Sabitlenmiş Tweet

Here is my WhatsApp group where all members discuss SME stocks.

Anyone can join👍

Link👇

chat.whatsapp.com/FkbV7bui0hI433…

English

Investor Yash

621 posts

@yashsoni____

Long term investor. Talks undervalued and growth SME & micro cap companies. Target 🎯1 crore portfolio by 2027.

Supreme Power Equipment H1'25 con-call key highlights: Potential candidate for 3x in 3 years? at 40% CAGR FY27 onwards? - FY26 Topline Guidance: The initial target was around Rs. 200 crores. Due to the late commissioning of the new plant, management estimates the final number might be closer to 180-190 crores - Capacity Expansion: The plant is planned to be fully operational by December 2025, with production scheduled to begin from January 2026 + New Product Capability: The facility will enable the manufacture of transformers up to 160 MVA at full capacity. Management plans for Phase 2 to potentially go up to 315 MVA + Full capacity utilization, leading to Rs. 500-600 crores in revenue, is expected to be achieved over the next 2 to 3 years (FY28/29), implying 40% CAGR ^ Note:- New Capacity Approvals: While commercial production for smaller capacity transformers (< 50 MVA) can start in Jan'26, gaining approval from major buyers (like PGCIL) for higher capacity transformers requires a longer process involving vendor approval, type testing, prototype testing, and consent to operate, which will scale gradually - Margin: Although focusing on higher MVA transformers (which usually offer better margins) will increase revenue, the associated overheads (especially talent acquisition for extra high voltage work) will absorb the increased margin potential - Geographic Expansion: ◦ Orders totaling Rs. 10.02 crores in Karnataka (20 MVA, 66 KV and 110 KV class). ◦ Order worth Rs. 19.82 crores from a leading EPC client in Telangana, marking an important expansion of geographic reach in South India - Execution Timeline and NLC Order • General Execution: Management expects 50% to 60% of the current Rs. 235 crores order book to be executed within this financial year (FY26), with the remainder moving to the next year. • NLC Order (Rs. 60 Cr): Supply has started. Manufacturing is almost complete, but some units require prototype type testing. Once testing is successfully completed, continuous sales will follow. Management believes all transformers for this order will be dispatched within about 1.5 months, contributing significantly to H2 numbers - Operational Focus and Expansion • Product Mix Focus: The strategic shift is towards larger power transformers (above 25 MVA, up to 160 MVA) where competition is less severe than in the smaller distribution transformer segment. • Government/Private Balance: The long-term strategy is to cap exposure to government tenders at less than 50%, ensuring 50% of orders come from the private sector. • Geographic Reach: SPEL is actively expanding its geographical presence beyond its traditional South Indian base, having secured approvals and orders in Telangana and Karnataka. • Export: Discussions are underway regarding export opportunities, with specific interest shown from UK - Receivable Cycle: The current receivable cycle is between 85 to 100 days #microcap #investing #stockmarket #supremepower #transformers

ORIANA Power #OrianaPower #Oriana Class executor FY25 PAT more than FY23 Revenue FY23 revenue at 135cr FY25 PAT at 159cr Guidance for FY26: 2000-2500cr revenue with similar OPM

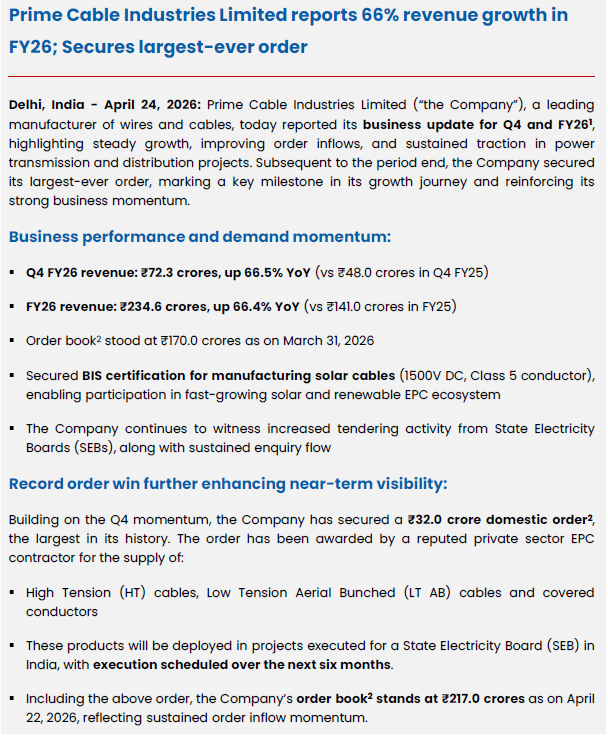

Cable sector is heating up and showing strong aggressive momentum 🔥🔥🔥 Two good SME companies to study and track from this space are: 1. JD Cables 2. Prime Cable Industries What their management has shared in the recent Bharat Connect Conference 👇

