昆山龙哥

349 posts

I’ve been grinding away trying to map out China’s recent crude plays, but after going through today's report, I have to hand it to OIES—they scripted the plumbing way better than me.

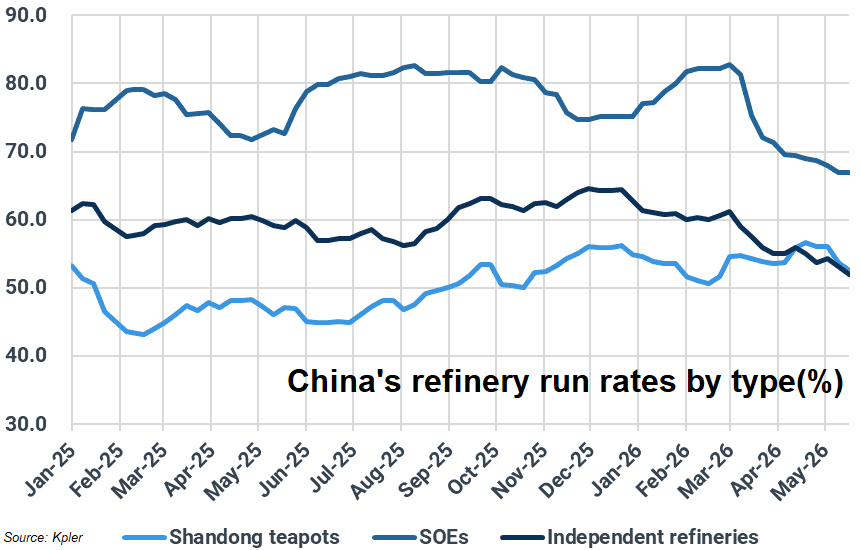

Here is my quick breakdown after running through their print, alongside the Chinese refinery throughput chart to help connect the dots.

-

Three months into the Hormuz crunch, and Beijing is completely blindsiding the market with its crude playbook. A heavyweight that easily sucked in 11mb/d over the last five years just saw its import prints plunge to 9.3mb/d in April. Now, the forward data says May and June seaborne arrivals are about to crater straight into the gutter at 6.5mb/d.

Instead of running its usual playbook of panic-dumping the SPR to backstop the market during a supply crisis, Beijing just completely cock-blocked refiners from touching the strategic vaults, only greenlighting commercial stock draws.

To make it worse, refiners aren't even willing to bleed their own commercial inventories, while state traders are acting like total penny-pinchers—happily flipping premium WAF cargoes back into the market and hoarding dirt-cheap Russian barrels instead.

This is a complete 180 from the 2021 power crunch, when Beijing panicked and ordered everyone to grab supply 'at any cost.' The heavyweights and policymakers in Beijing clearly think they can outmaneuver this supply shock and keep the economic damage locked down by playing a few smart, tactical micro-levers.

China’s true red line for freezing out imports is hardwired to the scale of their run cuts. If they try to copy-paste their five-year average throughput of 14.1mb/d, the exact moment seaborne arrivals drop below 9.2mb/d, they’re trapped—they either have to open the strategic taps wide or start chasing expensive market barrels. Instead, chopping runs by 5% down to a 13.4mb/d baseline is hands-down their most realistic, long-term survival play.

In this setup, if domestic crude extraction and pipeline taps keep humming, they can easily coast for a few months without taking a single economic hit, even with seaborne prints scraping a measly 7.9–8.5mb/d, because transportation fuels like gas and diesel will still be taken care of.

However cranking run cuts to a nuclear 10% scenario means they could survive without chasing a single market barrel even if seaborne flows dry up to 7.2mb/d—but they'd have to throw petrochemical feedstocks like naphtha and LPG under the bus just to keep gas and diesel flowing, a desperate move that runs on borrowed time and stalls out after a few months unless the whole economy is in a total tailspin.

To micromanage this whole run-rate circus, China's refining complex is pulling a highly responsive lever: the yield shift.

