Teedub

106 posts

Teedub

@teedubposts

interested in politics, history, real estate, technology, investing, travel... (but not necessarily in that order)

United States Katılım Temmuz 2023

501 Takip Edilen102 Takipçiler

@scottmelker ...and maybe the car was never the point.

The road trip.

The people in the passenger seat.

The feeling of having earned it.

The memory attached to it.

Objects are often just containers for experiences.

English

Short story.

I bought my dream car.

It felt great for a few days.

Then it mostly sat unused.

Then it became an annoying expense.

Then I sold it and realized, once again, that material items bring me no joy.

English

@scottmelker Perhaps you are doing it wrong. Love my toys… but family is always first. Enjoy my ability to buy fun things and share with others, including my kids and close friends.

English

@DeepVaue_Adv @BoxLongs Hmmm. I have been on waitlist since they first posted about Zaira, with no updates from Bakkt.

English

English

@DeepVaue_Adv $BKKT i want to be there for the move - need to see some meat on the bone. downloaded the app. couldnt get it to work. stalled at KYC. needs some seasoning...

English

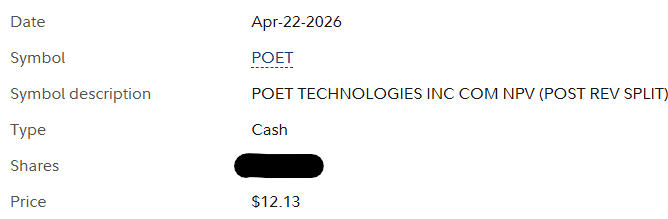

WHERE IS SERENITY????? $POET

McFly@ilzmcfly

AI supply chain mapping wont help you predict human stupidity from the CEO $POET down 40%, retail misled by they/them the pumper... $MRVL Cancels all contracts. The same thing will happen with many other companies they/them likes... I can see the faults. $AXTI next

English

@dekruh @BitcoinAIGuy Yep… not sure why you would question it. It’s call profit taking and rotation.

English

@ericmmatheny It was fun and easy to root for him during his college career. (Coming from a major SEC alumni and fan)

English

This guy will remind us what a professional athlete role model should be.

He’s got a promising career ahead of him and will

Hopefully inspire a generation of young men.

English

@ericmmatheny Cooked. This guy is such an arrogant prick. I hope his wife files for divorce before Monday.

English

Whoa.

You don’t move past this.

His career is over. Never to be resurrected again.

Hell withdraw from the CA Governor’s race within a week. He’ll resign from Congress or risk expulsion shortly thereafter.

English

The one time I got the invite of a lifetime, to play Augusta National, it was only a few weeks before The Masters. On property was Rory, Shane Lowry, Tom Brady, Scottie, the Chairman, Jimmy Dunne and more … it was power-packed and I was dizzy with the visuals.

On the course, which I played twice on that trip, it exceeded expectations. The walk was a lot of things, but if I were to use one word, it’d be “glorious.” Or, “magnificent.” Something I wouldn’t normally use to describe a round of golf.

And to play it requires “precision.” Which, for any golfer, but especially an amateur, is what makes it so difficult. We are not precise like they are. And from the tips, playing hard and fast, it’s the demand for that extreme level of precision that even tests The Best. Lies are so tight. Edges are so clean. Slopes are so extreme. Speeds are unlike anything we’ve seen.

From the member’s tees, rattle-bottom, I can’t imagine breaking 100 on a day like today. I would set over-under at 105. And for context: My current Index is 7.1, I have decent length, struggle with iron play, streaky short game and I consider myself a good putter. That being said, there would be plenty of bets on the over. Rightfully so.

Every shot, from tee to green, and then on the greens, requires strategy and skill. It’s relentless. Right, left, up, down. Get out of position, you pay. Dearly. It beats you down with a southern genteel charm, leaving you humbled and, at times, embarrassed. And I left with so much more respect for what these guys do and how they do it. (And mind you, I had a lot of respect going in.) The scores they card?! Unfathomable.

This week in particular, buckle up. It’ll be defensive. Destructive. Demoralizing. More middle fingers and slammed clubs. A guess on winning score? It might just be -5.

English

@mikealfred Never know whether to take your posts seriously. Pick a lane. Serious investor and public stock board member or internet clown

English

In line at the bank and guy in front turns around, looks at me, and says “Mike Alfred”. He looks at me like I should know him but I don’t. He says “from X” and I say “okay yeah”. Shows me his phone. Screenshot of a $780,000 brokerage acct balance. He says “we should go soon” 🤣🚀

English

@kryptosopus Jeff Sprecher and ICE (owner of NYSE) and has been forward thinking in this space for years. Securitize is a great company (I am an investor there) but NYSE will likely have many partners in the tokenization space.

English

@WSJ Funny how NYSE didn't build this themselves. Securitize basically got hired to modernize someone else's house because the owner refused to pick up a hammer for ten years.

