statarbed

193 posts

statarbed

@statarbed

Random thoughts on Crypto, Politics, Markets

Katılım Haziran 2020

914 Takip Edilen65 Takipçiler

BYD reports most horrific results in a while (as expected), price up 4%.

Also one of the very veery few China consumer names up YTD (alongside the other EVs).

Basically since Dec/Jan, after a rough 2H25, everyone positioning ahead for the domestic EV market to recover in a couple of quarters (and exports to continue). Maybe. We'll see.

I added because wisdom of the crowds and stuff.

Also option value on Trump Xi meeting announcing Chinese OEMs can create jobs in US (very low chance, UAW etc midterms blah blah, but who knows).

One would imagine UAW would love to be part of a communist enterprise (until they find out the definitions may differ).

English

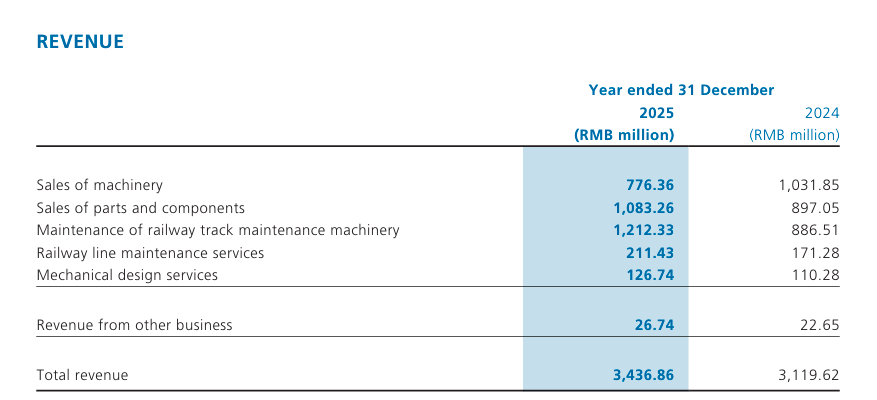

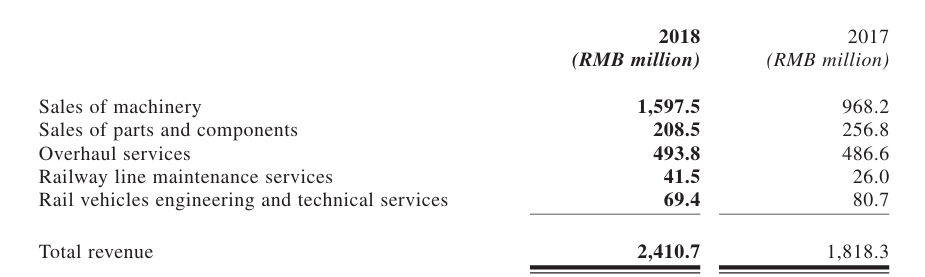

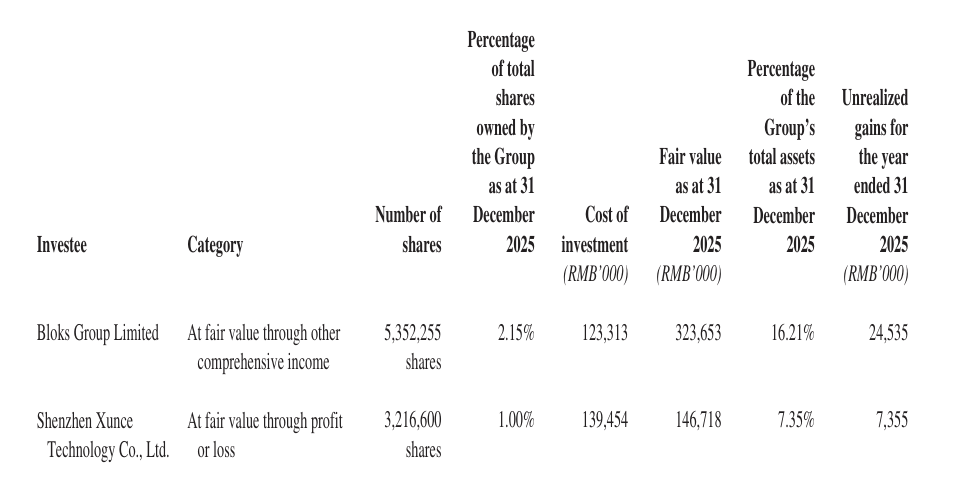

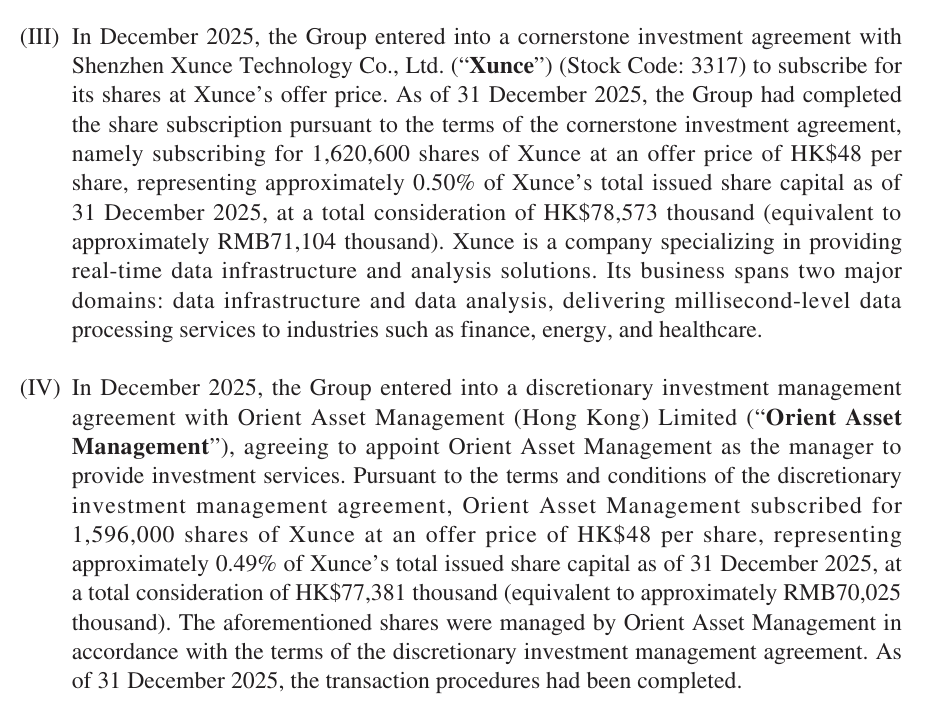

With all the * Deep Value account spopping up, waiting for one called HK/China Deep Value pitching something like $1786.HK CRCC High Tech where Net Cash is 1.4x Market Cap, 0.15x Book, 7x Earnings and where revenue is likely now mostly recurring in a monopoly maintaining rail

English

@veetsam @MikeFritzell So the regular German withholding tax doesn't apply to Haier D?

English

@statarbed @MikeFritzell According to Grok : For Haier D-shares, the primary tax at source is the Chinese 10% WHT.

English

Ten dividend stocks in Asia:

1. Halyk Bank: 13% yield

2. Oriental Watch: 11% yield

3. Best Mart: 11% yield

4. Lion Rock: 9% yield

5. Haier D: 8% yield

6. Capitaland India Trust: 8% yield

7. VTech: 8% yield

8. Concepcion: 8% yield

