Alex_Capital

481 posts

Alex_Capital

@Alex84Crypto

$AMD $NBIS $ONDS $PATH $RKLB $ASTS $BTC

Присоединился Mayıs 2022

867 Подписки154 Подписчики

Alex_Capital ретвитнул

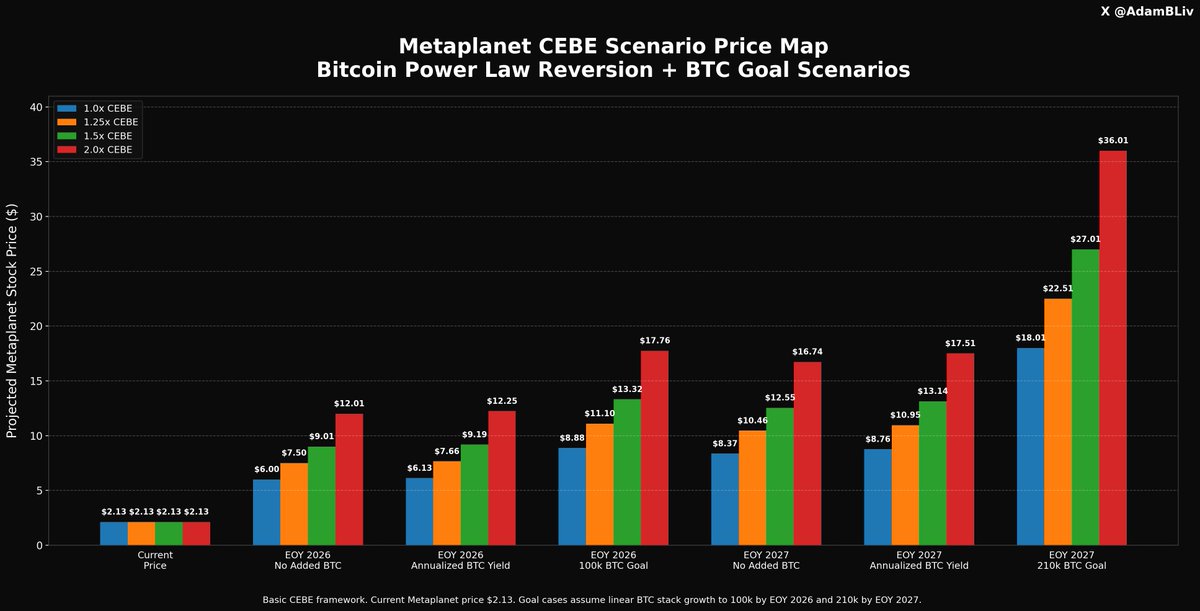

Metaplanet Stock Price Projections

After loading up on more MSTR + ASST shares this year I am back to loading up on Metaplanet.

The reason I think Metaplanet is underpriced here is simple:

The market is still valuing it like a discounted Bitcoin wrapper when it could become a very serious Bitcoin accumulation machine.

Here’s the setup:

0.87x market cap to BTC NAV

0.99x EV mNAV

40,177 BTC already on the balance sheet

preferred and senior financing still not fully understood by the market

BTC Yield still early

huge upside if Bitcoin simply moves back toward trend

even more upside if the balance sheet machine actually works

That is the opening.

I want to buy BEFORE there is consensus on the prefs.

Now:

I ran a CEBE-based scenario map using Metaplanet’s current balance sheet, then layered in:

a conservative case where BTC Yield is simply annualized from their YTD number

a more aggressive case where they linearly grow the stack to their BTC goals by end of 2026 and 2027

zero common dilution in the modeling so we can isolate the balance sheet torque

Here’s what falls out:

Current Metaplanet price: $2.13

EOY 2026, BTC at $200k, no added BTC:

$6.00 to $12.01

EOY 2026, BTC at $200k, annualized BTC Yield:

$6.13 to $12.25

EOY 2026, BTC at $200k, 100k BTC goal:

$8.88 to $17.76

EOY 2027, BTC at $275k, no added BTC:

$8.37 to $16.74

EOY 2027, BTC at $275k, annualized BTC Yield continues:

$8.76 to $17.51

EOY 2027, BTC at $275k, 210k BTC goal:

$18.01 to $36.01

To be clear:

I do not know they hit the 100k and 210k BTC goals.

