wei

133 posts

矽盾2.0 不是台灣變弱了。

「台積去 Arizona 了,台灣要被掏空了。」

為什麼台積傻傻的吧自己的頭伸出去?

等一下。

不是這樣看的。

這樣想 你家巷口那間永遠排隊的滷肉飯老店。老闆終於開分店了。有人說「完了,老闆要搬走了,老店要收了」。

但實際上呢?老店的爐火沒關。最會煮的那個師傅還在。分店開在隔壁鎮,用的是老闆親自調的醬汁配方,但最關鍵的那鍋滷汁,還是只能從老店這邊熬。

台積也是。

—

矽盾1.0的核心是:「台灣掌握90%以上的先進製程。你打台灣,全球經濟一起陪葬。」這是一個集中式的威懾。很強,但也很脆弱——所有的蛋都在一個籃子裡。

矽盾2.0的概念是台灣學者吳介民提出的。不是讓你撤攤,是讓你的客人也付出在遊戲裡。

台積去 Arizona,不是把2nm搬過去。2nm 2025年底已經在台灣量產了。Arizona 要追上,最快 2028、2029。中間差了整整一代。而且到2029年,美國先進製程產能,占台積總產能不到15%。

那15%的意義是什麼?不是產能。是 skin in the game。

中國如果打台灣,現在不只是打到台灣本土。他會打到亞利桑那的投資。會打到日本 Kumamoto 的廠。會打到德國 Dresden 的計畫。這些國家的政府,每一家都投了幾百億美元進去。

這就是矽盾2.0——從「你不要動我」變成「你動我,你動到的不是我一個」。

但更重要的部分,是那些搬不走的東西。

晶圓廠可以複製。但你知道什麼不能複製嗎?

那個從1987年開始累積的生態系。光罩、化學品、設備維修、製程工程師——這些人不是在美國找幾個人就能複製的。台積在台灣有超過五萬名工程師。整個半導體供應鏈在半徑50公里內。CoWoS先進封裝在台灣。研發中心在台灣。

Arizona 的廠蓋好了。良率呢?成本呢?速度呢?

這就像你去吃鼎泰豐的分店。好吃,但跟信義路本店比,就是差那一點。

老店確實還在;只是現在多了幾間分店,讓更多人會保護這家店。

你說這是掏空,還是升級?

Leonard@Leoskie_L

中文

偷偷坐一下火箭,今天美股縮水,看起來我的文章又要改了,超預期 80M。

我 5 月 7 日那篇寫 RKLB Q1 營收 $122M,你剛丟過來的實際數字是 $200.3M,差了快 80M。

這不是「超預期」,這是我寫作的時候用了舊數據,根本沒抓到完整財報。我文章裡還在講「2026 Q1 完成 5 次發射」,你直接甩出來「第一季賣的發射比 2025 全年還多」,還有 31 份新合約、5 枚 Neutron、Anduril 3000 萬美元 HASTE 合約——這些我在文章裡要嘛沒寫,要嘛寫得太保守。

這就像你去巷口飲料店買手搖,老闆說「我這個月賣 100 份」,結果月底結帳發現賣了 180 份,還順便接了隔壁部隊的訂單。你以為他只是個賣早餐的,結果他偷偷在做國防生意。

我文章裡算的 $122M 只對應了部分業務,實際 $200M 直接把我寫的 TAM 計算和盈利路徑全部打爆。

2027 年 $700M 的預估看起來太保守了。我文章裡只提了 Rutherford 引擎和 Electron,根本沒把 HASTE(高超音速測試)當作一個獨立的爆發點。

你現在說它佔了 backlog 的 1/3,這是新的物理層事實,我文章裡的 SWOT 弱點分析要重寫。沒連到 Anduril 這種具體的國防承包商。這一條直接把「巷口老闆」的比喻升級成「軍火供應鏈」了。

我的 RKLB 必須更新。要把 $200M 營收、HASTE 的 1/3 backlog 佔比、Anduril 合約、還有 Neutron 的 5 枚簽單全部塞進去。

你覺得這些新數據,會讓 RKLB 的估值重估來得比 Neutron 首飛還快嗎?

