--

808 posts

--

@technicalanysis

No financial advise - warning people for blatant european scams

- Katılım Eylül 2017

453 Takip Edilen82 Takipçiler

Kijk, het is natuurlijk een grote mindf#ck met gemixte signalen. Crasht het door is het achteraf logisch en draait het omhoog is het achteraf logisch. Korte daily timeframe onder de MA200 dag gesloten, maar weekly timeframe nog ruimte! Wat ik doe is hedgen met short edelmetalen (deed ik al!) en zeer korte put(spreads) die maandag + dinsdag expireren. Komende week gaat cruciaal worden voor mijn scenario's! Maar gek genoeg heb ik al die tijd geroepen na Iraans nieuwjaar omhoog draaien. Dan kan er dus een bodem staan vandaag. Niet helemaal volgens het Nikkei scenario qua prijsactie, maar wel volgens het tijdsschema.

Nederlands

Did I get it right?

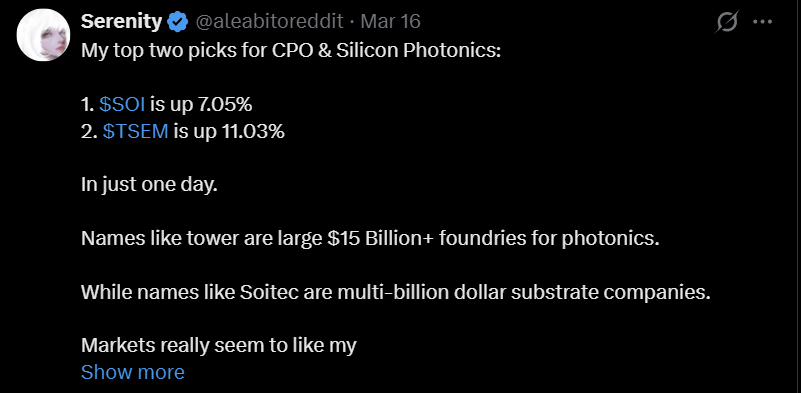

Just last week, the biggest focus was on $TSEM and $SOI, absolute best, long on those names.

This week $SIVE is everywhere as the best name.

Here's what I noticed:

$AXTI was the best, then it slowed down, then

$LITE was the best, then it slowed down, then

$AAOI was the best, then it slowed down, then

$SOI was the best, then it slowed down, then

This week is $SIVE.

Once it drops 10%, it'll stop being mentioned.

Great calls all around (it's something I'll never be able to do, so hats off) but have to notice the moment stock jumps it's interesting, the moment it slows down it's not mentioned or mentioned rarely.

$IQE was spammed for weeks, but then it dropped, just to jump 30% one day and got mentioned. Now, I guess it'll be forgotten again. Same goes for $ALMU, $AEHR, $POET etc.

Besides getting rich on these calls, the user behind the account is very good with engagement and focusing the hottest stock in the given moment. Smooth mention of tickers to increase views is also done in a smart way.

This industry is something I don't understand, but since the posts are all over my feed I have to share what I'm noticing. Maybe I'm wrong.

I'm sure plenty of you benefit from these posts, congrats! If people are interested in this industry, having this type of accounts is useful, especially since all of it is for free.

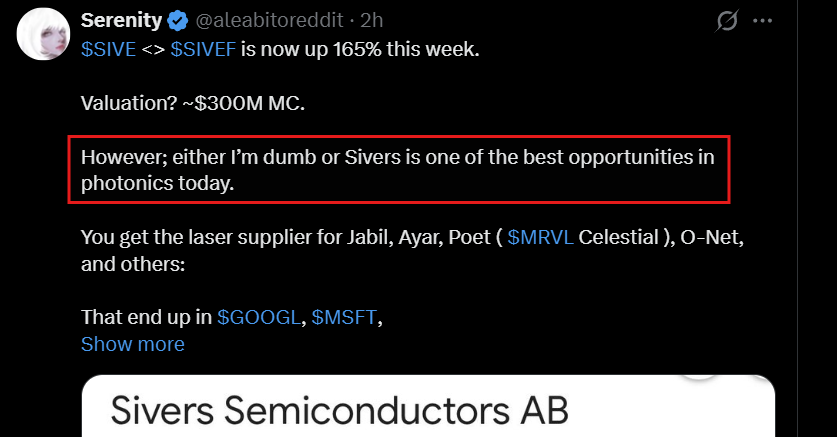

Serenity@aleabitoreddit

$SIVE <> $SIVEF is now up 165% this week. Valuation? ~$300M MC. However; either I’m dumb or Sivers is one of the best opportunities in photonics today. You get the laser supplier for Jabil, Ayar, Poet ( $MRVL Celestial ), O-Net, and others: That end up in $GOOGL, $MSFT, $AMZN, $META AI datacenters. At ~$300M. The EML laser suppliers today from $LITE to $COHR for reference are $45B+ This is one of the most undiscovered yet critical bottlenecks for future upstream photonics supply chains. That markets have only starting to price in today.