9. Link REIT: 7% yield

10. Haad Thip: 7% yield

English

After months of talking to people in Singapore, the local media is starting to pick up on Singapore construction cos listed in Hong Kong!

#google_vignette" target="_blank" rel="nofollow noopener">nextinsight.net/story-archive-…

English

@RecoveryTrade What's the catalyst for 0050.HK? Agreed there's a lot of value in the company but it feels like a lost cause as long as they don't return capital to shareholders

English

Cigar butt 'net/net' Cosco Shipping International 517.HK still has a few puffs remaining. Still trading below net cash. Nearly 1.6x 12-month return after including dividends.

Another value investor@RecoveryTrade

@Refinedman2 @bentan__ Since the entire group is listed on multiple exchanges (HKSE, SGX, SHSE), it seems unlikely to me that they will try anything aggressive like underpaying the 29% minorities, as it would frighten the public shareholders of the other (much larger) entities.

English

lol Guming, 11k stores in China already and plan to open 3000 stores a year? what, like 8 a day??😅 (franchises, but still, man).

Godspeed to any sector where 3-4 competitors raise usd1bn in IPO money at the same time. Battle royale.

Food delivery platforms saw it and probably thought "well, since you all have some spare cash now, I have an idea on how we can burn some together". Bubble tea price is going negative like WTI in 2020.

English

Hysan $0014.HK breaking out above HK$16 today! 1H25 results showed resilience in tough HK market: turnover +2.2% to HK$1.73B, profit +1.2% to HK$1.03B. Retail occupancy up to 94% from 92%, office to 92% from 90%, tenant sales +8% YoY. HK$8B new capital recycling goal.