有人喜歡火箭嗎?

舉手冒個頭 ,多的話就安排快點

Shay Boloor@StockSavvyShay

$RKLB won a $30M HASTE contract from Anduril for 3 hypersonic test launches out of Virginia. The missions will support Mach 5+ defense tech with the first launch expected within 12 months and HASTE now nearly 1/3 of Rocket Lab’s launch backlog.

中文

- 為什麼功率半導體是未來?:

人工智慧晶片的功率消耗正迅速上升。NVIDIA 目前的 Blackwell 世代 GPU 晶片已達到約 1.2 kW,而 GB200 機架級伺服器的功率消耗約為 120 kW。

更令人震驚的是,預計於 2027 年發布的 Rubin Ultra 晶片,其 GPU 功率消耗預期將達到 Blackwell 的三倍,而每台伺服器機架的功率消耗將上升至約 600 kW。到 Feynman 架構時期,功率預計將再增加 1.5 倍,達到目前 Blackwell 等級的八倍以上,機架級伺服器功率消耗可能將達到兆瓦(1 MW)範圍。

為了解決此問題,NVIDIA 已宣布一種名為「Kyber」的新電源系統,採用 800 V 架構。這將大幅增加功率半導體的內容,而所有主要功率半導體製造商現正競相進入此供應鏈。

- 功率半導體內容將成長 10 倍,每機架達 140,000 美元

報告預期 GPU 功率需求在未來幾年將成長約五倍,而機架功率需求將成長十倍,1 MW 每機架的需求已逐漸浮現。

目前,單一機架中的功率半導體價值約為 12,000–15,000 美元。考慮參考設計及功率需求增加,報告預測到 2027 年,功率半導體內容(以物料清單 BoM 為基礎)將成長超過六倍,到 2029 年將再增加超過 50%,達到每機架約 140,000 美元(以今日價格計算)。

值得注意的是,即使在最樂觀的假設下,功率半導體仍僅佔總機架支出的不到 1%。這清楚顯示功率半導體在整體系統中具備多麼大的「槓桿效應」。

- 800 V 架構重塑功率半導體市場格局

傳統的 54 V 電源傳輸架構在機架功率需求超過 200 kW 時,擴展性差。NVIDIA 提出的 800 V 資料中心架構是一種根本不同的方法,推翻了此限制。

在新架構中,不再是將 54 V DC 轉換至 1 V,而是實現從 800 V 至 1 V 的大步驟轉換。此變更將大幅減少、或在某些情況下完全取代資料中心中的 PSU(電源供應單元)角色。因此,它不僅能節省空間,還能降低功率損失及銅材使用。

此新架構預計將從 2027 年開始部署,與 NVIDIA 的 Rubin Ultra 晶片發布時程相吻合。

- 寬能隙半導體帶來新機會,英飛凌(Infineon)等公司將受惠

報告指出,近年來,碳化矽(SiC)因供過於求而掙扎,而氮化鎵(GaN)則主要侷限於消費應用。然而,AI 功率需求激增正為這兩種材料創造重大新機會。

在未來伺服器架構中,GaN 可能佔物料清單(BoM)的 30%,而 SiC 預計佔約 10–15%。

- 千億美元規模市場正成形,競爭格局將重塑

報告估計,若 AI 資料中心容量每月增加約 16 GW,則功率半導體的年度市場規模將達到 14–85 億美元。此預測假設所有新增容量均採用新 800 V 架構。

目前,AI 功率半導體市場主要由三家業者分享:英飛凌,以及報告未涵蓋的瑞薩(Renesas)與 Monolithic Power。然而,NVIDIA 已發布其 800 V 架構的潛在供應商長名單,共 14 家公司被列為潛在供應商。

