Josh Hunt@iAmJoshHunt

There are two numbers that should be sitting on every UK policymaker's desk this year. They are not.

The first is £9.18 trillion. The total value of UK housing stock.

The second is 70%. The share of UK workers in occupations the IMF classifies as exposed to AI. Higher than the US. Higher than the advanced-economy average.

Both numbers are real. Both come from serious published research. Neither is talking to the other.

Start with what UK housing actually is. Not bricks. Not land. Not planning permission. At the margin, UK housing is priced by what the next buyer can borrow. Mortgages clear at 4 to 4.5 times salary. Which means housing is a leveraged bet on British wages.

Now look at what those wages are.

81% of UK GDP is services. 83% of UK employment is services. Law. Finance. Consulting. Admin. Media. Tech. Middle management. These aren't side categories. They are the British economy.

They are also the roles with the highest AI exposure.

Goldman Sachs ranks them at the top: legal, financial analysis, operations, content production. The IMF puts 70% of UK workers in AI-exposed occupations, against around 60% in the US.

Why is the UK so exposed? Because we deindustrialised faster and further than any G7 peer, and replaced factories with knowledge work. The UK has seen the steepest manufacturing decline of any G7 economy since 1970. Every policy decision for forty years pushed labour into exactly the categories now in the crosshairs.

Then we concentrated it geographically.

London and the South East hold over 40% of UK housing value on just 26% of the housing stock. Same regions. Same workers. Same wages. Same exposure. The financial concentration mirrors the labour concentration almost perfectly.

Then we leveraged it.

UK household debt: around £2 trillion. Of which mortgages: over £1.6 trillion. Debt-to-income ratio: 117.5%. Lloyds alone has a £317 billion mortgage book.

The British banking system is a direct bet on services wages staying intact.

Now run the scenario.

If AI compresses services wages 10% over a decade, it is not a 10% fall in house prices. It's larger, and it's at the margin, because leveraged buyers drop out first and the comparables reset downward. That's how housing markets actually clear.

And the UK has no hedge.

The US has manufacturing reshoring, CHIPS Act money, energy abundance, resource extraction. Blue-collar wages rising as white-collar gets squeezed. The UK has none of it. We deindustrialised, layered the economy onto services, and financed £9 trillion of housing against wages that are now the most AI-exposed in the G7.

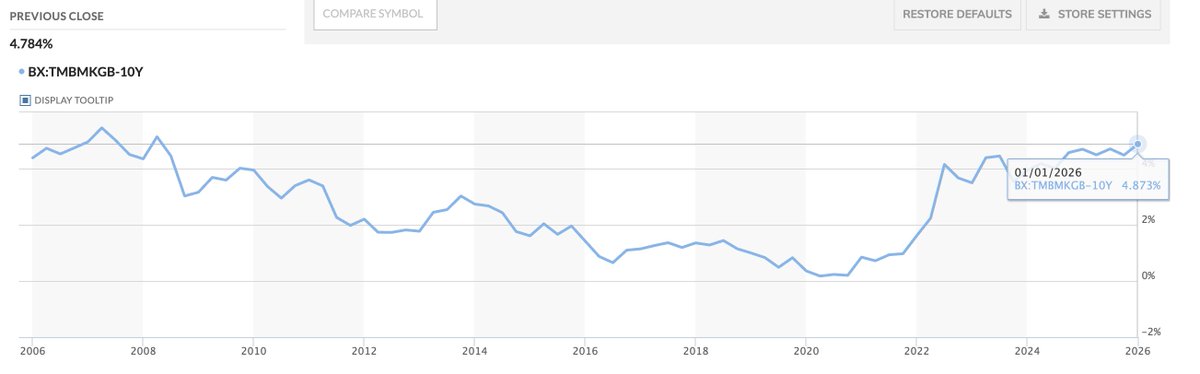

The rebuttal is that AI boosts productivity. The OECD expects UK productivity growth of 0.4 to 1.2 percentage points a year from AI. Second only to the US in the G7.

But mortgages don't clear on aggregates. They clear on individual incomes.

And the aggregate hides who captures the gains. The IMF's own recent research finds AI-era wage gains concentrating at the high-skill and low-skill ends of the labour market. Middle-skilled workers don't share in them proportionately.

Middle-skilled knowledge workers are the exact population whose mortgages clear the UK housing market.

The blast radius goes well beyond house prices.

Buy-to-let yields break. Pension funds' bank equity revalues. The council tax base erodes. Treasury receipts soften. Bank capital gets stress-tested against a shock no model has priced.

Every major UK asset class is, in some form, long services wages.

And yet the silence is total.

Politicians can't say it. The median voter is a homeowner. Banks can't say it. Capital requirements. Pension trustees can't say it. Members' retirements depend on the number. The Treasury can't say it. Its own fiscal projections assume rising property-linked receipts forever.

The silence is structural, not accidental.

Britain didn't just bet the economy on services. We bet the balance sheet of every household on services wages surviving the most disruptive labour technology in a century.

Nobody chose that trade explicitly. But every mortgage written in the last twenty years locked it in.

The numbers in this post aren't mine. They come from the IMF, OECD, ONS, Savills, the Bank of England, NIESR, and the UK government's own January 2026 AI labour market assessment.

Most came from Whitehall.

Nobody in Whitehall is connecting them.