Tweet fixado

mod323

722 posts

It’s worth pointing out that an unfreezable asset does no good if it can’t be spent. In 1945, Finland, who had managed to fight the Allies, the Axis, and the Communist bloc at various points in WWII, had a population sitting on piles of cash (goods were rationed during the war) and few things to buy with them. Fearing a burst of inflation similar to what the US experienced post-COVID, the Finnish authorities came up with a novel way enact financial repression on otherwise censorship resistant cash. Effective immediately, all large denomination bills were to be cut in half. The left side was still cash - worth half the face value. The right side was now a 4-year bond yielding a paltry 2%. Needless to say, Finland still suffered robust inflation (well above 2% paid). It also left bank accounts untouched, for reasons I’m not clear upon. As you know, most of the monetary base is made up of bank deposits, not physical cash. But it’s a good example of how even if the asset itself has no freeze or burn function, if those who would otherwise accept it in payment can be squeezed, you still have a problem.

Credifi v.1 goes live today! Borrow $100–$20K for three months at 4% fixed interest rate. No collateral. No fees.

Credifi v.1 goes live today! Borrow $100–$20K for three months at 4% fixed interest rate. No collateral. No fees.

Credifi v.1 goes live today! Borrow $100–$20K for three months at 4% fixed interest rate. No collateral. No fees.

Credifi v.1 goes live today! Borrow $100–$20K for three months at 4% fixed interest rate. No collateral. No fees.

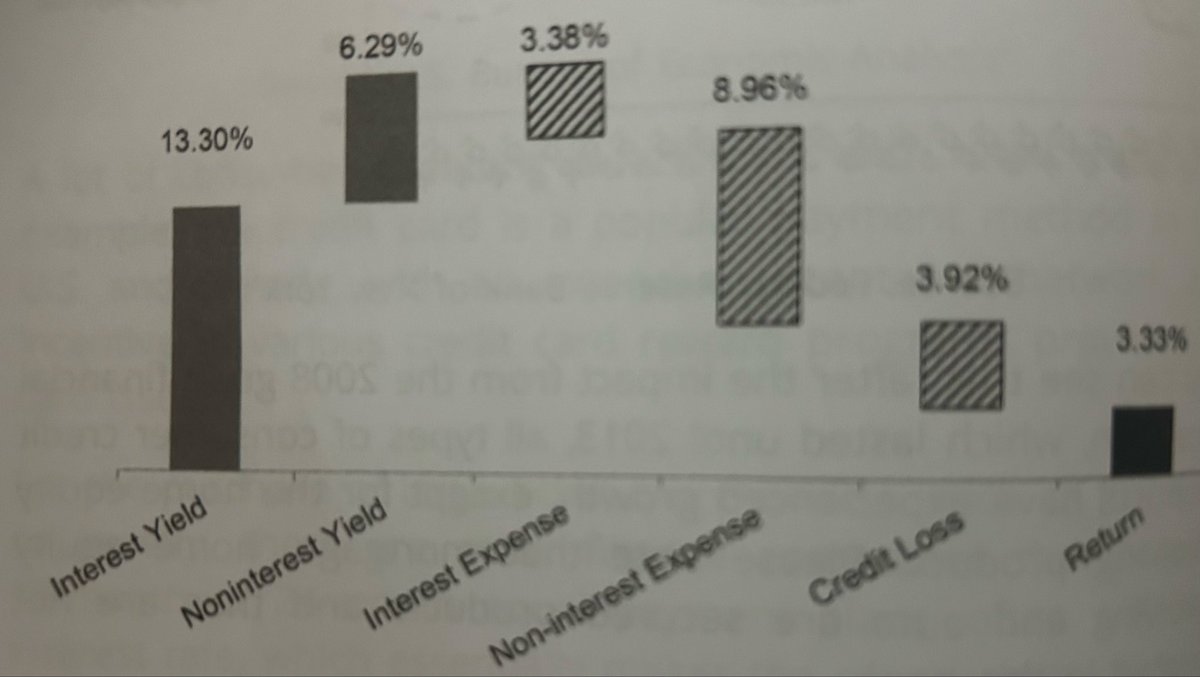

The global unsecured credit market is ~$5.3 trillion. In the U.S., the cash flow-based financing market (i.e., credit cards, business advances, trade margin) is ~$1.3 trillion. Unsecured credit is one of the biggest opportunities for crypto over the next year.

New episode out now with @linfluence of @reforge_vc 🎙️ He breaks down how he spots frontier opportunities in programmable money, infrastructure, and the coordination stack. Inside the ep: 🔧 Why coordination systems are breaking and where the rebuild starts 🏦 How Reforge sources founders earlier than many traditional funds 🤖 Using AI agents to support deal sourcing and diligence 🌱 What a coming secular spring may mean for crypto and capital markets Watch: youtu.be/IBWdIy3LpSM Listen: tinyurl.com/A2A-Ep-51