Perspez@perspez

$OSS (One Stop Systems) still flying under the radar around a ~$200M market cap, and the setup is pretty compelling if you like microcaps with “platform supplier” upside.

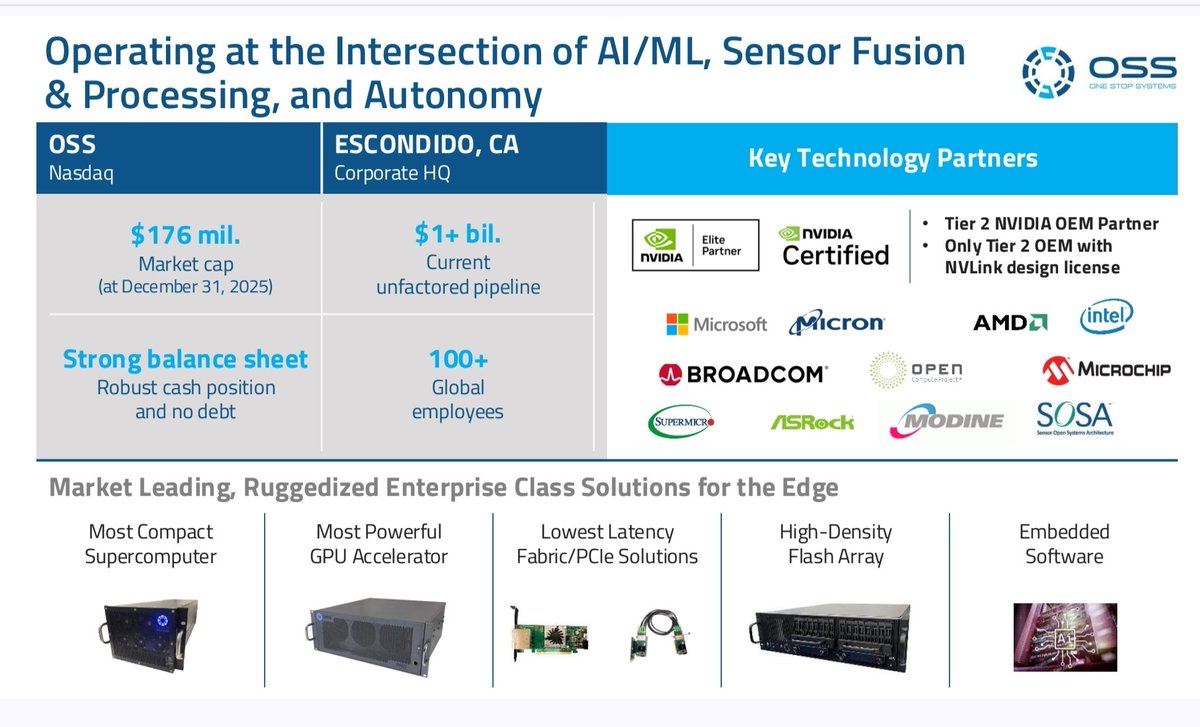

■What OSS does

They build rugged, datacenter-class compute + storage for places where normal servers can’t operate: defense aircraft/vehicles/ships, mission systems, and industrial autonomy. Think AI + sensor processing at the edge (low latency, high bandwidth, rugged, engineered for the program).

■Why it’s getting interesting now

They’ve made the story much cleaner:

- Sold their European unit Bressner for ~$22.4M → removes the lower-margin reseller layer and leaves mostly the higher-value core business.

- Raised ~$12.5M (registered direct offering) to support growth/working capital → positioning to scale, not just survive.