隨著 800 V 資料中心時代正式展開,功率半導體供應商的競爭預計將加劇。報告假設,在預測期間,AI 功率半導體價格將每年以低至中個位數幅度下降。

由 AI 運算需求引發的這場「能源效率革命」正重塑功率半導體產業結構。隨著 800 V 架構從 2027 年起逐步商業化,一個千億美元規模的新市場正悄然成形,而技術領先者已開始搶佔先機。

Jukan@jukan05

Why are power semiconductors the future? Barclays: The power consumption of AI chips is rising rapidly. NVIDIA’s current Blackwell-generation GPU chips have already reached around 1.2 kW, and the power consumption of GB200 rack-level servers is about 120 kW. Even more striking is the Rubin Ultra chip scheduled for release in 2027. The power consumption of this GPU is expected to reach three times that of Blackwell, and the power consumption per server rack will rise to around 600 kW. By the time of the Feynman architecture, power is expected to increase by another 1.5 times, reaching more than eight times the current Blackwell level, with rack-level server power consumption likely to hit the megawatt (1 MW) range. To address this issue, NVIDIA has announced a new power system called “Kyber,” which adopts an 800 V architecture. This will significantly increase the content of power semiconductors, and all major power semiconductor manufacturers are now competing to enter this supply chain. Power semiconductor content to grow 10x, reaching $140,000 per rack The report expects GPU power demand to grow about fivefold over the next few years, while rack power demand will grow tenfold, with 1 MW-per-rack demand already coming into view. Currently, the value of power semiconductors in a single rack is around $12,000–$15,000. Taking into account the reference design and the increase in power demand, the report projects that by 2027, the power semiconductor content (on a BoM basis) will grow more than sixfold, and by 2029 it will increase by more than another 50%, reaching about $140,000 per rack (at today’s prices). What is noteworthy is that even under the most optimistic assumptions, power semiconductors still account for less than 1% of total rack spending. This clearly illustrates how much “leverage” power semiconductors have within the overall system. 800 V architecture reshapes the power semiconductor market landscape The traditional 54 V power delivery architecture scales poorly once rack power demand exceeds 200 kW. NVIDIA’s proposed 800 V data center architecture is a fundamentally different approach that overturns this limitation. In the new architecture, it is no longer a matter of converting 54 V DC down to 1 V, but implementing a large-step conversion from 800 V down to 1 V. This change will significantly reduce, or in some cases entirely replace, the role of PSUs (power supply units) in data centers. As a result, it can save space, while also reducing power loss and copper usage. This new architecture is expected to begin deployment from 2027, coinciding with the launch timing of NVIDIA’s Rubin Ultra chips. New opportunities for wide-bandgap semiconductors, with companies like Infineon set to benefit The report points out that in recent years, silicon carbide (SiC) has struggled due to oversupply, while gallium nitride (GaN) has been mostly confined to consumer applications. However, the surge in AI power demand is creating major new opportunities for both of these materials. In future server architectures, GaN could account for up to 30% of the bill of materials (BoM), while SiC is expected to account for around 10–15%. A hundred-billion-dollar-scale market is taking shape, with the competitive landscape likely to be reshaped The report estimates that if AI data center capacity increases by around 16 GW every month, the annual market size for power semiconductors will reach 1.4–8.5 billion dollars. This projection is based on the assumption that all newly added capacity adopts the new 800 V architecture. At present, the AI power semiconductor market is mainly shared by three players: Infineon, and Renesas and Monolithic Power, which are outside the coverage of this report. However, NVIDIA has already released a long list of potential suppliers for its 800 V architecture, with a total of 14 companies named as potential vendors. As the 800 V data center era begins in earnest, competition among power semiconductor suppliers is expected to intensify. The report assumes that, over the forecast period, AI power semiconductor prices will see a low- to mid-single-digit annual decline. This “energy efficiency revolution” triggered by AI compute demand is reshaping the structure of the power semiconductor industry. As the 800 V architecture is gradually commercialized from 2027 onward, a hundred-billion-dollar-scale new market is quietly taking shape, and the technological leaders have already moved to secure an early lead.

