@TMTLongShort Why not take tirze which is approved and tested, while reta is newer and not fully tested?

English

Vlad Andrei

2.3K posts

@vladsiminel

Decentralized Finance, Partner at Albaron Ventures -- Tweets are not financial advice

Fantastic explanation by Chris Whalen of how institutions use insurance companies to gain access to private credit & how intertwined the systemic risk is. $OWL and other lenders are borrowing from the government Federal Home Loan Bank to fund these crazy data center loans.

Do I hear a cockroach? A shadowy private credit firm is suddenly blocking investors from withdrawing their money. The Trump Administration needs to wake up. Stop pushing these risky investments into Americans’ retirement accounts.

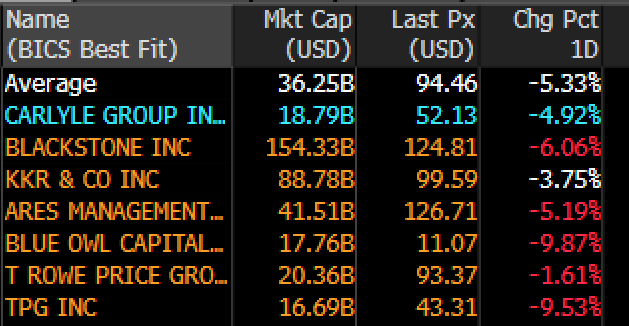

Blue Owl just announced the sale of $1.4 billion of private credit loans (including, gasp, software loans!) to a group of institutional investors at 99.8% of par value. Meanwhile, its BDC prices imply its loan book at 73-78% of par value. $OBDC $OTF

Agent Skills are everywhere - Claude Code, Gemini CLI, Codex all support them. But do they actually work? 105 domain experts from Stanford, CMU, Berkeley, Oxford, Amazon, ByteDance & more built SkillsBench to find that out. 86 tasks. 11 domains. 7,308 trajectories. 🧵👇

Google has revealed that "commercially motivated" actors attempted to clone @GeminiApp by bombarding it with over 100,000 prompts. This "model extraction" attack aimed to steal the AI’s proprietary logic and reasoning capabilities, particularly in non-English languages, to train a cheaper, unauthorized copycat model. The attackers systematically mapped Gemini’s response patterns to create a synthetic dataset for fine-tuning smaller, open-source models. Google’s Threat Intelligence Group detected the coordinated activity and blocked it, labeling the incident a direct attempt at intellectual property theft. Beyond commercial cloning, Google’s report noted a rise in state-backed threats. Groups from Russia, China, Iran, and North Korea are increasingly using AI to refine phishing campaigns, perform reconnaissance, and assist in writing code for malware. Source: Ars Technica

I underestimated how much exposure Fannie and Freddie ("F2") have to crypto, not on balance sheet, but in their shareholder bases. Run a correlation between F2 and bitcoin and you will see what I mean. Forced liquidations and margin calls in crypto are leading to F2 share sales in the market. We don't own bitcoin, but clearly in the short term, we own a stock market proxy for bitcoin. In the short term, the technicals can overweigh the fundamentals. F2 are a case study of that phenomenon.