English

Very impressive find

Moody@MoodyWriter13

$AIXA controls ~90% of InP MOCVD reactors and every one ships with LayTec metrology inside, the only provider ensuring atomic-level precision. LayTec is owned by Nynomic (M7U), a tiny German photonics group valued below its book value. open.substack.com/pub/fwriter/p/…

English

@CHItraders Tonner drones - $altd is a better alterative. Also has a stake in SpaceX

English

SWARMER IPO: DRONE SWARM HYPE

$SWMR pops in premarket after pricing IPO at $5/share for ~$15M raise—because nothing says "defense tech moonshot" like starting small and hoping for swarm magic.

🔹 3M shares offered, underwriter greenshoe for 450K more.

🔹 Cash for ops, hiring, drone integrations—combat-proven AI already logged 100K+ missions since '24.

🔹 Austin HQ, Ukraine/Poland/Estonia footprint—war-tested software licensing to drone makers.

English

I feel like markets should value:

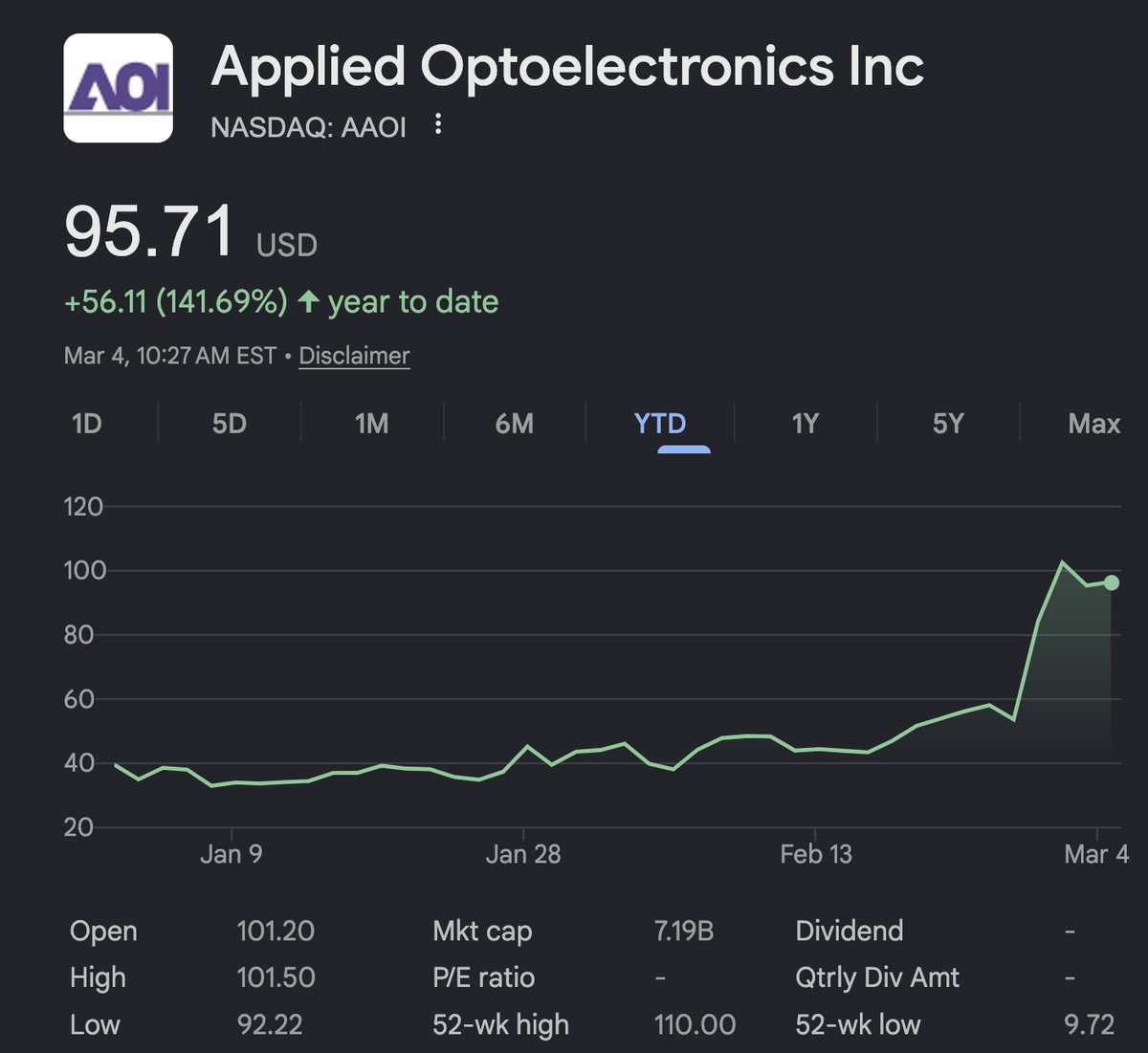

$AAOI $93 -> $162 (~$13B MC) after their new capacity projections today.

and

$SIVE should be valued at 7.7 -> 38.5 ($1.1B MC) at least?

If one is ramping to ~$1.97B capacity EOY 2027 (which is basically revenue, since hyperscalers are buying anything they can make)

Then the other is the likely laser supplier to hyperscaler supply chains from $AMZN Trainium to $MSFT Maia Clusters?

At the very least, should price in forward revenue growth.

This is including execution uncertainty, and without premiums assigned to others like $LWLG at $1.1b+.

If Win semi qualifies $SIVE and $POET/Ayar/and others scale up. I feel like $SIVE valuation could easily 20x-30x from here?

If $AAOI hits $378M/month projections, could easily 5x from here to a ~$30B MC.

These possible price targets is how insane the optical supercycle is (like memory), but largely depends on how each company can execute.

English

The more I look into Sivers

< $SIVE / $SIVEF >

the more I wonder:

How is the laser company for the hyperscaler photonic supply chains…

Valued at ~$200M USD MC?

All the companies that buy and repackage their lasers are now worth $1-4B+?

Pre-product SV AI companies are worth billions?

Pre revenue Photonic companies in development phase line $LWLG are worth $1B+?

Yet the company that makes the silicon photonics/CPO scale up & scale out work.

And has actual revenue.

~$200M…

Reminds me of early $AXTI when I had zero clue how a company worth $500M MC controlled the InP substrate/feedstock supply chain for photonics.