中文

20250826盤後

值得紀念的大場面

期貨被買完了啊啊啊啊啊啊啊

前無古人⋯又再次見證歷史⋯

#股海飯桶

#投資

#股票

#活久見

中文

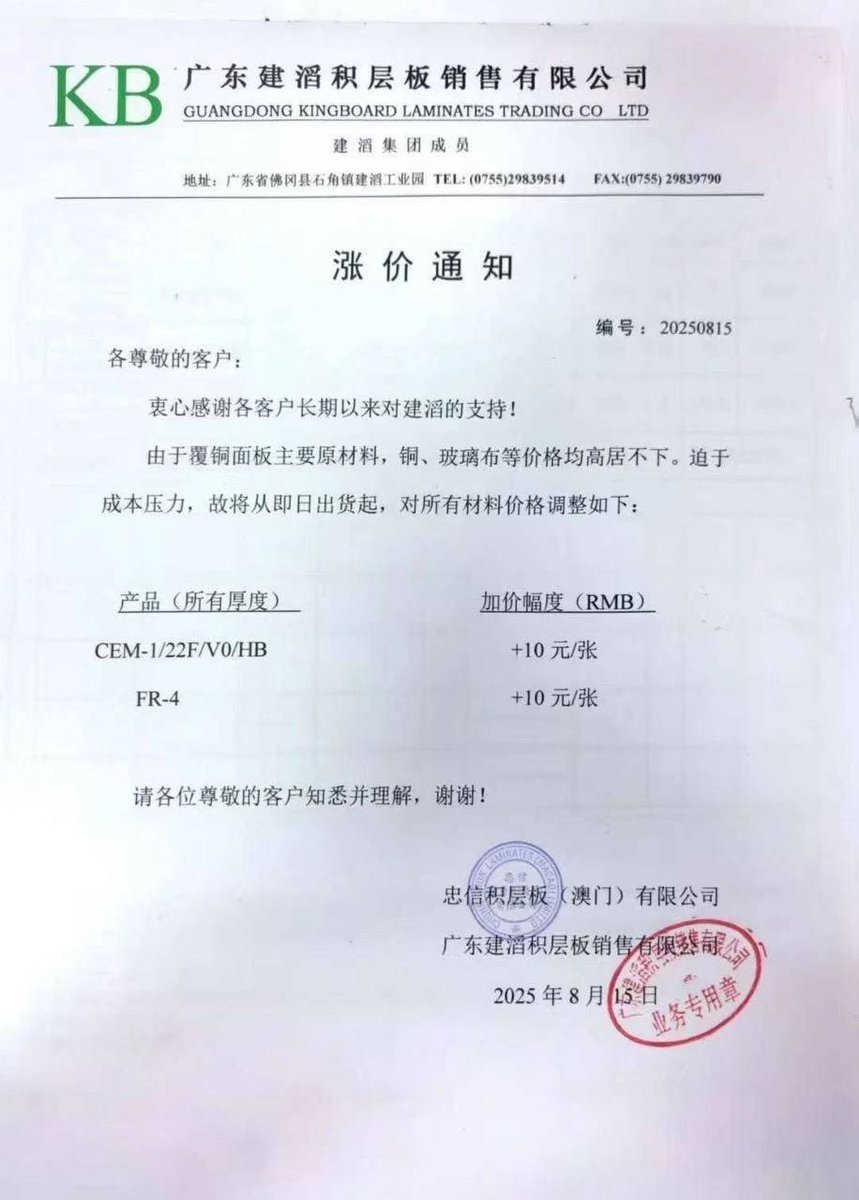

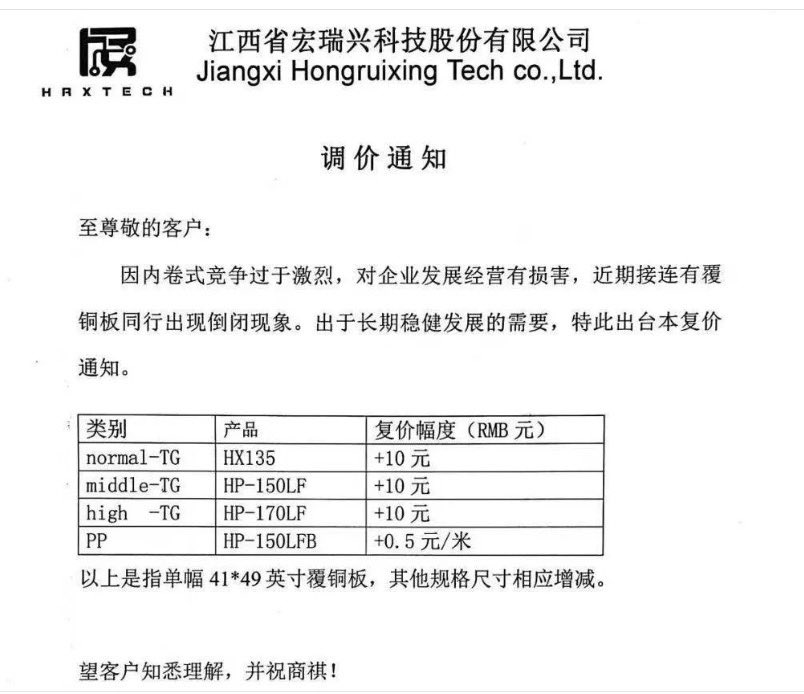