■The “good bits”

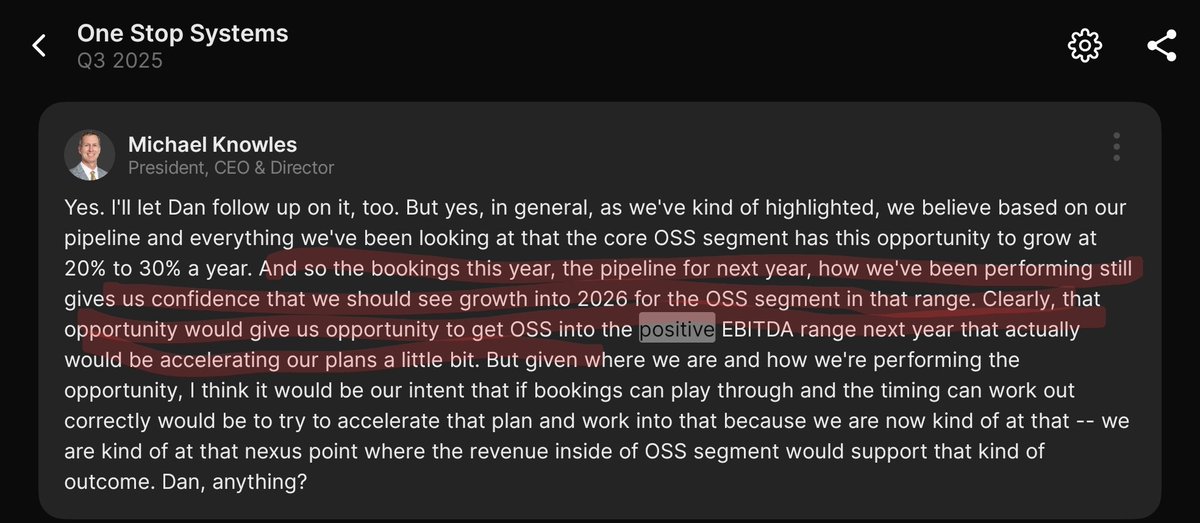

- Raised FY2025 consolidated revenue guidance to ~$63–$65M.

- Their deck frames core OSS (post-Bressner) revenue around ~$30–$32M as “continuing ops” — so you can model the real business now.

- They cite TTM book-to-bill ~1.4x → orders > shipments = backlog building.

- They highlight ~44% gross margin and expect positive full-year adjusted EBITDA (2025).

■The real bull thesis: platform flywheel (not one-off box sales)

- Their deck calls out a P-8 platform case study with $50M+ revenue to date (land → expand → sustain).

- That’s the blueprint: customer-funded development → production orders → follow-ons → sustainment/tech refresh.

■The upside “optionalities” people are missing

This is where it gets spicy:

