Sabitlenmiş Tweet

Stocks To Focus for this week

1) GRSE

2) Black Box

3) Hind copper

4) Ashapura minechem

5) Sanduma

No Recommendation | DYOR

English

Stocks Compass

208 posts

@stockscompass

Stock market analyst | Sharing insights & sector trends | No buy/sell Recommendations | Not SEBI-registered. Purely educational

⚡️ What GE Vernova Management Said in the Recent Concall About HVDC, High Voltage & Data Centers - And What It Signals for the Power Market 🔥👇 This isn’t about one company. This is about what transmission commentary tells us about the real power cycle. 1⃣ HVDC – Renewable Evacuation Is Now Structural Management clearly positioned HVDC as essential. Renewables are being built far from load centres - Rajasthan, Gujarat, remote belts. Bulk power needs to travel long distances efficiently and stably. HVDC enables: 1. Long-distance bulk transmission 2. Lower losses 3. Better renewable integration 4. Grid stability They indicated multi-year visibility (~4-year execution cycles) and a continued opportunity pipeline ✅ 📌 This suggests India is building long-distance high-capacity corridors, not just incremental lines. 2⃣ High Voltage Grid Expansion – 400kV & 765kV Push Repeated mentions of: 1. 400 kV bays 2. 765 kV reactors 3. Large MVA transformers 4. GIS substations 📌 This signals grid strengthening at ultra-high voltage levels. Higher voltage means: 1. More power per corridor 2. Lower transmission losses 3. Future-ready backbone This is not maintenance capex. This is preparation for scale ✅ 3⃣ Peak Power Demand Projection – 446 GW by 2030 Management referenced that peak power demand is projected to reach 446 GW by 2030. That is a massive jump from current levels. To handle that: 1. Transmission capacity must expand 2. Substations must scale 3. Grid stability systems must be upgraded Peak demand growth alone justifies HVDC and 765kV expansion ✅ 4⃣ Per Capita Electricity Consumption Target India’s per capita consumption target: 1. ~1,460 kWh today 2. 2,000 kWh by 2030 3. 4,000 kWh by 2047 📌 This signals structural electrification. Rising consumption means: 1. More industrial load 2. More commercial load 3. More urbanization 4. More digital infrastructure Transmission buildout is not optional under this trajectory ✅ 5⃣ Data Centers & AI – The Silent Transmission Driver Management also highlighted massive global data center & AI investments. Data centers: 1. Run 24/7 2. Require ultra-reliable power 3. Are highly voltage sensitive 4. Need strong substations & transformers Unlike residential or industrial demand, data centers cannot afford outages or voltage instability. AI growth = Power infrastructure growth. AI infrastructure is power-intensive. Data center growth → high-voltage demand → grid reinforcement ✅ 📌 This is a silent but powerful multiplier for transmission capex. The above insights are based on commentary shared by GE Vernova management in their recent earnings concall. I have highlighted the key structural signals around HVDC, high voltage expansion, peak demand, and data center growth. If you have any doubts or want clarification on any specific point, drop your question in the comments below 👇 If you want me to cover any specific concall or theme in detail, mention it in the comments as well 👇 Disclaimer: This is for educational and informational purposes only. Not investment advice.