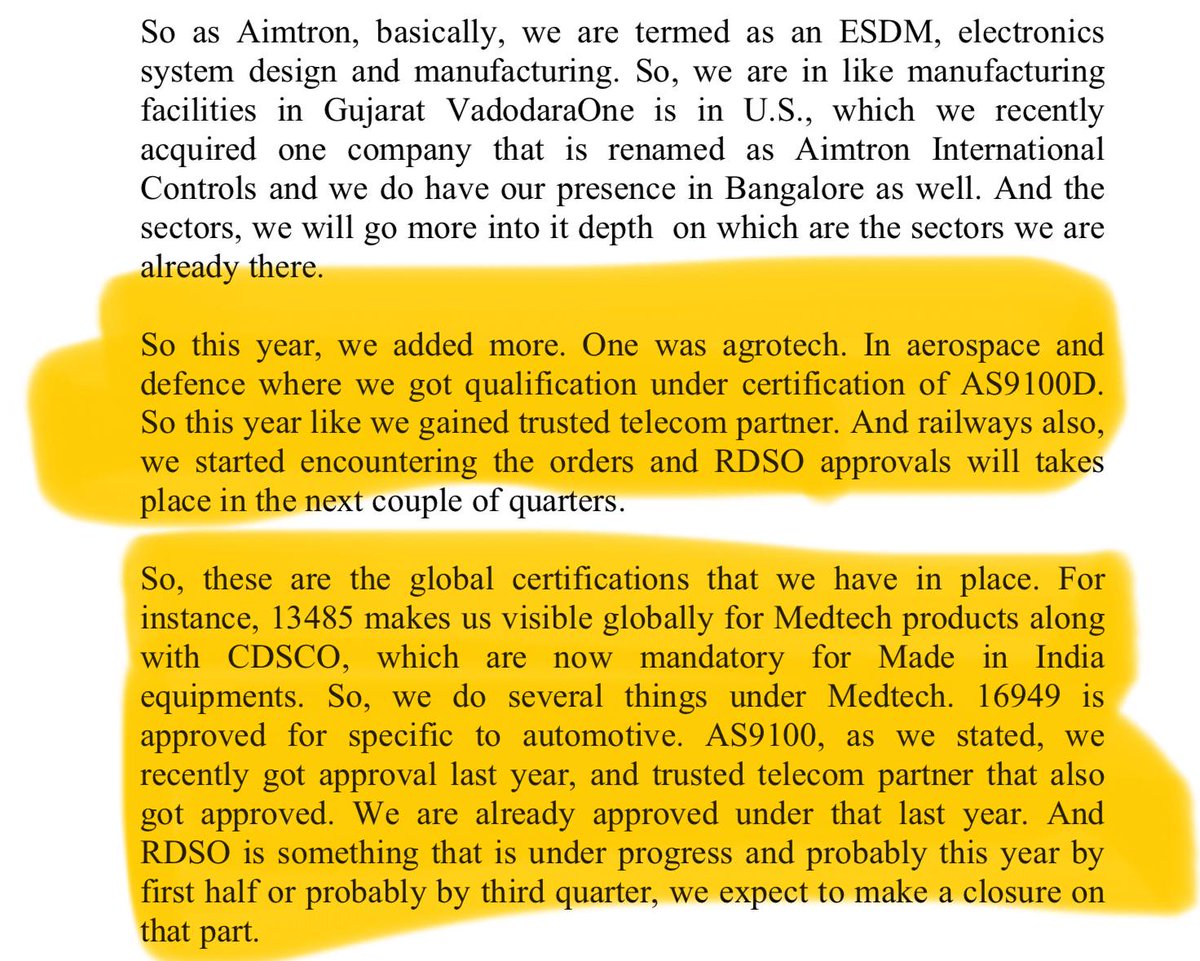

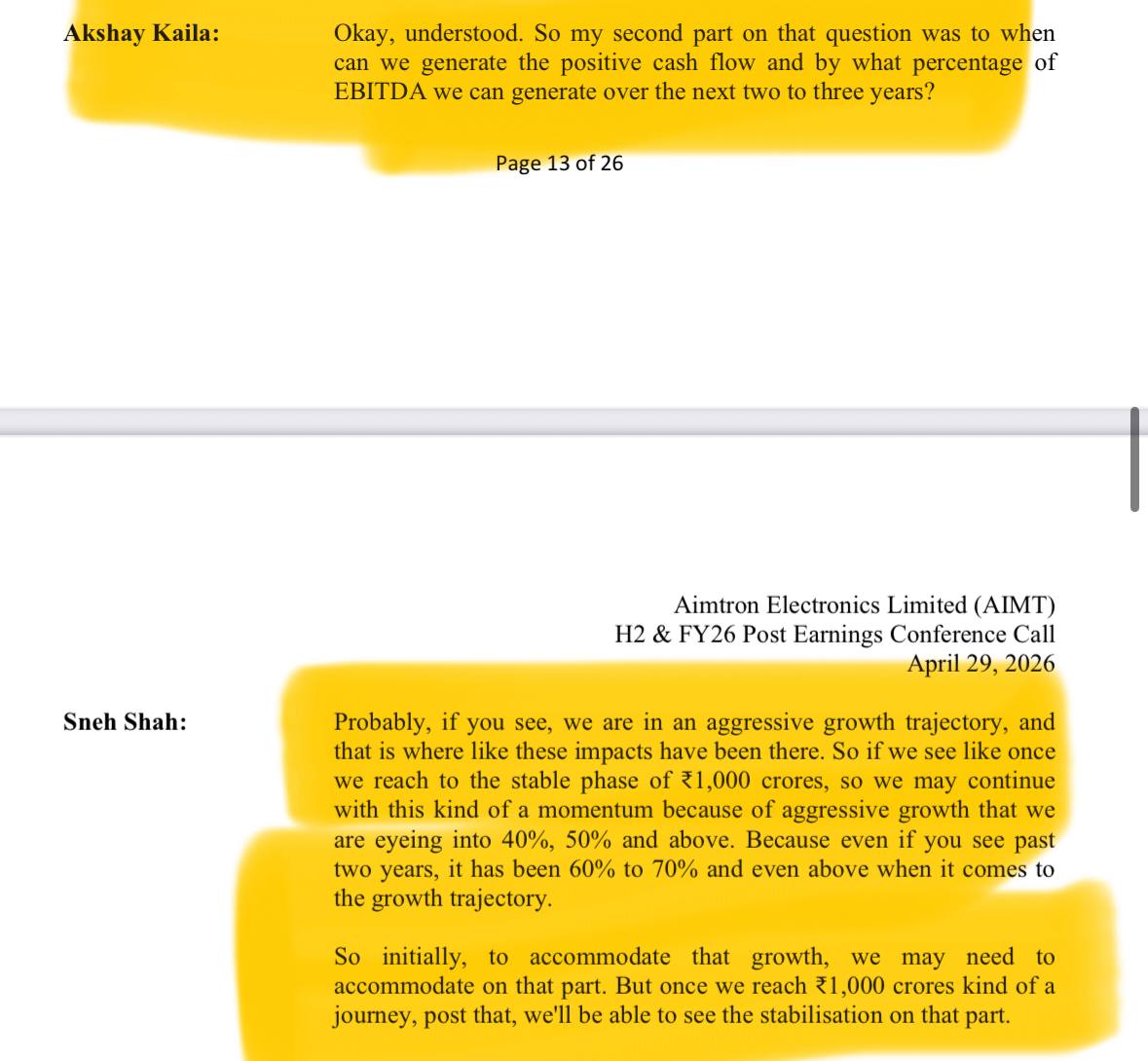

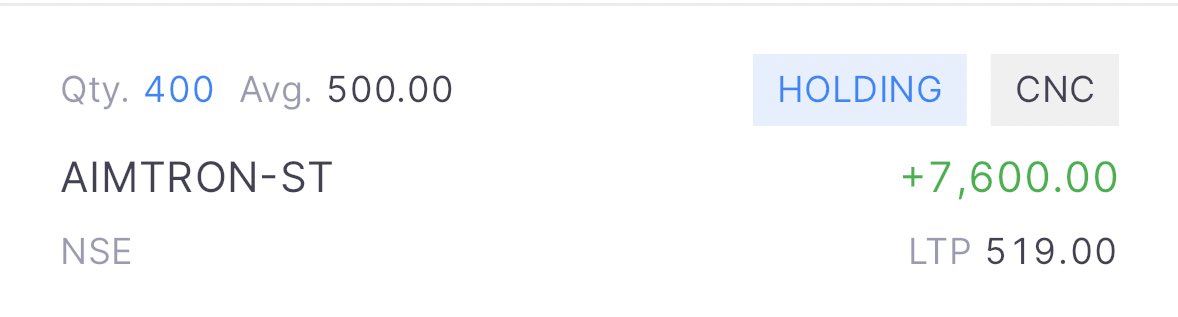

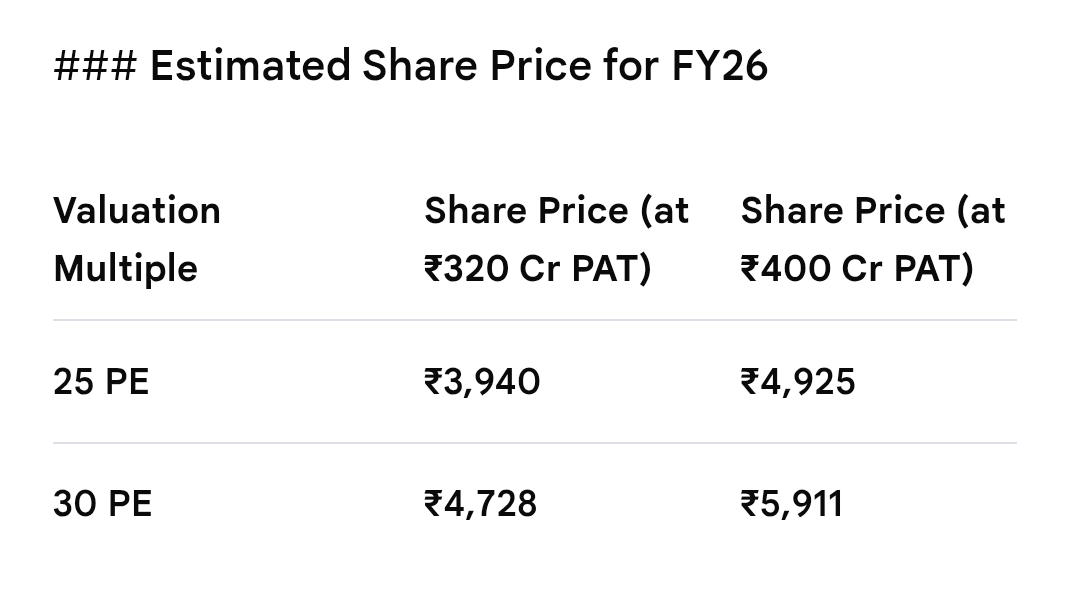

One more SME added today 👌#AimtronElectronics #aimtron Management given 35-40% CAGR guidance.🚀 Good results posted yesterday.💯

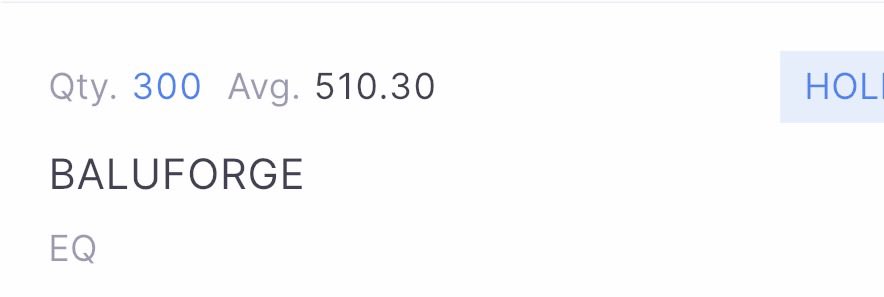

Noise VS Reality 🧐🧐🧐 Good recovery Balu forge limited #BFL

NEETU YOSHI - 👉FY25 ~ Revenue: ₹71cr 👉FY28 ~ Revenue Target: ₹380 Cr 👉Order Book ~ ₹150 Cr+ 👉If they achieve it’s 5x growth in 3 years🔥 👉Valuation ~ 19 PE Looks good at cmp(114). No recommendations. @Akash17971 @imujjwalsehgal @vishan_29 @DhawalDoshi5