@aleabitoreddit @CoastalInvstmnt I want to get out but don’t want to sell for a loss…

English

Imverymad

32 posts

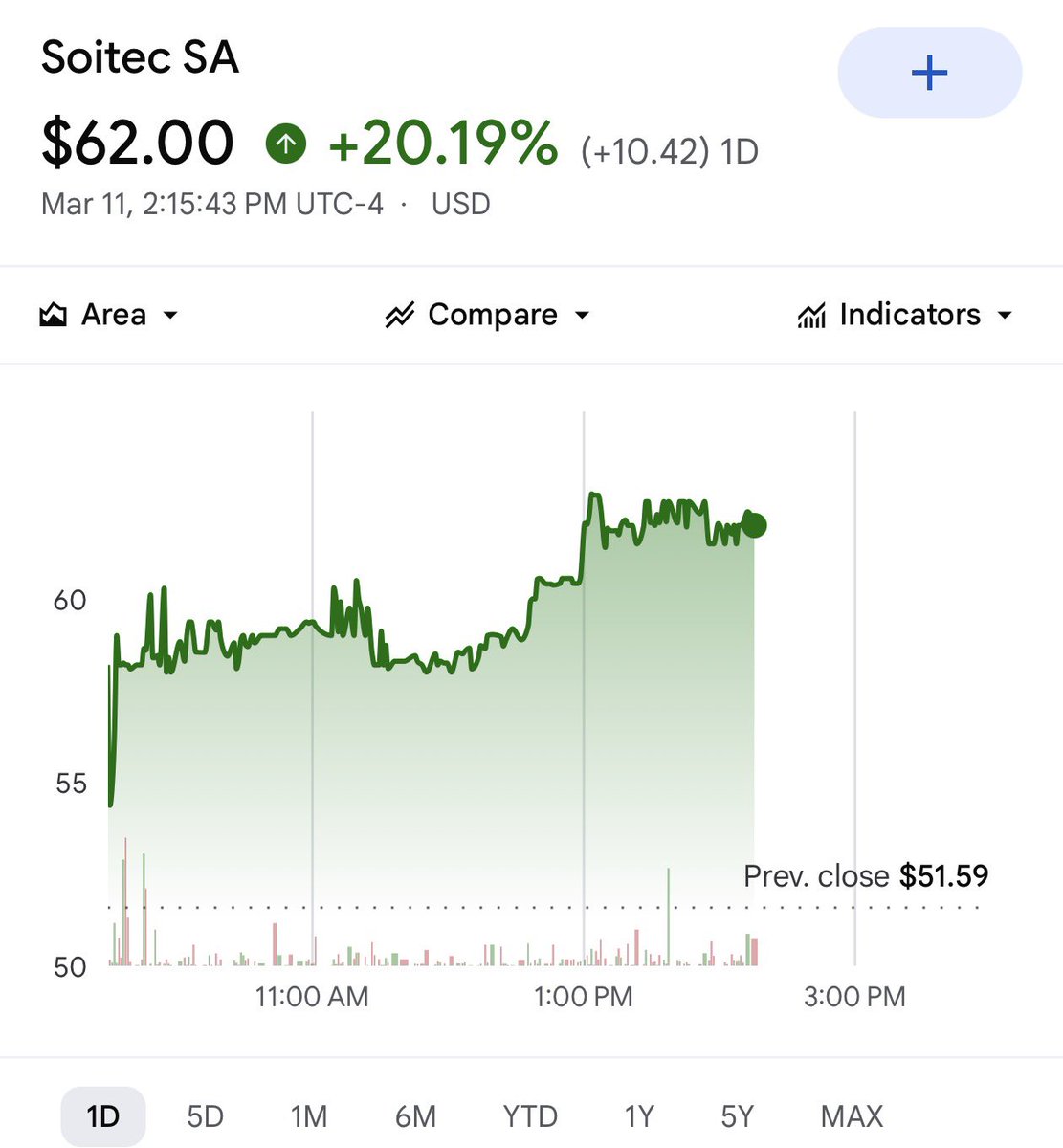

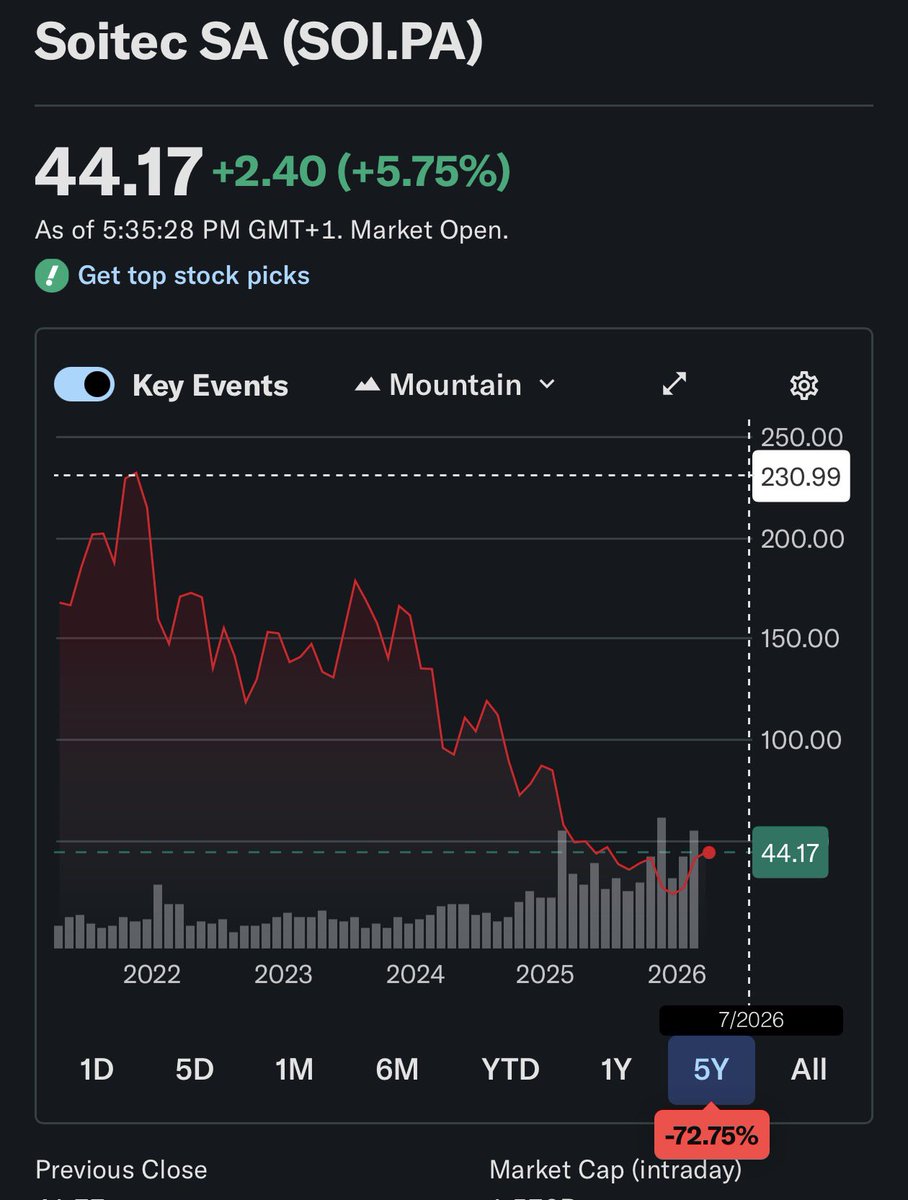

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.

