Dutch

2.6K posts

*PAKISTAN OFFICIALS SAY 2ND ROUND OF US-IRAN TALKS EXPECTED

English

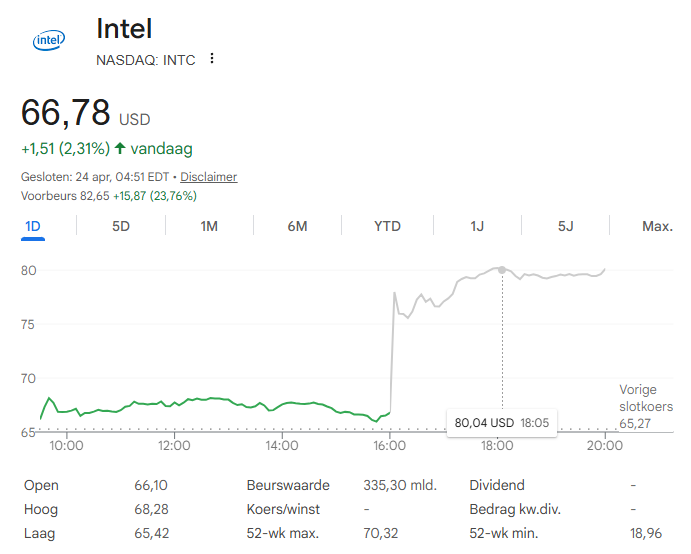

Deze koersreactie bij Intel $INTC is echt zotjes... Ik zie die comeback graag slagen, maar daar nu zo sterk op anticiperen...no thanks.

Nederlands

$BESI earnings today. Hybrid bonding customer count up to 20 with a second memory customer getting evaluation tools for HBM. Huge guidance. Next phase of the vortex will find these guys and their 65% gross margins.

Rob@boymanrobshit

$BESI We should talk more about set and forget names. Check out the gross margin on this one when you have time. $AMAT owns 9% and $LRCX was rumored as looking to aquire. Hybrid bonding is ultimately inevitable.

English

TRUMP ON IRAN: I'M THE LEAST PRESSURED PERSON IN THIS POSITION

- he's just too old to feel any pressure

English

@De_belegger Vindt jij $BESI niet overschat nu? Het aandeel staat echt heel hoog nu.

Nederlands

TSMC schrikt van prijs $ASML: nieuwste machines voorlopig te duur

De stap naar High-NA wordt alleen uitgesteld tot minstens 2029, omdat die machines met 350 tot 400 miljoen dollar per stuk nog te duur zijn. Voor ASML betekent dat tragere adoptie, maar de bestaande EUV-machines, upgrades en service blijven voorlopig de motor.

Overschat de markt deze tegenvaller voor ASML?

Nederlands

$Besi laat zien wie écht verdient aan de AI-boom.

Q1 2026:

• Nettowinst: €51,6 mln (+63,8%)

• Omzet: €184,9 mln (+28,3%)

• Orders: €268,7 mln, ruim verdubbeld

De motor? Advanced packaging en hybrid bonding voor AI- en geheugenchips. En Besi verwacht in Q2 nóg meer versnelling.

Steeds meer lijkt Besi geen cyclisch chipaandeel meer… maar een structurele AI-winnaar.

👉 Is dit volgens jou nog steeds een koopje, of loopt de koers al vooruit op de hype?

#Besi #AI #semiconductors #beleggen #aandelen

Nederlands

$Besi €269.7m orders in the 2026 hype: the hybrid bonding “surge” is just low-volume eval tools & prototypes, while real high-margin production for AI chips, HBM stays delayed. It was supposed to be red-hot by now, but it’s clearly not accelerating. SOURCES

English

@ArendJanKamp Wacht maar tot hybride bonding overschat gaat worden. $BESI is een €100 aandeel.

Nederlands

Voor u uw aandelen in de EUV-shredder gooit, bedenk dat #ASML (long) dit niet vandaag uit de krant haalt, maar al lang weet

#TSMC en ASML werken al ruim 30 jaar innig samen

ASML had vorige week echter prima cijfers en (lange) outlook (met dit dus in het achterhoofd)

TSMC bestelt wellicht wel (meer) andere ASML (EUV-)machines, want het moet hoognodig investeren

Arend Jan Kamp@ArendJanKamp

#ASML zegt het zelf ook, zijn machines zijn eindeloos te tweeken en te pimpen, waardoor er meer uit gehaald kan worden. Zo trekken de Chinezen chips uit de minder geavanceerde DUV-machines, die zelfs de folder niet beloofde

Nederlands

Orderboek, outlook en ook de rest is allemaal (veel) beter dan verwacht bij #Besi

Vraag is in hoeverre dit al is ingeprijsd bij dit peperdure en op all tme high staande aandeel

Nederlands

@BeuvingJordy BESI does emphasize progress in Q1 (orders and adoption), but 2026 remains a ‘very important year’ for the timing of broader HBM adoption.” (finance.yahoo.com). In my opinion, this is too weak.

English

@DutchTrading111 In line with css and more than enough to reach FY2026 css, especially with these orders. Why bad?

English

🌐 ✅ 📈 🚀 👇 BREAKING: BE Semiconductor Industries (BESI) results are out! $BESI

👉 Summary: orders above css, results broadly in line & solid Q2 outlook + outlook Hybrid Bonding improved

Bookings Q1-2026

📊 Orders: €269.7 million

🔎 Estimates: €250 million

"Q1-26 orders of € 269.7 million more than doubled versus Q1-25 due to broad based growth across all Besi’s end-user markets, with particular strength in hybrid bonding, mobile and photonics applications. In addition, orders increased by 7.7% versus 23 April 2026 2 Q4-25 due primarily to a significant increase in bookings for hybrid bonding systems from multiple customers and end-user applications."

Results Q1-2026

👉 Revenue: €184.9 million

📊 Guidance: €175-191 million

🔎 Estimates: €187 million

👉 Gross margin: 63.5%

📊 Guidance: 63-65%

🔎 Estimates: 64.2%

👉 Operating income (EBIT): €63.9 million

🔎 Estimates: €65 million

“Besi reported strong first quarter results and advanced packaging orders in an improving industry environment. Revenue of € 184.9 million increased 28.3% versus Q1-25 due to higher shipments for highend mobile and 2.5D AI photonics and datacenter applications."

Outlook Q2-2026

👉 Revenue: mid €250 million (plus 30-40% QoQ)

🔎 Estimates: €230-250 million

👉 Gross margin: 64-66%

🔎 Estimates: 64.3%

"Based on our backlog and feedback from customers, we anticipate that Besi’s Q2-26 revenue will grow 30%-40% versus Q1-26 as revenue and order momentum continue versus the prior year period. In addition, gross margins are anticipated to increase to a range between 64%-66%. Operating expenses are anticipated to be flat to up 10% due to increased revenue and customer support activities. As a result, we anticipate a significant expansion of our Q2-26 net income and profit margins relative to Q1-26 and Q2-25.”

Full press release: besi.com/investor-relat…

$ASML $BESI $KLIC $ASM $NVDA $TSM $AMAT $AMD $MU $INTC $LRCX

English

Besi $BESI heeft cijfers over het eerste kwartaal en blijkt verder te versnellen.🔥

Dit zinnetje is veelzeggend: Orders of €269.7 million were up 7.7% vs. Q4-25 primarily due to a significant increase in bookings for hybrid bonding systems.

Later meer op StockWatch

Nederlands

En dan te bedenken dat we een maandje geleden op €950k stonden…

Nederlands