India Commercial Vehicles - The Next Structural Upcycle Is Forming | Nomura Report - Nomura is pointing to early cycle economics turning favourable, setting up the next CV upcycle into FY27 to FY28 - Let’s break what actually changed 1️⃣ Cycle positioning - still early, not crowded ▪️ Indian MHCV cycles typically peak every ~6 years ▪️ Industry volumes are still below FY19 peak ▪️ Nomura sees FY27 to FY28 as the cycle high - Stocks have moved ahead of volumes. - That usually happens only in early cycle phases, not near peaks. 2️⃣ The real trigger - fleet economics flipped What actually changed on the ground: ▪️ GST cut reduced truck acquisition cost by ~8% ▪️ Freight rates improved modestly ▪️ Profit after EMI for operators jumped ~50%+ - This matters more than GDP. - CV demand revives when operators feel cash rich, not when macro headlines improve. 3️⃣ Replacement demand is now unavoidable Nomura highlights a key structural signal: ▪️ Average truck age ~10 years ▪️ Normal replacement age ~7 to 7.5 years Add to this: ▪️ Higher maintenance costs ▪️ Downtime losses ▪️ Rising regulatory costs ahead - Replacement cycles are non discretionary. - Once triggered, demand becomes sticky. 4️⃣ Regulation will PULL demand forward, not hurt it Upcoming braking, safety & ADAS norms: ▪️ Implementation from FY27 onwards ▪️ Estimated cost increase ~₹1 lakh per vehicle Counter intuitive truth: - Operators buy before regulations kick in → pre buying lifts volumes. - Scale leaders absorb costs better → pricing power improves. 5️⃣ DFC fear is overstated - Nomura clarifies Common worry: Rail freight kills trucks. Reality: ▪️ ~70% freight already moves by rail (bulk cargo) ▪️ Non-bulk (~30%) still depends on road ▪️ DFC capacity addition is incremental, not disruptive - DFC causes mix shifts, not demand destruction. - First mile & last mile trucking remains intact. 6️⃣ Segment mix is quietly improving margins Industry trend Nomura flags: ▪️ Shift toward higher tonnage vehicles ▪️ Tractor trailers gaining share ▪️ Better ASPs + operating leverage Company positioning: ▪️ Tata CV - dominant in tractor-trailers & tippers ▪️ Ashok Leyland - strong haulage base, improving mix - This is not just a volume cycle. - It’s an ASP + margin cycle. 7️⃣ Operating leverage still ahead ▪️ Industry utilisation ~55 to 70% ▪️ No aggressive capex needed yet in many Why this matters: - Margins expand faster than volumes in early upcycles. - Best earnings surprises come before capacity tightens. 8️⃣ Where Nomura Sees Asymmetric Upside - The Clean CV Plays Ashok Leyland ▪️ Pure-play India CV exposure ▪️ ~31% MHCV market share ▪️ Margin expansion visibility ▪️ Strong EPS compounding outlook Tata Motors Commercial Vehicles ▪️ ~46% MHCV market share ▪️ India upcycle + Iveco optionality ▪️ Conservative SOTP valuation by Nomura 9️⃣ What could break the thesis (To Track) ▪️ Sharp fall in freight rates ▪️ Govt capex slowdown ▪️ Faster than expected rail modal shift ▪️ Iveco execution slipping - These are monitoring risks, not base case assumptions. 🧭 Investor Compass Takeaway - Nomura is flagging a cycle reset. ▪️ Operator cash flows are stronger ▪️ Replacement demand is lining up ▪️ Regulation supports pre buying ▪️ Leaders gain operating leverage - Early cycle setups reward patience, not excitement. - Earnings upgrades come first. Rerating follows. Source credit : Nomura No Buy/sell recommendation #StocksToWatch #StocksInFocus #AshokLeyland #Tatamotors

Data Centres - Infra & AC firms eyeing big gains 🔥 🔶️ Key Highlights • Strong demand driver AI-led cloud expansion by global & local tech giants • Investments ~$32 bn announced in last 2 years; total sector investment ~$60 bn (2019–24), projected to reach $100 bn by 2027 • Capacity India’s IT load at ~1.4 GW (Q2 2025), expected to double in 2 years • Key beneficiaries L&T, Voltas, Blue Star, LG Electronics, KRN Heat Exchanger • Business impact > Voltas’ data centre share to rise from <5% to ~30% of B2B > L&T seeing rising private sector order inflows > Blue Star focusing on chillers, liquid cooling & partnerships • Why it matters High-margin MEP, cooling & infra opportunities → structural, multi-year growth tailwind for infra & AC players Follow @vishan_khadke for more such updates. @deepak4748 @Akash17971 @Dynamicinvstr @DhawalDoshi5 @EquityInsightss