Either I’m completely wrong… or this is the most undervalued and unknown photonics company on the market.

Serenity@aleabitoreddit

$SIVE is the upstream laser supplier for CPO and Silicon Photonics. They're the likely $COHR / $LITE type future light source for: - $AMZN Trainium Clusters - $MSFT Maia Clusters and possibly other hyperscalers like $META MTAI and $GOOGL TPU clusters. At a ~$200M MC. Relational Mapping (speculative): $SIVE (light source) -> $POET (optical interposers) -> $MRVL (Likely Celestial Captive) -> $MSFT Maia + $AMZN Trainium. $SIVE (light source) -> Ayar -> AiChip -> $AMZN Inferentia/Trainium $SIVE (light source) -> Enablence -> O-Net -> ? Asia Hyperscalers _ Ongoing: $SIVE (light source) -> Ayar -> GUC -> ? (Google $TPU) $SIVE (light source) -> Ayar (TeraPHY/SuperNova)-> Wiwynn (captive CPO) -> ? ( $MSFT, $META historically Wiwynn's largest clients). Because of captive models like $MRVL Celestial, they get a free ride. However, they do compete multi-source ELS against Lumentum, Coherent, and $MTSI with Ayar and win anyway in merchant models. But they win either way. For high-volume production ramp up, a large part of it depends on the ongoing Win semi qualification, but this will likely be a large indicator. Again supply chain BOM is extremely confidential. $AMZN will never tell anyone "Hey, we use $SIVE ". But if you put 1+1+1+1+1 together, you can piece together the likely suppliers. Most people see "Poet Starlight" uses $SIVE. Or Ayar uses $SIVE. But don't map all the multi-hop relations to see where they end up. I do think $SIVE is an extremely undiscovered opportunity as the next possible mini $LITE for Silicon Photonics at $200m MC. As they're the likely upstream laser supplier for hyperscaler supply chains for future CPO/Silicon Photonics scale up with cw dfb lasers and scale out with laser arrays.

English

@NCheron_bourse Check out $swmr - Drone IPO in US could weigh on sentiment of Tonner Drones

English

Tonner drones

(demande de mise à jour d'un lecteur)

Haussière à moyen terme, en trendfollowing au-dessus de MM200 jours, proche des prix, en soutien.

Une oblique passe par les plus hauts récents et bloque l'ascension des prix pour le moment.

En d'autres termes, une accélération au-dessus des 0.0360€ serait un signal fort.

Point positif, les volumes sont fournis ces dernières semaines et les replis payés par les acheteurs.