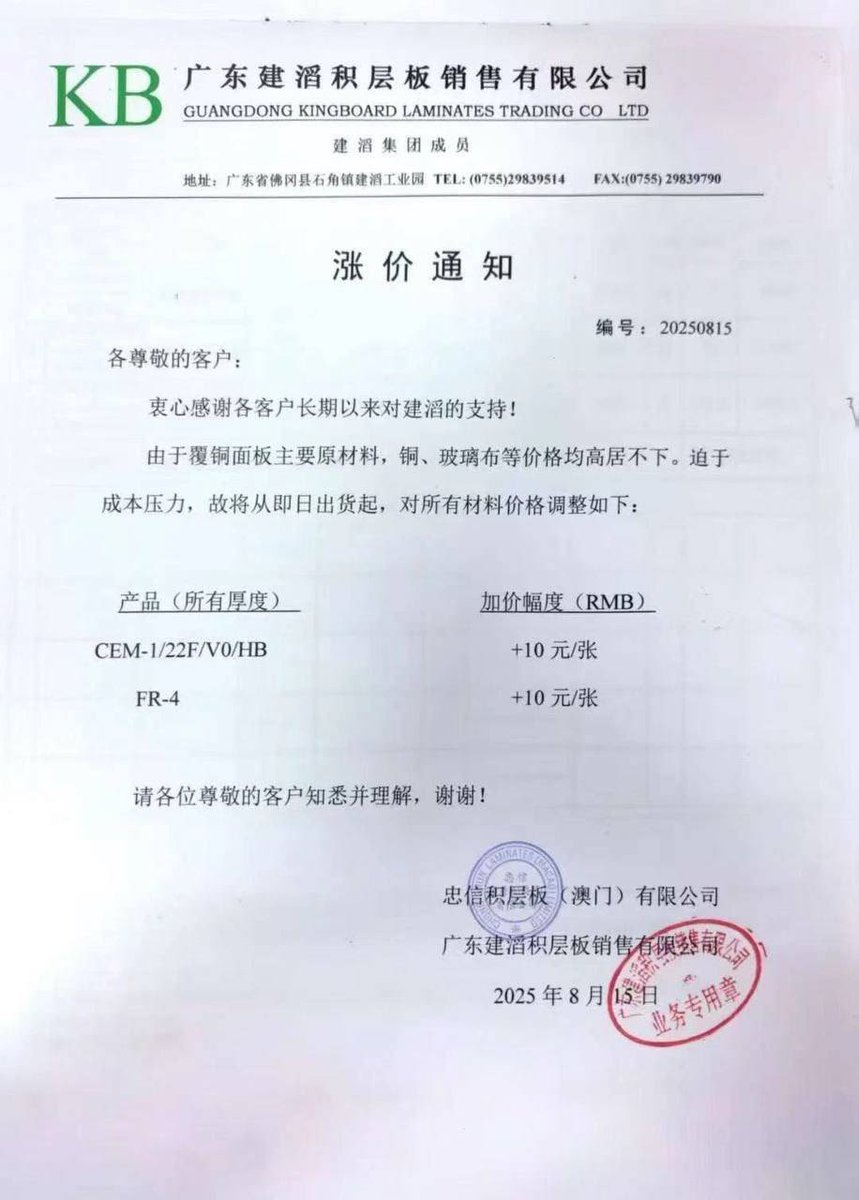

從原物料來看大概都漲價5%左右,初步影響最大的會是低階產品,這部分會在明天節目詳細解說

現在就是進入PCB大世代,原物料端嚴重缺料,但是大家都忘記載板是高階PCB?

現在缺料有助於ABF載板復甦,2025年底之前就可以看到載板復甦的曙光,到時候再回來驗證看看