India’s Solar + BESS Reset – Connecting the Dots - Two excellent articles, one on solar slowdown, one on battery storage rules, together deeply explain a single structural shift in India’s clean energy journey. 1 | THE BIG SHIFT - India’s renewable story is moving from speed driven expansion to system driven execution. ▪️ Solar capacity awards are slowing ▪️ Battery storage rules are tightening ➡️ Not a policy failure. A structural recalibration. From Article : - India’s rapid solar boom is slowing as grid constraints, weak demand growth, stalled contracts and rising storage needs push the sector into a recalibration phase. 2 | WHY SOLAR HAS SLOWED - Solar expansion ran ahead of the supporting ecosystem. ▪️ Generation capacity scaled faster than transmission ▪️ Evacuation infrastructure lagged ▪️ Power produced wasn’t always absorbable ➡️ Capacity hit a grid wall, not a demand wall. From Article: - Power transmission capacity creation is currently lagging growth in generation capacity as there have been delays in ramping up grid infrastructure. 3 | GRID RELIABILITY BECAME THE BOTTLENECK - Once evacuation lagged, reliability overtook capacity as the key constraint. ▪️ Weak grids undermine project economics ▪️ Adding more solar stopped solving the problem ➡️ Reliability > headline GW addition. From Article: - In this situation, ensuring grid reliability becomes critical and slow transmission build out undermines project economics and capacity growth. 4 | DEMAND EXISTS – BUT IT’S UNEVEN AND MISALIGNED - The issue isn’t lack of demand, it’s where and when demand shows up ▪️ New demand centres are emerging (EVs, data centres) ▪️ But overall demand growth is still muted ▪️ Solar peaks in daytime, demand peaks evening/night ➡️ Mismatch makes storage + ToD mechanisms necessary. From Article: - While new demand centres have come up in the form of electric vehicles and data centres etc, the country has not witnessed huge overall electricity demand growth this year. - Time of day pricing… can shift evening and night demand for power to daytime demand, which coincides with availability of solar power. 5 | STORAGE BECAME NON NEGOTIABLE - When demand doesn’t align with solar hours, storage becomes mandatory. ▪️ Grid strengthening alone isn’t enough ▪️ Storage required to shift power ▪️ Solar + grid + storage become inseparable ➡️ Storage becomes a system requirement. From Article: - If a large part of the power demand is not coming up during solar hours, you are naturally going to need more storage and grid strengthening measures. 6 | SLOWDOWN IS A SYMPTOM, NOT THE DISEASE - Lower capacity awards reflect a pause to fix the system. ▪️ FY24 peak followed by slowdown ▪️ FY26 YTD numbers show recalibration ➡️ Pause to fix plumbing, not abandon growth. From Article: - The year wise renewable energy capacity awarded in the country jumped from 9.3 GW in 2022-23 to 47.3 GW in 2023-24, before slipping slightly to 40.6 GW in 2024-25 and finally plummeting to a mere 5.8 GW in the first eight months of 2025-26. 7 | EXECUTION IS STUCK, NOT INTEREST - Projects are awarded but not executable. ▪️ Large backlog of unsigned PPAs ▪️ PSAs stalled due to connectivity issues ▪️ Capital waits for offtake clarity ➡️ Execution bottleneck, not investor apathy. From Article: - Unsigned power purchase agreements (PPAs) also remain sizable at about 40-45 GW as of date. - Power sale and purchase agreements (PSAs) as of September end are stalled due to a variety of factors including lack of connectivity. 8 | POLICY THINKING HAS SHIFTED - The transition is officially acknowledged. ▪️ Focus moving away from adding capacity ▪️ Priority on absorbing power ▪️ Stability over speed ➡️ This line explains both articles. From Article: - The sector has entered that phase, where the focus is shifting from capacity expansion to capacity absorption. 9 | TRANSMISSION IS THE FIRST FIX - Before solar accelerates again, the grid must be ready. ▪️ National grid planning reworked ▪️ Green energy corridors prioritised ▪️ High capacity transmission lines planned ➡️ Grid first. Generation later. From Article: - The government is reimagining development of the national power grid under a ₹2.4 trillion transmission plan for achieving the 500 GW target. - It is prioritising investment in green energy corridors and new high-capacity transmission lines. HOW THE BESS ARTICLE COMPLETES THE STORY 10 | STORAGE IS NOW CORE GRID INFRA - Battery storage has moved from optional to critical infrastructure. ▪️ Needed for peak demand ▪️ Needed for grid stability ▪️ Needed for higher RE penetration ➡️ BESS becomes the backbone. From Article: - More efficient batteries with longer life cycles could be mandated to address grid stability concerns under a scheme that offers incentives to produce 10 gigawatt-hour (GWh) of utility scale power storage. 11 | WHY BATTERY RULES ARE TIGHTENING - As storage becomes critical, quality matters. ▪️ Efficiency determines usable power ▪️ Battery life determines project economics ▪️ Low-quality solutions create future risk ➡️ Quality > cheap capacity. From Article: - One is the criterion of round-trip efficiency to ensure that out of the energy infused in a battery, the maximum quantum is usable by the battery or grid operator. 12 | LIFECYCLE ECONOMICS MATTER Grid storage projects run on long-term PPAs. ▪️ Life cycle must match contract duration ▪️ Mid-life replacement destroys returns ➡️ Lifecycle value > upfront cost. From Article: - The other thing being considered is the life cycle of the battery. - In case a PPA (power purchase agreement) is signed for 10 years, then as per the current global life cycle standards, there would be no requirement to replace the battery to cater for the 10-year period. 13 | SHORT-TERM DELAYS ARE DELIBERATE - Storage rules are under evaluation, not finalised yet ▪️ Standards first ▪️ Capacity later ▪️ Bidding will start only after these criteria are decided ➡️ This is deliberate sequencing to avoid long term system risk, not policy hesitation. From Article: - The bidding process for the scheme will begin once the decision on the new criteria is made. - These conditions weren’t part of the 40 GWh storage capacity bid under the PLI-ACC. 14 | SECTORS THAT BENEFIT ▪️ Power transmission & grid EPC / equipment player ▪️ Grid scale battery storage players with high efficiency & long life ▪️ Developers focused on hybrid / RTC renewable projects ➡️ Capital preference shifts toward reliability enablers. SECTORS IN NEAR TERM PAIN ▪️ Plain solar EPC & panel-only developers ▪️ Low-spec / short-life battery suppliers ▪️ Aggressive low-tariff bidders in standalone solar ➡️ Speed without system readiness gets penalised. 🧭 Investor Compass View The market is moving from: - Adding GW fast ➡️ Delivering reliable, usable power - Solar alone no longer works. - Grid strength + storage decide value. - Policy is sequencing: Fix evacuation and standards first, scale later. - Solar, grid & storage are now one integrated stack. Source : Bussiness Standard & Mint No Buy/Sell Recommendation #StocksInFocus #StocksToWatch #Solar #BESS #FDRE