PhilHK@phil_hk

There’s a lot of doom surrounding Hong Kong & HSI. The narrative is that HK’s days as a financial center are numbered. Everyone is entitled to their belief but think this is complete bullocks. I urge everyone to read this to get a better understanding: x.com/phil_hk/status…

English

@phil_hk @RecoveryTrade I'm not picky - special divs, buybacks, any distribution is welcome :)

English

@statarbed @RecoveryTrade The company has a history of doing special dividends, which I also prefer in this type of business. The founder was buying shares at the lows during Covid.

English

Ming Fai Int'l 3828.HK (hotel consumable manufacturer) trades at 1x EBITDA, 5x PE, pays a 10% divvy, with significant net cash position, and decent decent revenue growth. According to CapIQ, David Webb holds 16%. This stock should trade 3x higher.

English

@pandawatch88 I think the overall goal here from the Chinese govt's view is to ensure there is long term competition and innovation. Gross margins will go up, but the govt will expect companies to use most of this additional cash to invest in R&D, increase salaries.

English

On Cluseau's post abt profit upside on Chinese companies, which is an interesting topic to me:

The short answer.

--yes, there is specific margin potential in some names (JD and Xiaomi for sure IMO), but what the government wants is EBIT up, not necessarily MARGIN up. Bigger pie via better more expensive products, and not more efficiency at platform level.

Why? The Long, if you are bored:

--the problem is not low prices leading to low margins at the large internet/chinese listed cos. The margins are actually world class.

(ebit margins: 45% TTG, 25% Meituan well above Dash/uber, Trip 30% same as Booking. BYD margins are 5% CATL 10% but ROCE is 30-40% which is wild for industrial companies in growth mode. These are money machines)

--the problem is the system that produces those margins:

---in the US high margins come from high prices that cover all sorts of corporate fat (good thing, that fat feeds a lot of mouths in the economy who then buy things to project success etc, basic human driven economy, works)

--whereas in China the margins come from max squeeze of process efficiency and stakeholders, from suppliers to engineer salaries to marketing efficiency to no consultant fees no bank fees no outsourced bulsit no late night limos no business class no inhouse psychologist low cloud fees low electric bill etc. The opposite to a US software company or WeWork. This is passed on to consumer via low price.

--what this means is in the US you create a lot of corporate surplus to feed the machine

--and in China you increase disposable income via low prices but you cap/reduce personal income (involution)

--what the government complains about is that pushing more volume through this system by lowering end prices means more squeezing of all stakeholders listed above. Salaries don't go up, suppliers have to work double for the same profit etc.

--what the government ideally wants is more volume through better products not lower prices. Better products have higher prices have higher absolute ebit and feeds more people. They want platform EBIT up, not margin up (and China platform total EBIT has actually doubled since 2019, same growth as in the US).

Now on the two companies mentioned:

-JD margin should go up (if/when the food delivery shenanigans end) just mechanically because marketplace and ads (10% of retail revenue today) are becoming a larger share of revenue. Management has already guided to HSD mid term. The 1P retail margins of JD are prob around 3%, same as WMT/COST. 1P+3P is currently 4% vs Amazon 6%. 2024 top line retail growth for JD was 7% vs 5% for WMT/COST and 10% for Amazon. JD is already a well run retailer (if we ignore the small detail of recent food wars).

-Xiaomi margin should also go up. GM on phones is 13% (you get a lot of tech for your money) and EBIT breakeven. Consolidated EBIT is 6.4% (services and iot compensate for phones and EV). The branding exercise aims at unlocking that upwards. IF they can move phones to from 13% GM to 20%, iot GM from 20% to 30% (like he other white goods cos), and EVs to 5% (like geely Li byd) consolidated EBIT margin goes from 6% to 16%.

going for a hike and a bubble tea

fin

Cluseau Investments@blondesnmoney

Think one of the crazy things about China is the R&D there is excellent. Believe me, no one likes to lampoon China as making cheap trinkets more than me, but what they are coming out with is immense. Xiaomi 15 with 90 W charging? Iphone is stuck at 22 and Samsung at 45. BYD Seagull at $8,000. In the US this would cost $30,000. I think one of the reasons many of us haven't realized what they've been up to is the US has flat out banned their products. Xiaomi, Huawei, etc, you just can't buy these in America. Same for the cars. An interesting trend is the Chinese government likes the R&D competition, but is not happy about pricing. Unlike US companies who enjoy massive profit margins with minimal innovation, it's a fight to the death in China and many companies are just lowering prices to compete, hence the cycle of deflation. The government is literally bringing CEO's into re-education camps to explain to them they have to stop competing on price, and fatten margins up. Almost reverse pricing controls. It's got me thinking about Chinese tech, so many companies are very cheap, like $JD, and running on 4-5% profit margins. Imagine if they increased to 7%?