Those goal cases assume linear growth of the BTC stack and zero common dilution for modeling purposes.

But that is the point.

Even if you ignore the moonshot cases and just look at the conservative balance sheet math, Metaplanet still looks very underpriced if Bitcoin reverts back toward the power law trendline.

Even if I don't get these returns in 1-2 years... if I can get them in 3-4... I will be MORE than a HAPPY CAMPER.

Why this works:

CEBE strips away the fairy dust and asks one question:

How much Bitcoin is actually left for common shareholders after senior claims are accounted for?

That matters because as BTC rises:

the company’s BTC stack gets repriced upward

debt and preferred claims stay fixed in dollars

those fixed fiat claims shrink in BTC terms

common equity captures more of the upside

That is the whole game.

With Metaplanet, the market is staring at:

a huge BTC treasury

sub-1x EV mNAV

market cap below BTC NAV

an early-stage financing engine

and a balance sheet that could become much more powerful if the market accepts the prefs

The beauty here is that the upside does not require some insane meme-stock premium.

It just requires:

Bitcoin moving back toward the power law

management continuing to accumulate BTC intelligently

senior financing remaining viable

common dilution staying restrained

If BTC hits $200k in 2026, Metaplanet already starts looking dramatically mispriced.

If BTC hits $275k in 2027, the stock starts looking like a compressed spring.

If they actually scale toward 100k BTC by end of 2026 and 210k BTC by end of 2027, the stock price path gets absolutely stupid.

If the machine works, common equity holders are sitting on a very nasty asymmetry.

I think Bitcoin will be at $1,000,000 in less than ten years, so if I can get these gains in 3-4 years...

...now is the time to STRIKE.

English

@daniel_koss Great read, appreciate you sharing the discipline and transparency. Curious how you’re thinking about allocation across your current positions, what % are you running in each?

I’m with you on staying cautious here, also in $NBIS and $HIMS.

English

Yesterday was pretty great!

Strong moves for all my positions

$HIMS

$LPF / $LPFK

$OUST

$SHMD

and finally a juicy dip in $NBIS below 8ema which allowed me to add it back!

Overall market looks completely overvalued to me. Generally I think now is a very bad time for FOMO and leverage.

This is also why I decided to sell both $NVTS and $VICR at just a net 10% gain.

I see all the smart people saying power semis are next and I believe it. But after I updated my macro analysis I immediately decided that it's one of the worst times to hold such overvalued names.

Obviously they can always go much higher. I sold $OKLO between $120-$140 and then it ran to $180 before crashing.

Right now I do think well see many such names crash if we get any narrative violation in earnings.

If certain metrics I'm tracking hit my risk bar, I will seriously consider going 100% cash for a while. Have only done that once (tariff escalation).

Will share that here transparently, even if I know going cash will be a super hated move.

English

@aleabitoreddit @aleabitoreddit would be great an updated view from you on this brother! Thanks 🙏

English

Based on the equity ranking table:

Here's a deeper analysis of each stock, alongside how I reposition my portfolio to capitalize on the market reset:

· $NBIS at $92, PT $400 / 1Y

· $RKLB at $43, PT $500 / 5Y

· $CRCL at $72, PT $150 / 8M

· $ALAB at $143.4, PT $250 / 6M

· $SNAP at $8.1, PT $22 / 1Y

· $CIFR at $14.8, PT $28 / 6M

· $RDDT at $185, PT $275 / 8M

· $SMCI at $34, PT $55 / 6M

· $HIMS at $35, PT $60 / 6M

This is in order of concentration weighting from when posted and internal PT speculation based on existing information for mid-cap ($5B+) sections.

Here’s a deeper breakdown on each one and PT timeframe, and a “qualitative”why:

1. Nebius ( $NBIS ): $23B marketcap. Incredibly undervalued and detached from fundamentals.

$7-9B forward ARR, 20-30% EBIT, enterprise contracts from Shopify, Accenture, Cursor, foreign governments and hyperscaler contracts from Meta and Microsoft give Nebius revenue visibility. With $4.8B+ in cash, it's isolated from credit tightening affecting data centers. With 2.5 GW expected capacity contracted 2026, it rivals many others eg. $IREN at 2.8 GW, and defeats many of the capacity/power arguments. With many portfolio companies powering companies like Tesla and Anthropic, it also has higher growth potential (think $MSFT with its portfolio companies for longer defensibility).