India’s BESS Roadmap Is Here - One of the most insightful concalls this Quarter - If you want to know the future of BESS in India, this concall is your cheat code. - Here’s why every serious BESS investor must listen to this call ⤵️ 1⃣ Energy Storage: From Optional → Mandatory 🗣️ “Almost all new solar projects are now coming with an energy storage capacity… if you are setting up 1 GW or 500 MW, around 25-50% of that is now requested as storage backup.” ▪️Solar + BESS is now industry default, not optional ▪️Solar projects are no longer built alone – 1/4th to 1/2 of capacity is now paired with batteries ▪️This ensures power is available even at night, not just when the sun shines ▪️Creates steady, guaranteed demand for battery materials ▪️ Backed by government tenders (SECI, NTPC) making storage mandatory ▪️ Perfectly matches Neogen’s CAPEX timing – their new plant will be ready just as demand explodes 2⃣ TAM Explosion – 100 to 150 GWh of BESS Needed 🗣️ “India’s 500 GW solar target by 2030 can mean 30-40 GWh annual storage demand, adding up to 100-150 GWh over next 4-5 years.” ▪️India will need 30 to 40 GWh of batteries every year just for solar ▪️Adds up to 100–150 GWh demand by 2030 – a giant market ▪️Makes BESS as big a driver as EV batteries ▪️Multi-year growth runway for Neogen – demand visibility till FY30 ▪️Opportunity to capture global market share as a non-China supplier 3⃣ Demand Is Already Real – Projects Tendered 🗣️ “There were around 10-12 GWh of energy storage projects already tendered last year, which will come over a two-year period… around 5-6 GWh is on average consumption for energy storage already there.” ▪️This is not just a future story – demand is live and rolling ▪️5-6 GWh annual base already being executed ▪️Provides early revenue opportunity for Neogen ▪️Reduces utilization risk for FY26-27 – capacity will find buyers ▪️Builds confidence that the market is moving from concept to reality 4⃣ Domestic Giga-Factories Coming Online 🗣️ “Ola wants commercial ops by Sep-Oct 2025… Exide trials started Aug 15… Reliance, Tata, Waaree, Amara Raja are all targeting 2026 commissioning.” ▪️Multiple giga-factories going live in next 12-18 months ▪️Syncs perfectly with Neogen’s Pakhajan capex completion (Mar 2026) ▪️Provides strong utilization visibility from H2FY26 onwards ▪️Ensures demand ramp-up is immediate once capacity goes live ▪️Reduces risk of idle assets – revenue growth will follow capex 🧭 Investor Compass View – Big Picture on BESS ▪️Storage = Grid Backbone – Solar/wind need 24x7 balancing, making BESS mandatory. ▪️100-150 GWh Demand – Locked-in runway over next 4-5 years. ▪️Policy Push – SECI/NTPC hybrid tenders + PLI for batteries driving adoption. ▪️Execution Visible – 10-12 GWh projects tendered, giga-factories going live. ▪️Global Shift – Non-China capacity key as US/EU diversify supply chains. ▪️Mega Theme: BESS will be as big as EVs in India’s energy transition. ✅ Batteries are the new grid infrastructure powering India’s clean energy future. No Buy/Sell recommendation #StocksInFocus #StocksToWatch #Neogen #BESS #batteries #waaree #Amararaja #ola #tata #exide #EXIDEIND