Beijing explicitly told state majors like Sinopec and PetroChina to ditch chemical feedstocks and prioritize flooding the market with gas and diesel, and these plants immediately saluted by shifting their product yields by several percentage points on a dime.

As a result, the real bloodbath isn't happening at the refining gate—it's completely decimating the downstream petrochemical chain. With Hormuz blocked, their seaborne naphtha inflows were already sliced in half, but a 5% run cut is about to bleed domestic naphtha and LPG supplies by tens of millions of tons a quarter, sending a compounding, fatal shock straight through the petchem feedstock backbone.

They are keeping wheels turning by guaranteeing gas and diesel, but the squeeze on industrial chemical feedstocks is completely running on borrowed time.

To paper over the massive raw material hole in the petchem chain, Beijing is shoving its massive 'Coal-to-Chemicals' complex into the spotlight, branding it as a strategic shield against volatile crude under the 15th Five-Year Plan.

Thanks to dirt-cheap, stable domestic coal, inland plants churning out olefins and methanol are running hot to boost volumes, but this quick fix hits a hard ceiling when it comes to replacing lost barrels at scale due to structural bottlenecks.

The core infrastructure is trapped deep in the northwestern sticks like Inner Mongolia, meaning slamming those products down to the massive manufacturing teeth on the southeastern coast comes with a punishing logistics and freight premium.

Most importantly, coal gasification routes physically cannot clone key aromatics or specialized LPG chemical chains—the feedstock deficit is mathematically locked in.

On top of that, the fact that Beijing is sitting on a massive 1.1-1.3 billion barrel pile without tapping it proves that institutional red tape is locking up the plumbing.

The 100 million barrels buried deep in dark underground rock caverns—completely invisible to satellites—are almost entirely SPR, requiring endless red tape like complex auctions and market disclosures, so Beijing is hoarding it as a nuclear option.

Even for the commercial barrels that are accessible, refiners are terrified to draw down because plotting out the repayment timeframe to replace that crude is a total mathematical nightmare in this chaotic macro environment.

Beijing is pulling off a highly calculated micromanagement script here: they are completely freezing out the inventory draw requests from state-owned heavyweights like Sinopec, who are nakedly exposed to global benchmarks and were the first to aggressively slash throughput.

Instead, they are using the Shandong teapots as a human shield—handing these independent refiners tax breaks and strict run-rate mandates because they have the flexibility to stomach toxic, illicit Iranian and Russian barrels to cushion the margin bleed.

Bottom line, this entire web of macro levers—starving imports, shifting yields, hunting for distressed barrels, and burning through coal-to-chem assets—will keep the lights on and protect the economic skeleton through the peak of summer, but only under that tight 5% run cut baseline that keeps seaborne arrivals pinned at roughly 8mb/d.

But with May and June seaborne prints already locked in at a subterranean 6.5mb/d, the expiration date on this makeshift band-aid play cannot stretch into autumn.

Short of letting their entire national refining infrastructure suffer a catastrophic meltdown, Beijing is running straight into a hard physical wall.

Before late summer wraps up, they will be forced to either open the strategic floodgates and dump their massive stockpiles or make a frantic U-turn right back into the international physical market, chasing heavy volumes aggressively at any price.

#oott #iran

English

最近,在富途、长桥、老虎被证监会罚款事件后,香港券商炒美股的合规成本已经非常高了,存量账户虽然还能用,但政策不确定性一直悬在那里,什么时候收紧、收紧到什么程度,没有人说得准。

我没事研究了一下汇丰Trade 25,发现用这个投资的成本其实相对来说是很低的,25 万港币以内,每月港币 25 元,0 股票佣金及 0 平台服务费,而且你只需要一个汇丰银行账户就可以投资港股和美股,也不用再去冒着合规风险开券商账户了。

先说结论:Trade25比较适合两类人:港股中频交易者,和美股小额定投党,发现优势主要来自这么几个地方。

第一个是港股的费用结构真的很干净。 在每月25万港币的额度内,每笔交易0佣金。每月固定的25港币月费,也只在当月有港股交易或者港股持仓的时候才收,当月没动过就不收。