$BTC MIRRORING 2022 COLLAPSE

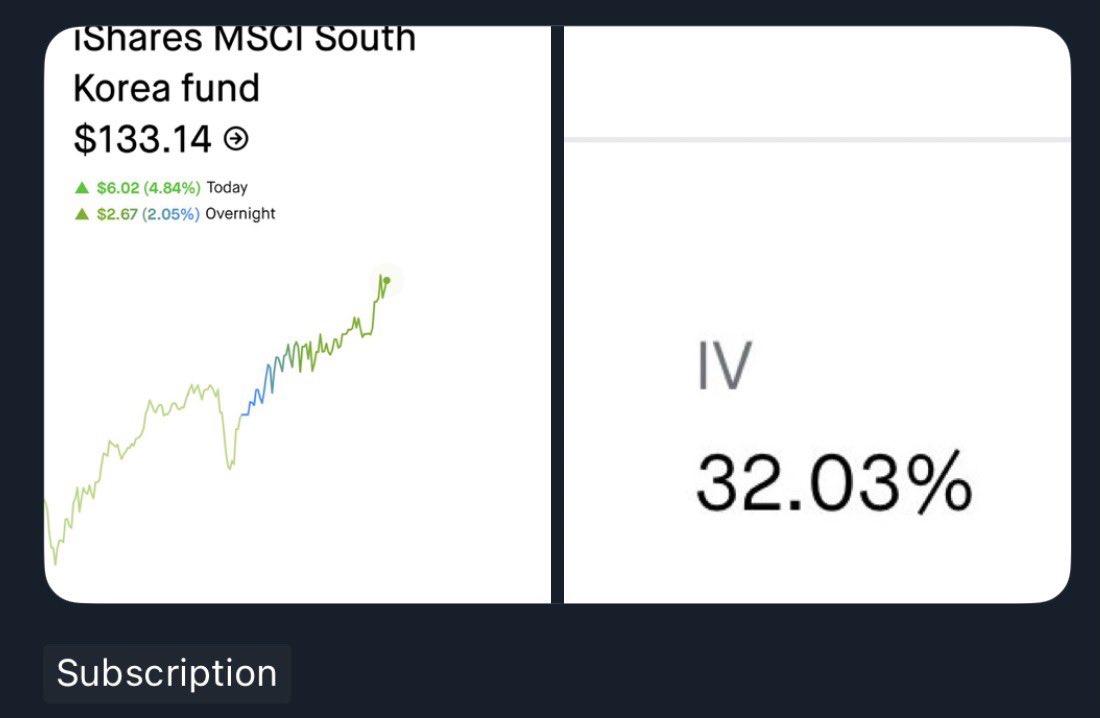

Trade idea that I published to my shower thoughts channel: Korean Index volatility arbitrage and taking advantage of Black-Scholes models. $EWY long options seem mispriced. This is Blackrock's Korea Index, which is majority memory (Samsung Electronics, Sk Hynix). The stock swings 2-5+% a day, and is up 136.25% 1Y, despite priced like a normal index IV. Samsung is volatile. SK Hynix is volatile (eg. 65% - 80% est). But the combination of the two through the index is priced way less than both low beta $GOOGL (37.33%) and $AMZN (39.12%) at ~32% IV. I've been watching $EWY for a bit and it does look volatile. As for pricing my guess is MMs priced in IV based on historical averages (5-10 years), where the Korean index was completely flat. And were expecting calls 2 years out to revert to the mean. But this volatility should be the new norm as markets price in the new memory supercycle (eg. $TSM went from 30% IV to 46.2% IV). Long calls should benefit from both Samsung + Sk Hynix carrying the index. And the main benefit is vega expansion that you won't get from $KORU. You also can't get this option MM pinning like individual US stocks since this is Korea's national index and long term. TLDR: Individual components SK Hynix + Samsung are highly volatile. They're basically half of the index, but options in index are priced with low volatility, perhaps due to historical 5-10 year data. Long calls benefit from vega expansion that weren't priced in correctly as MM forward vol estimates are anchored too heavily on historical realized vol, which was low for $EWY over the past 5-10 years