India’s Defence Flywheel is Spinning Fast 🇮🇳🛡️ A robust ecosystem is emerging across every layer - from drones to destroyer: 🔖 Bookmark & Repost ✉️ ▪️ Defence & Aerospace Bharat Electronics Limited (BEL) Hindustan Aeronautics Limited (HAL) Bharat Dynamics Limited (BDL) Data Patterns Apollo Micro Systems (AMS) Krishna Defence & Allied Industries Ltd Unimech Aerospace and Manufacturing Limited (UAML) MTAR Technologies Ltd Azad Engineering Ltd NIBE Ltd Avantel Ltd Techera Engineering DCX Systems Adani Defence Paras Defence Dynamatic Technologies Lokesh Machines Rossell India Macpower CNC Machines Tembo Global Industries AXISCADES Technologies Premier Explosives Sika Interplant Systems Mishra Dhatu Nigam Ltd Jyoti CNC Automation PTC Industries Solar Industries Jaykay Enterprises Swan Defence and Heavy Industries Mahindra Aerospace Tata Advanced Systems ▪️ Land Systems & Military Vehicles Ashok Leyland Bharat Forge Larsen & Toubro Tata Motors Mahindra & Mahindra BEML ▪️ Shipbuilding & Naval Systems Garden Reach Shipbuilders (GRSE) Mazagon Dock Shipbuilders (MDL) Cochin Shipyard CFF Fluid Control Ltd Larsen & Toubro Shree Refrigerations Hindustan Shipyard Limited (HSL) ▪️ Drone-Anti Drone & Unmanned Zen Technologies ideaForge Technology Droneacharya Aerial Innovations Paras Defence and Space Technologies Garuda Aerospace Adani Defence Drone Destination Asteria Aerospace Limited ▪️ Cybersecurity & Telecommunication Expleo Solutions Ltd. Tac Infosec L&T Technology Services Sahana Systems Astra Microwave Products Ltd ▪️ Electronic Systems & C4ISR Data Patterns Bharat Electronics (BEL) Tata Elxsi Centum Electronics Paras Defence Electronics Corporation of India (ECIL) 💭 Are you holding or tracking any of these defence companies? 🚫 No Buy/Sell Recommendation. #Defence #MakeInIndia #ViksitBharat #ViksitBihar #StocksInFocus #Nifty @Chart_Wallah108 @deepak4748 @suryachaudhary1 @sriranganek @tsatwork @TheAlpha10X