We also had stellar $NVDA earnings going into Q4 with their blowout, Jensen clarifying arguments against GPU depreciation, which helps with DC sector sentiment.

$400 1 year price target, $100B+ valuation given forward revenue/margins.

2. Rocketlab ( $RKLB ): $22B marketcap. Overvalued current term, undervalued long term potential.

Rocketlab is my highest conviction 5Y long alongside Bitcoin. With Space, it's not winner takes all, and I've maintained $350-500B long term PT to match SpaceX’s most recent valuation/capabilities.

As of now, it's overvalued. But it's an incredible + defensible moat from purely a technological standpoint building reusable rockets and we're early in terms of commercialization of their end-to-end space products at scale (likely ~2028).

However, we're pricing in forward growth with Flatlite commericalization (eg. Starlink), and medium-lift payloads (SpaceX Falcon 9). The market prices in forward growth as well but it’s more about how long in the future with Rocketlab. It's always a solid buy, depending on how patient you are with company execution.

3. Circle ( $CRCL ) - $16B marketcap, undervalued.

With Circle, I've been bear posting it since it was a $50B marketcap, saying short Circle, long Coinbase, given $COIN has 50% revenue sharing with Circle.

It was overvalued due to float numbers and massive insider lockups 2-3 days after earnings/Dec 2nd led to a sell-off (like $BULL). Float dynamics matter a lot that ETF managers like Cathie Wood seem to not understand (hence my warnings).

But now we're reaching respectable valuation numbers. I expect USDC commercialization to continue and given a regulatory focus in the digital asset market, I see $CRCL taking over a lot of Tether's marketcap.

That being said, it's well deserving of a $30B+ marketcap pricing in stablecoin volume growth once we start seeing insider shares redistributed to institutions and long term holders.

4. Astera Labs ( $ALAB ) - $22B marketcap, reasonable valuation

ALAB was one of my mid-term high conviction picks, due to Mag7 adoption of connectivity for datacenter buildout.

Incredibly high growth and $NVDA-like margins sitting at ~74%, latest er: $230m/q (101% Y/Y growth). My thesis was that if Mag7 is dependent on a company ($NVDA for GPUs) ( NBIS, IREN, CIFR for DC AI cloud buildout), the company will blow away expections quarter after quarter, and we're seeing this.

There's been a recent sell-off on Astera from $250 back to $140 marks, depsite beating earning expectations across the board and this presents a good buying opportunity.

I maintain a medium term PT $250 for recovery after NVDA earnings and record-high DC buildout from Antrophic's $40B DC to $GOOGL's $50B DC in Texas + connectivity demand.

5. Snapchat ( $SNAP ) $13B marketcap, undervalued.

$SNAP is one of my least favorite stocks and CEO's (sorry Evan).

However, I can't argue with fundamental changes. A TLDR of my most recent thesis post was that they're cutting their massive opex bloat from memories/videos stored 10 years ago and if you look into their GCP hosting fees, it's cutting in margins.

Now they're both reducing that OPex cost and increasing revenue from that. We also have AI deals with perplexity adding $400m+ additional revenue streams like RDDT.

However, short term it's suffering from tax-harvesting due to underperformance this year relative to AI companies. In 2026 Q1, I expect the market to start pricing in the new fundamentals Hard. and for this company to beat expectation soundly.

That being said I expect over a 200%+ upside 1Y from here with the market pricing in the new dynamics.

5. CIFR ( $CIFR ) - Undervalued at $5B marketcap

$CIFR is my second favorite stock in the Neocloud sector. From memory, it holds a lot of Bitcoin on its balance sheet and is materially affected by the selloff in BTC prices from $120k to $90k.

However I expect crypto asset prices to recover in a few months once cascading margin liqudations finish and instituions buy-in Bitcoin at low prices.