English

SBI Holdings’ $8473.JT $SBHGF consolidated subsidiary SBI Shinsei Bank has filed a listing application with the Tokyo Exchange in preparation for its upcoming IPO. SBI Shinsei Bank had Y84 bi in net income last year and the IPO could fetch a valuation of some Y1.5 tri according to Reuters. That’s an implied P/E lower than that of SBI Sumishin Net Bank, which was recently sold to NTT DoCoMo and would represent a MCap similar to the total Mcap of SBI Holdings currently.

English

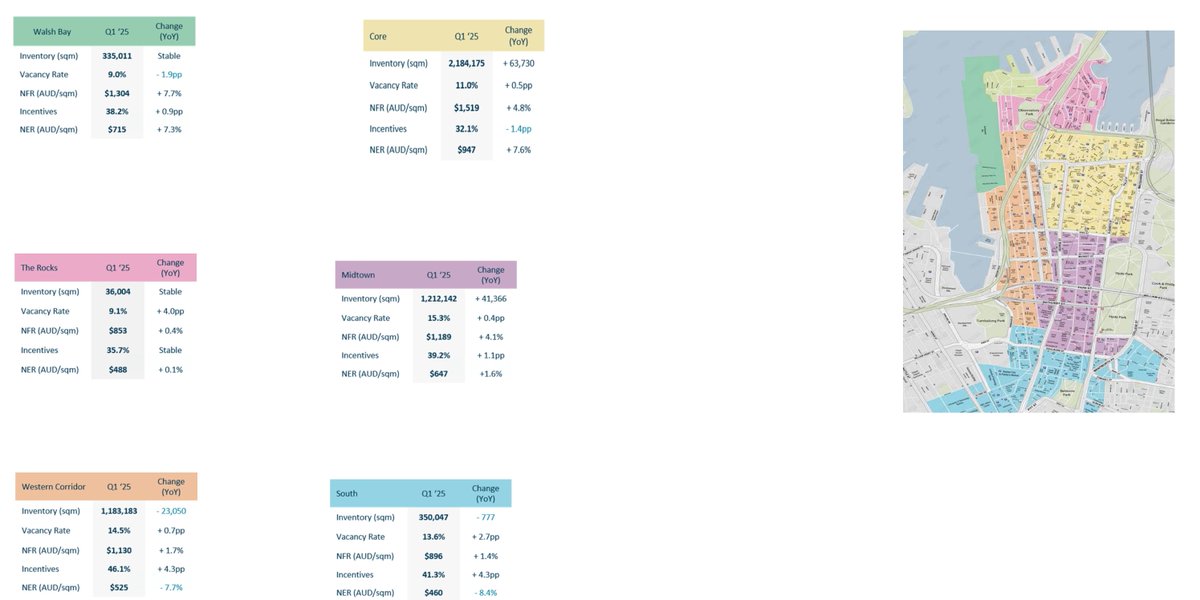

Sydney office vacancies continue to skyrocket.

Pre-covid was ~3.7%.

Midtown 15.3%

Western corridor 14.5%

South 13.6%

Core 11%

Based on who's paying rent. Actuals are higher.

Landlords keep pretending rents haven't crashed.

There will be a reckoning.

English

statarbed retweetledi

We will unfortunately never see another moment like DeFi summer or NFT mania again. Participants are too jaded and there are few true believers left, when new ways to speculate come along the micro cycles get shorter and shorter. If OHM launched today it would be over in 48 hours

English

@JRUrbaneNetwork Why is it so expensive to build? Does this budget include land works around the stations so that the govt can sell development projects?

English

Hong Kong ExCo approved the Northern Link Project (red) today, paving the way for construction to start this year. The 11km 5 station underground line costs an eye watering 1 billion INT$/km to build. The line will shrink travel times from 古洞 to 錦上路 from 60-80 min to 12 min.

English

Someone seems to really like Great Eagle $0041.hk. We have broken out.

PhilHK@phil_hk

Great Eagle reported core profit down 16.1% yoy, but flat when adjusted for one off costs. Company should become almost debt free on a holding level once sales from OnmanTin are recognized (H1 2025?). Seems market liked the report and we are on the cusp of a breakout. $0041.hk

English

statarbed retweetledi

CK Hutchison, the Hong Kong-based conglomerate, agreed to sell control of a unit that operates ports near the Panama Canal after pressure from Trump to limit Chinese interests in the region trib.al/GF4EkKe

English