Big AUM ≠ Big Alpha | India’s Mutual Fund Reality Check - Many chases large AUMs. - But do India’s biggest active equity funds consistently deliver alpha? - Value Research answers that and the insight is worth bookmarking. Let’s decode ⤵️ 1⃣ Size ≠ Skill – Consistency is the Real Compounder - India’s largest equity funds by AUM aren’t always the best performers. ⬇️ Axis ELSS Tax Saver - AUM: ₹35,000 Cr+ Rolling 5Y outperformance: - Only 54% of the time - 5Y return: 18.4% vs category avg 24.5% ⬇️ Mirae Asset Large & Midcap - AUM: ₹39,450 Cr+ - Underperformed across 3Y, and 5Y periods - Yet remains one of the top AUM funds in its category ✅ Parag Parikh Flexi Cap ✅ ICICI Pru Large Cap - Both beat category average in 100% of daily 5Y rolling periods Insight: ▪️Big AUM = marketing reach, not alpha. ▪️Discipline > distribution. ➡️ Rolling returns = true test of consistency ➡️ Size ≠ skill, discipline compounds, not corpus 2⃣ Consistent Winners – Who Outperformed Most Reliably - Not all funds need to outperform every time, but a high hit rate matters. 🔹Parag Parikh Flexi Cap – 100% of the time 🔹ICICI Pru Large Cap – 100% 🔹Nippon India Small Cap – 100% 🔹Mirae Asset Large & Midcap – 98% 🔹ICICI Pru Value Discovery – 88% 🔹HDFC Midcap Opportunities – 80% Insight: ▪️High rolling outperformance = robust process across market cycles ▪️It shows a fund doesn’t just perform, it performs predictably ➡️ Consistency is what builds conviction in SIPs 3⃣ The Silent Alpha Engines – Strong CAGR with Low Noise - These funds delivered superior 5Y returns vs their category peers: 🔹 Nippon India Small Cap – 38.6% vs 34.8% 🔹HDFC Midcap Opportunities – 32.9% vs 30.2% 🔹ICICI Pru Value – 29.2% vs 28.0% 🔹Parag Parikh Flexi Cap – 26.8% vs 22.9% 🔹ICICI Pru Large Cap – 24.5% vs 21.6% Insight: ▪️These aren’t flavour of the year winners. ▪️They combine alpha + process + repeatability. ➡️ The best alpha stories don’t trend, they compound silently 4⃣ Rolling Returns > Point-to-Point Performance ▪️5Y CAGR tells you what the fund earned ▪️5Y rolling tells you how often it earned that return ➡️ Parag Parikh, ICICI Pru, HDFC Midcap ▪️Didn’t just outperform once, they did it again and again Insight: ▪️Rolling returns smooth out market noise ▪️They show whether you’re betting on a process or just a lucky streak ➡️ In volatile markets, frequency > flair 5⃣ Axis ELSS – A Case Study in Missed Potential - Despite massive AUM and investor base: ⬇️ Axis ELSS ▪️Underperformed 46% of the time in 5Y rolling ▪️Trailed category in all major timeframes ▪️Still one of India’s top ELSS funds by inflows Insight: ▪️Brand memory ≠ performance ▪️Past pedigree doesn’t guarantee future alpha ➡️ High AUM without delivery is just dead weight on your portfolio 6⃣ The Checklist That Actually Matters - When choosing a fund, don’t just look at return %, look at: ✅ % Time Beat Category Avg (Rolling) ✅ Return Spread vs Category (CAGR gap) ✅ SIP Experience Across Cycles ✅ Fund Manager Tenure & Strategy Continuity Insight: ▪️Alpha is earned through process and patience ▪️Data-backed conviction beats star ratings ➡️ Long-term wealth comes from boring, consistent funds 7⃣ Investor Compass View – 3 Funds That Pass Every Filter - If you're looking for long-term compounders that deliver with discipline: 🔹Parag Parikh Flexi Cap – Global scope, process-first 🔹HDFC Midcap Opportunities – Consistent alpha engine 🔹ICICI Pru Large Cap – Quiet compounding with wide safety net Why they stand out: ▪️Proven track record across timeframes ▪️High-frequency outperformance ▪️Strong CAGR + Low volatility ➡️ These funds are built for investors who think in decades, not quarters ➡️ Back data, discipline, and durability, the only alpha that lasts. Source : Value Research #MutualFunds #MF #MutualFundsSahiHai