English

Exclusive: Securitize will become NYSE’s first digital transfer agent, allowing it to create shares for stocks and exchange-traded funds as digital tokens on a blockchain on.wsj.com/3Nyh8Pj

English

@modaegypt where exactly is that condition spelled out? "under the condition that Bakkt becomes the "unified global financial infrastructure platform" for ICE. ?

English

@WallStrOracle ICE agreed to vote its shares FOR the DTR acquisition, but only under the condition that Bakkt becomes the "unified global financial infrastructure platform" for ICE. they should also prove technically fit before the voting

English

$BKKT Why ICE gave up a 31.5% of BKKT to Naheta in exchange for DTR....Why the investor day announcements and contracts should come before the voting on the 24th....$BKKT

English

@SharkChart haha! thanks for posting this. I almost felt sorry for him, yesterday.

English

@ScottPresler you are a perfect example of how one person can make a difference... great job!

English

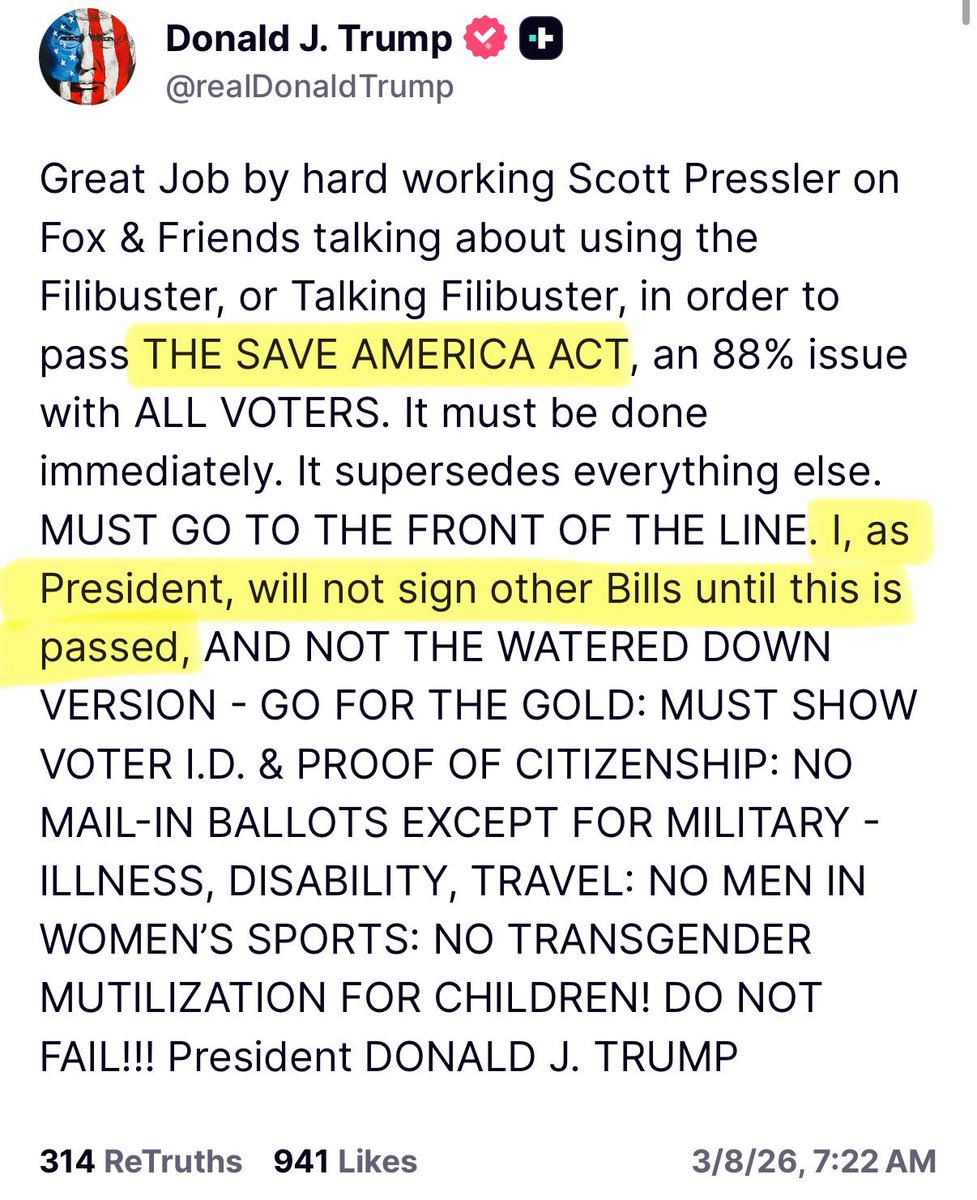

BREAKING

President Trump said he won’t sign other bills until the SAVE America Act is passed.

English

@MarshaBlackburn @boringcompany @elonmusk Would be nice to put all the bachelorette parties on an underground loop.

English

Last night, the Nashville Metro Council voted to oppose the Music City Loop, a private project that would improve infrastructure in Tennessee at no cost to taxpayers.

Woke bureaucrats should not condemn the @boringcompany simply because they don't like @elonmusk.

English

The fall of the Islamist Republic of Iran may be the biggest and most important geopolitical moment for Western values and prosperity since the fall of the Berlin Wall.

