Kepler Chevreux sobre Edenred, con un precio objetivo de 28€ por acción. $EDEN $EDEN.PA

Español

El Club del Value Investing

1.5K posts

@ClubdelValue

Comunidad formada por inversores profesionales que busca formar a inversores y aportar valor en forma de análisis profesional. 📨 [email protected]

‘THE SUPER MARIO GALAXY MOVIE’ has already passed $100M worldwide. Read our review: bit.ly/GalaxyDF

Nueva tesis publicada en el Club del Value con una rentabilidad por dividendo superior al 8%.

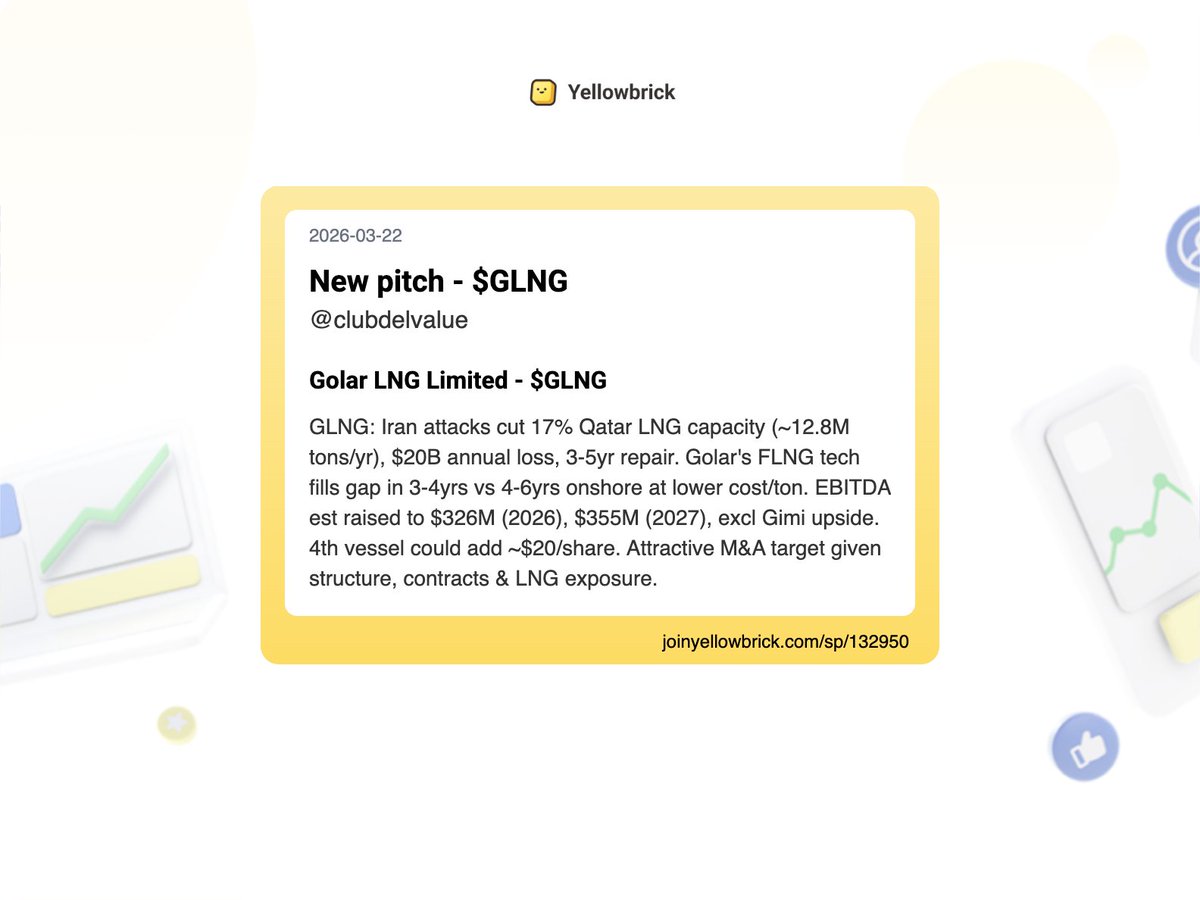

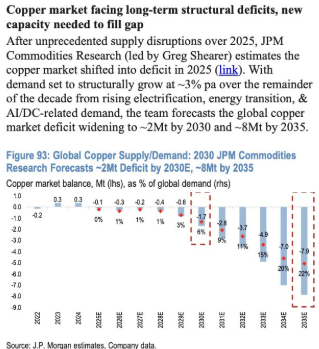

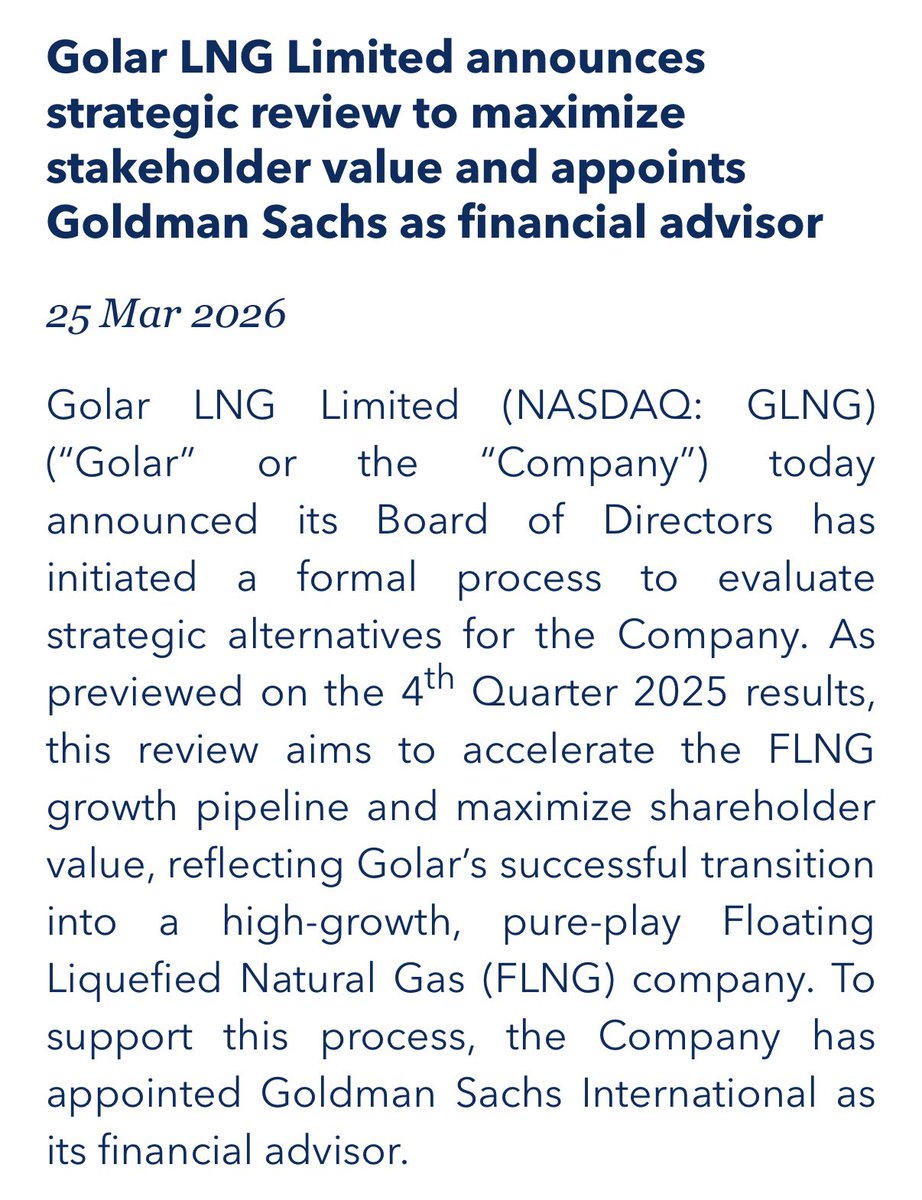

Nuevo artículo en abierto, esta vez sobre Golar LNG. $GLNG