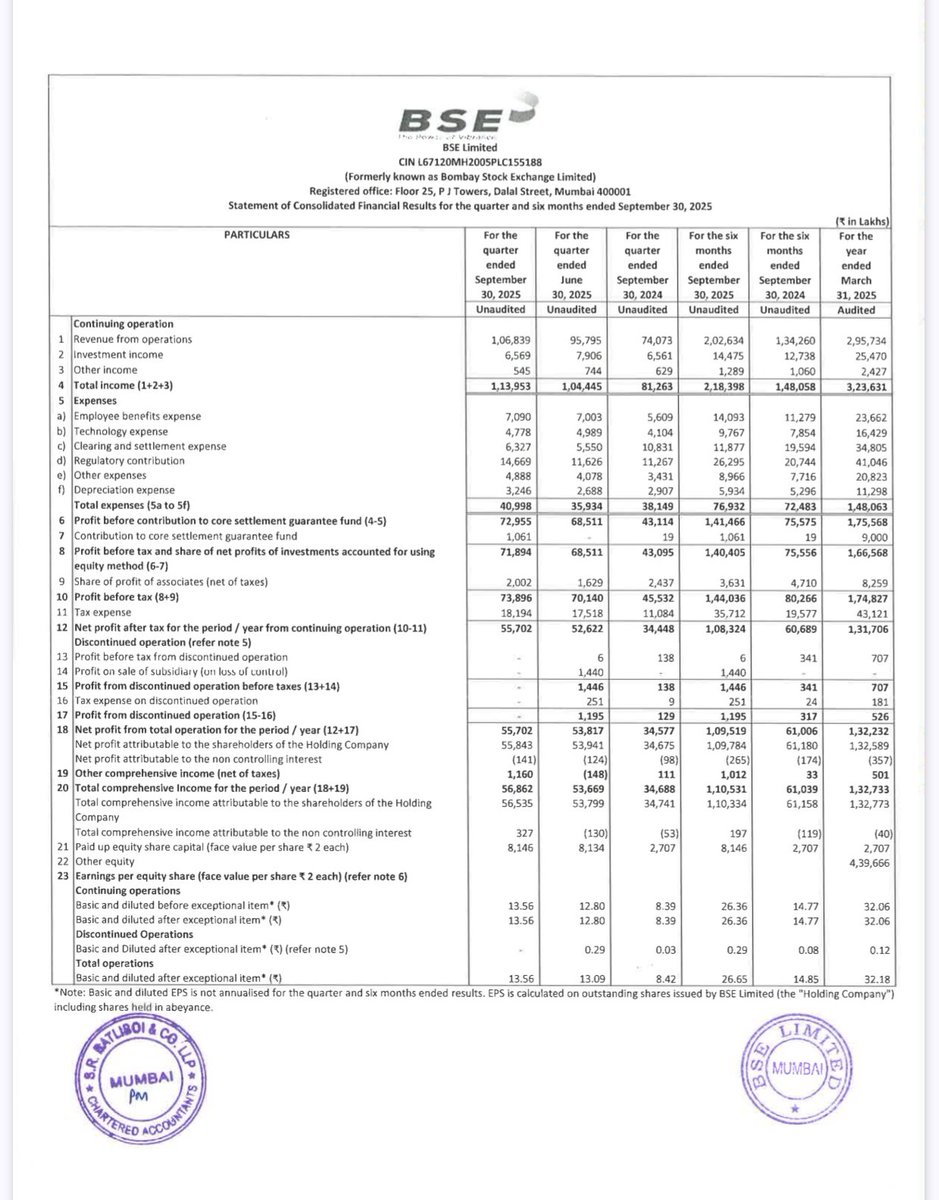

BSE Ltd. 🚀 Blockbuster Q1FY26 - Highest top and bottom line on quarterly basis 🔥 ➡️ Revenue at 1044cr, up by 57% YoY & 12.5% QoQ ➡️ PAT at 526cr, up by 100% YoY & 7% QoQ