English

Oobit’s DTR Integration is a Strategic Win for Bakkt $BKKT

What makes the Oobit and DTR integration interesting is not that another wallet added an off-ramp. Wallets add features every week. What matters here is who controls the settlement layer and what that implies if it scales.

From the beginning, @Akshay_Naheta stated ambition for Bakkt has been to sit at the connective layer between digital asset infrastructure and the regulated financial system. Stablecoins have already proven that they can move value at global scale (>$30T annually by most estimates) with hundreds of billions clearing each month.

But moving value onchain and settling value inside bank accounts are not the same thing. Liquidity is one half of the equation. Regulated settlement is the other.

Distributed Technologies Research (DTR), which Bakkt has under a potential acquisition, is the infrastructure that addresses that second half. Oobit’s new wallet-to-bank capability runs on DTR’s routing engine. Under the hood, that engine handles FX conversion, liquidity management, compliance routing, and connectivity into domestic payment rails such as SEPA, ACH, SPEI, PIX, and InstaPay. In other words, it does the unglamorous but essential work of turning programmable dollars into regulated bank deposits.

The flow itself is simple.

1. A user holds stablecoins in self-custody inside the Oobit wallet

2. When they initiate a transfer, DTR converts crypto into a USD-equivalent stablecoin amount

3. That value moves into DTR’s settlement engine

4. DTR executes foreign exchange where required and routes the payout through the appropriate domestic rail (SEPA, ACH, SPEI, PIX, InstaPay)

5. Funds arrive in a local bank account as a standard deposit

The user never leaves the Oobit interface. There is no redirection to an exchange, no separate custodial transition, no visible intermediary.

That embedded, white-labeled architecture matters because in much of crypto, users are pushed out of wallets into third-party on- and off-ramps, introducing friction, compliance duplication, and abandonment risk. Here, onboarding, KYC, account creation, and settlement are integrated inside the Oobit wallet experience. The customer may not even know DTR is operating in the background. From a distribution standpoint, that is powerful.

Equally important is the use of named accounts on the on-ramp side. In Europe (EUR), the UK (GBP), and the United States (USD), users can move money directly from their bank accounts into the Oobit wallet through accounts held in their own names at DTR. Banks see transfers between individuals rather than transfers to a crypto exchange. That structural detail reduces the probability of blocking and reportedly drives transaction success rates >99%.

Combine the on-ramp in Europe with the off-ramp in Mexico and you have a full loop: euros enter from a regulated bank account, stablecoins move across blockchain rails, pesos exit into another regulated bank account. Each leg can generate economics. The feature introduces a corridor that previously didn’t exist.

From Bakkt’s perspective, the significance lies in the economics of how this gets orchestrated. While payments is a ~$1.8T global revenue pool, cross-border flows remain fragmented and inefficient. Correspondent banks, acquirers, card networks, and FX desks each take their share. Yes, stablecoins give you fast, global liquidity but they do not eliminate the need for compliance, FX, and domestic rail access. That orchestration layer is where DTR operates.

It’s a volume-based business model. Assume a settlement layer captures 50-100 bps of TVL. On $1 billion of annual flow, that’s $5-$10M of revenue. At $5 billion, it becomes $25-$50M. At $20 billion, the math scales quickly. The precise take rate will vary by corridor and competitive dynamics, but the elasticity is the point. Once compliance frameworks, liquidity pools, and rail integrations are built, incremental volume can carry improving marginal contribution.

Oobit reportedly serves tens of millions of users. Even modest adoption of on- and off-ramp flows across that base can generate meaningful throughput. They provide the distribution, and DTR monetizes the settlement. If and when DTR formally sits under Bakkt’s umbrella, those settlement economics fully accrue to Bakkt.

The broader implication is that the bottleneck in crypto has not been transaction volume, it’s been conversion into the regulated banking system. Stablecoins already move value 24/7. What they’ve lacked is frictionless integration with domestic payment rails at scale.

If DTR becomes a preferred routing engine across multiple wallet and fintech partners, Bakkt would not need to win the consumer wallet war. It would need to win the infrastructure layer and it can do that by embedding its routing infrastructure across multiple distribution surfaces. Each additional integration compounds throughput without incremental customer acquisition cost.

If that architecture can scale, it doesn’t stop at remittances. By operating at the convergence between two monetary systems, the global, onchain dollar economy and, the regulated domestic banking system, Bakkt can position itself to eliminate the friction that’s historically made the interoperability been slow, expensive, and opaque.

If the handoff between the two can become seamless, predictable, and embedded, the implications can extend beyond remittances to payroll, SME treasury, and cross-border commerce. And, once settlement is trusted, adjacent products follow naturally: yield, credit, treasury optimization, programmable commerce, etc.

There’s a massive opportunity and TAM for any business that can operate the conversion point between digital liquidity and bank money. The onchain dollar economy is already here. Winners will be companies that make those two systems interoperate at scale. Own that conversion layer and you own the doorway between both. That’s what DTR was built to do and that’s what Oobit is integrating.

English