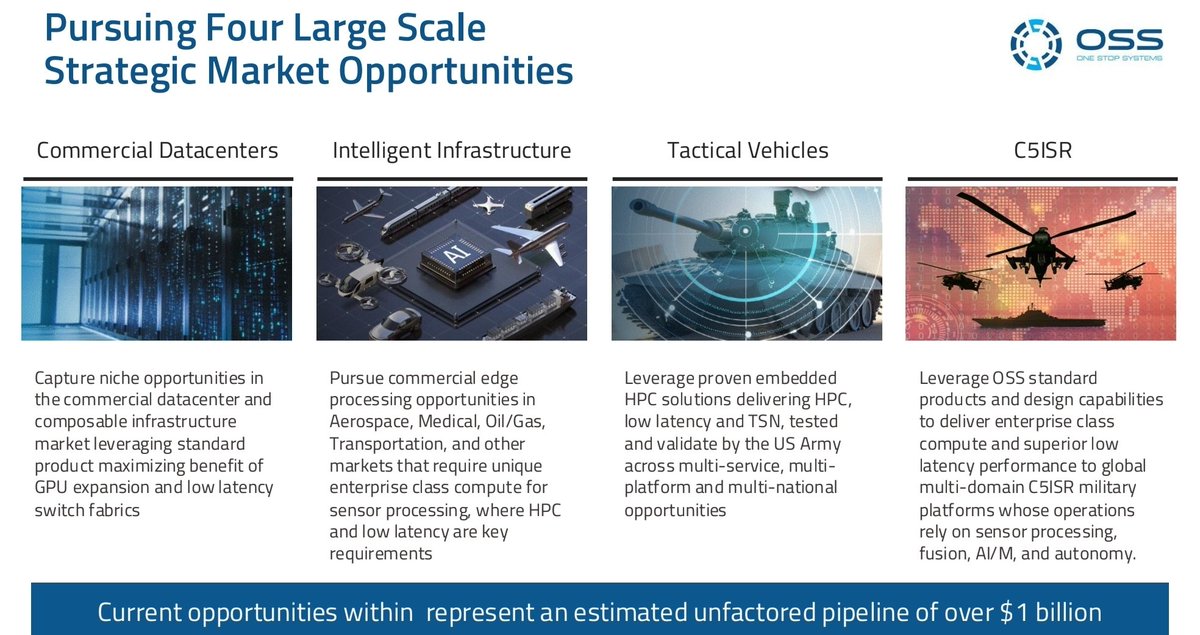

- OSS has discussed a ~$200M multi-year opportunity tied to a major U.S. Army tactical vehicle / situational awareness rollout (IF it moves from testing/evaluation into funded fielding).

Important: it’s an opportunity, not booked revenue — but it shows the scale of what a single platform decision could mean.

- They’ve also referenced a ~$200M pipeline opportunity in datacenter / composable infrastructure (again: not backlog, but a real “call option” if it converts).

■Why the market may be mispricing it

- At ~$200M market cap, you’re not paying much for:

- a cleaner pure-play structure (post-Bressner),

- a backlog-building profile (book-to-bill >1),

- a high-margin core (40%+ GM profile),

- and proven multi-year platform footprint (P-8 track record),

- plus the kind of $200M-scale platform optionality that can re-rate a microcap fast if it materializes.

■What to watch in 2026 (the “proof year”)

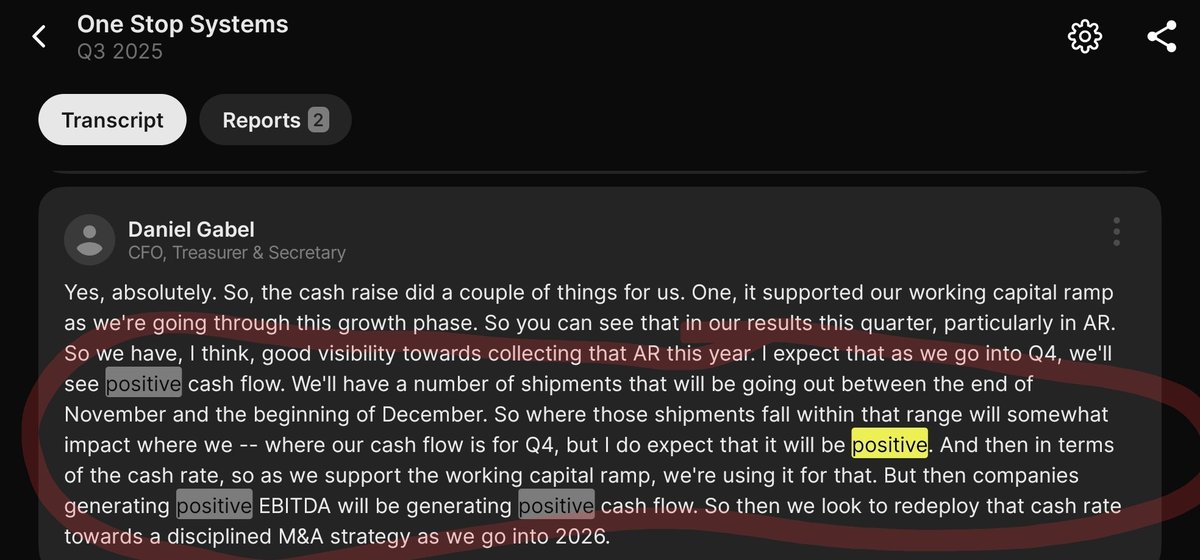

- Does backlog convert into shipments + cash (AR/working capital is the main risk)?

- Any follow-on awards / new platform wins that show “next P-8” is forming.

Not financial advice – just flagging a microcap that’s starting to look like a real edge-AI / defense platform story while still valued like nobody knows it exists.