第二个是美股小额交易的成本低。 上周买卖了一股VOO试水,买入零费用,卖出只收了0.01美元,是交易所的代收费。对比一下:长桥美股每笔最低1美元,盈透最低0.35美元,Trade25在小额交易上的成本优势,是数量级的差距。对于每次买一两股、慢慢定投的人来说,这个差距会随着交易频率不断叠加。

第三个是美股情况下月费暂时也不收。 如果你只交易美股、没有港股持仓,当月的25港币月费也不会触发。也就是说,纯美股定投的场景下,实际支出只有交易所代收费,几乎可以忽略不计。

第四个是股息没有代收费用。 美股持仓产生的股息,汇丰不额外收取代收费,这一点很多人没注意到,长期持仓的情况下会有实质性的差距。

第五个是资金安全的确定性。 汇丰是全球性银行,香港本地持牌经营,监管体系和互联网券商完全不同。在现在跨境券商政策持续收紧的背景下,这个底层稳定性的价值,越来越难被替代。

当然有得必有失,Trade25的短板也很明显:

1. 每月25万港币的额度买卖双边合并计算,超出后美股收费巨贵,最少18美元一笔;

2. 只支持盘中交易,没有盘前盘后;

3. 不支持碎股,最少1股起买;

4.软件功能比较基础,止盈止损单和期权都不支持。

大概就是这些了。

如果你是月交易额在25万港币以内、以定投为主、不需要复杂功能的普通投资者,Trade25目前来看是香港成本最低的选项之一,值得认真考虑。

投资有风险,入市需谨慎。

中文

这两天因为老虎富途的事情。大家都在推券商。

很多人都推了IBKR。

说实话。我觉得IBKR挺适合价值投资者的。

因为IBKR是我见过最JB难用的APP。

非必要我根本不想打开这个软件。非常适合你买了什么好股票然后忘记。

令人作呕的操作界面。一堆看不懂的按钮。离奇的提示弹窗。混乱的盈亏计算方式。像一坨屎一样的K线。

这一切都是为了让你别看线。拿住。

中文

Easiest way to gain 800 followers 🔥

Just say = Hello ❤️ let follow you 🫂💝

English

China didn't respond to Germany's "engineering" surplus by sitting on its hands -- it had a rather active industrial policy to substitute Chinese production for German imports (including by buying and digesting Kuka), and now it turbocharges its exports with a weak currency

Rory Green@rorygreen5

One reason Beijing struggles to take EU trade complaints seriously

English

没想到这篇帖子引起了这么新推友(新面孔)的共鸣,

没有其他的,我只感受到了真诚+感动

今天我慢慢回关,谁都不会漏掉❤️

我发现每天发推就像一个人的作息轨迹:

-早上互动暖场

-中午发文

-下午加强互动

-晚上总结

我感觉这是一条激活时间线冷启动的简单路径

--

这是一条回关温暖贴

0xjayfi@0xjayfi

其实我特别愿意关注刚起步的推友(低于500粉丝)以及和他们互动, 虽然我也不是什么大V 因为: - 自己也是这样过来的,理解起号的艰难 - 很多这样的推友非常活跃,非常愿意互动 - 经常会从这些推友的内容上学习到很多非常有价值的内容 - 说不定就榜上了一个未来的百万粉丝大V,哈哈 互关互爱~

中文

感谢各位大佬,蓝V又多了100位,离我的目标5000就差不到300人了。

蓝V互关第二十期。

第十九期的都已经回关喽,没有回关的评论区艾特我一下,我都会回关~

真诚找互关好友啦!关注必回,秒关不鸽~

#蓝V互关

小孩💢@caicai1953

蓝V互关第十九期。 第十八期的都已经回关喽,没有回关的评论区艾特我一下,我都会回关~ 真诚找互关好友啦!关注必回,秒关不鸽~ #蓝V互关

中文