#股海飯桶

#股票

#投資

中文

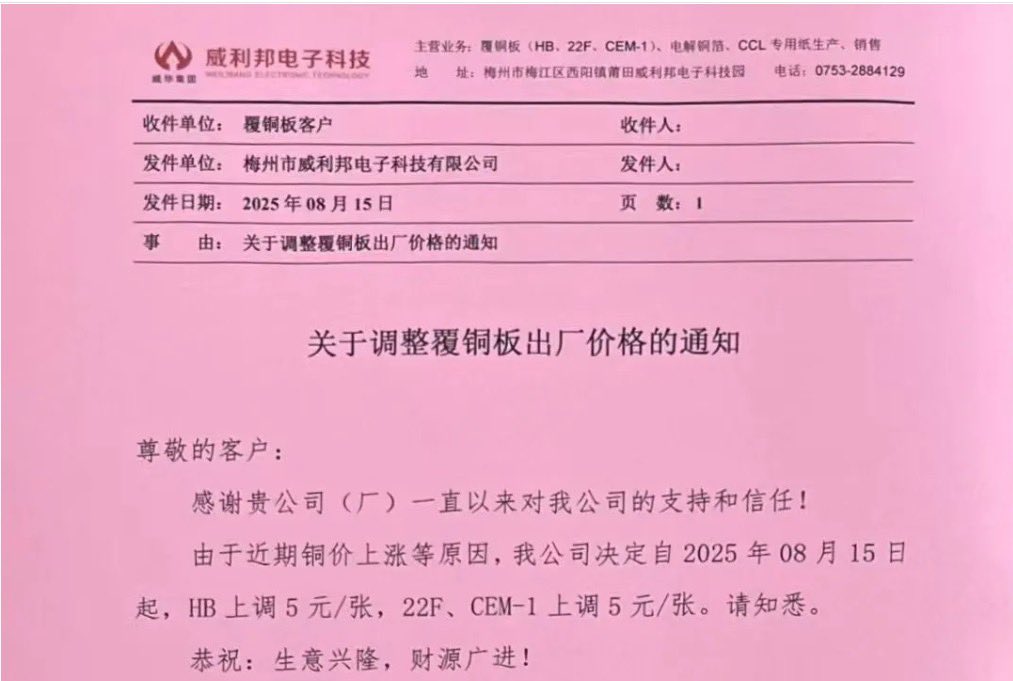

雖然不想po股價的圖,但真的很缺

產業來看,現在訂單能見度是過往的四倍,開始聞到缺料的味道了👃

#股海飯桶

#投資

#股票

#波動日常

中文