want to compare Denmark to US....?

Bill Mitchell@mitchellvii

What has Denmark ever done for Greenland? Why in the world would Greenland's residents want to remain with Denmark when they can become part of the Unites States? Trump wins this in the end.

English