Toujours actionnaire pour ma part, à noter le caractère ultra spéculatif de ce petit titre parfois peu liquide.

Français

English

@raghavrmehta @aleabitoreddit It was up almost 30% 3 minutes after he posted so I'm gonna assume it was something else before. I can't believe it was up 30% that fast from him. Most can't even buy the stock

English

$SIVE is now up +73.78% today ($231M MC).

As markets price in information synthesis of the next potential $LITE of photonics.

If I had to explain the difference:

One laser source in Lumentum primarily benefits from current optical bottlenecks.

The other in $SIVE is for the upcoming CPO/Silicon Photonic bottleneck.

Lumentum is largely benefiting right now from $NVDA and hyperscalers securing capacity of EML lasers for current pluggable optical transceivers cycles.

As seen with the current EML bottleneck, hyperscalers are buying out any 800G/1.6T transceiver + upstream capacity from:

- $AAOI (in-house)

- $COHR, $LITE (EML lasers + design) -> $FN (assembly)

- $COHR, $LITE (EML lasers) -> Innolight / Eoptolink

What's next?

Silicon Photonics and Co-Packaged Optics.

The architectural shift to CPO requires massive arrays of high-power CW DFB lasers.

And this would likely trigger a complete, sudden paradigm shift in volume demand.

$SIVE benefits from InP CW DFB lasers for SiPh and CPO:

The up and coming companies like:

$AYAR, $POET source $SIVE lasers, but primarily do advanced packaging.

Then they feed up to larger companies like $MRVL Celestial (that buy $POET's interposers).

However, if you go upstream, the light source is $SIVE.

CW DFB lasers are light engine ( $SIVE ); the silicon photonics package ( $POET and others) is how it gets transmitted.

CPO scale is not there yet. But we know it's coming.

And as seen with current optical transceiver cycles:

- Light sources from $LITE and $COHR demand much higher valuations than companies like $FN that focus on advanced packaging.

Markets have been focusing on $POET, but missed where they get the actual $LITE type light source for Starlight.

The risks are present including facing multi-source competition with $LITE, $COHR, $AVGO, and others. So again, make sure to do your own research.

But my argument against that:

Sivers been early enough to tailor custom lasers to fit $POET, Ayar, and other specifications before they got popular (sort like the $POET to $MRVL Celestial analogy).

There's volume risks as well:

But the potential Win Semi qualification offsets that.

Dilution risk to scale capacity, is always present with every early-stage company as well.

I did my thesis on $LITE last year and still love the stock for Google TPU ramp/OCS.

But this year, I'm focusing on:

$SIVE, as my personal CW DFB laser exposure for the new photonics architectural shift.

I’m sharing my own thoughts on capturing the rotation from the current EML cycle to the upcoming CW DFB/Silicon Photonics cycle.

Serenity@aleabitoreddit

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

English

English

High conviction long: $AAOI.

I genuinely think this could easily be a 3x by next year.

Nvidia funded $COHR, who does Malaysia manufacturing for 800G/1.6T.

$LITE uses FN in Thailand for volume production, and has it's own manufacturing in Thailand.

I will keep hammering this home but Applied Optoelectronics is only pure Made in America, optical transceiver play.

Again, the two "American" optical companies outsourced it to Asia, while $AAOI spent the years building up capacity and fabs in Texas.

Nvidia funded both $COHR and $LITE just now to build out a US-version to insulate its most critical supply chain from geopolitical risks.

But guess who already has the supply chain setup and is years ahead in that regard? $AAOI.

$LITE ($55B) FY 2026 est. ~$2.91B

$AAOI ($7.1B MC) H2 2027: $4.35B ARR.

$AAOI will actually leapfrong Lite FY 2026 projections if management executes (and with ~40% gross margins).

Once again. $AAOI ($7B) will leapfrog $LITE ($55B MC) entire 2026 revenue projections if they deliver their projections.

$FN over in Asia, 2026 projections are actually around the exact same as AAOI.

~4.39B revenue off 12.4% gross margins. And it's a $20B MC (with much lower margins)

Even if $AAOI hits 70% of their target, it's likely to be heavily re-rated way past it's current marketcap.

TLDR: Hard to see downside with $AAOI at these levels, especially with 3-4 hyperscalers (likely $GOOGL, $MSFT, $AMZN) wanting to buy up any capacity it can make for years out. And with $GOOGL not going the CPO route.

$AAOI leapfrogs $CRDO, $ALAB, $LITE, and others in growth + benefits from photonics theme vs. copper (from the first two).

$AAOI remains an asymmetrical 1Y high conviction as long as management delivers.

English