Nebius is top because it owns the full AI-cloud value chain for higher revenue potential and stronger returns, even though it forces them to handle orchestration, software, and GPU lifecycle risk instead of sticking to colocation.

However, $CIFR because it avoids that entire risk surface and has backing from AMZN and GOOGL for long term revenue anchors. It also stays insulated from GPU procurement, management, and depreciation.

For CIFR's economics we get a a high-margin, annuity structure built on space, power, and cooling for hyperscalers. Risk-adjusted, it’s one of the safest names in the group. But the trade-off is capped upside Long leases like 10Y, 15Y slow the revenue ramp and mute the payoff relative to full-stack Neocloud operators like NBIS that go from $145m quarterly revenue to $2.1B in a year.

That being said I maintain a $28 PT in 1 month once market prices in $AMZN, $GOOGL Fluidstack revenue and Bitcoin prices recover.

6. Reddit ( $RDDT ) - Moderate valuation

Coming from the Wendy's dumpsters on WSB subreddit, I am naturally biased toward this platform.

However, the initial sell-off of Reddit at $270 was due to fears over ChatGPT citations, which was immaterial. Now, recent data shows that citations are back, but Reddit's price still sits at $185 (way below that number) + partly due to macro.

Reddit is one of the least bloated, highly profitable social media companies. And it's here to stay due to long term defensibility of the network effect of both younger + older audiences (compared to Snap 900m+ MAU of mostly younger generation).

I expect RDDT to scale up monetization avenues through acquisitions like $HOOD (exchanges) due to their massive FCF and profitability or how Facebook originally acquired WhatsApp, Instagram, built out messenger. It's a low-risk, high growth stock, which is why I maintain a $275 PT in 8 months.

7. SMCI ( $SMCI ) - Undervalued, $20B marketcap.

$20B marketcap is a joke. Nothing else to say. They're doing $5B quarterly revenue (off lower-margins for sure). However, market is pricing in the company revenue dropping.

SMCI quoted majority of the backlog delay to Q2 2026, which aligns with a lot of the DC buildout from Neoclouds to Mag7 customers.

They expect revenue to grow 50%+ Y/Y next year, with at least $36 billion revenue, but judging from DC buildout from blowout NVDA earnings, I expect server rack companies like $DELL and SMCI to outperform Q2 2026.

This is why I'm taking advantage of revenue lag delays from the current quarter and assigning a $55 PT in 6 months time.

8. Hims and Her Health ( $HIMS) - Undervalued ( $8B marketcap)

Personally, I've used HIMS just for short term trading breakouts. And I've been one to not long-term hold the stock above $50.

However, back at $35, it's reset most of the year's growth but grew revenue 49% Y/Y to $500m and is producing a good amount of FCF.

The most under-priced narrative is the Zava acquisition. This adds 1.3M+ users to the HIMS platform and allows the company to expand to the EU market.

Similar to how META acquires companies like Instagram, grows its base + monetizes, I expect HIMS to do the same with Zava + market is pricing in current est. Zava numbers.

It's probably my least confident stock out of the bunch, especially leaving me with a bad taste with the CEO selling shares after leaving 👀 on SS posts back at $70.

But that being said it's a great rebound opportunity to $60 in a 6 month timeframe.

Hope you enjoyed my perspective. There's a lot of x at price posts, but I try to leave a more qualitative breakdown (+ part quantitative but leave out a lot of technical for easier reading) to help retail develop their own conviction and understanding.

Building understanding is important to create internal valuation models yourself rather than blindly following along FinX posters + capitulating when stock prices temporarily drop.

Happy to discuss more if you drop your own portfolio + concentrations.

Serenity@aleabitoreddit

The Great Reset, November 19th ratings: Strong Buy · $NBIS · $CIFR · $WULF · $RDDT · $SNAP · $ALAB · $META · $AMZN · $GOOGL · $IBIT · $SOL · $TSM · $RKLB · $TSSI · $SMCI · $GLXY · $SG Buy · $IREN · $KRUS · $CRCL · $LTC · $MRVL · $KRKNF · $OSS · $CORZ · $WLAC · $WYFI · $AMD · $TE · $CRDO · $FLNC · $HIMS · $BULL · $ETOR · $FISV · $FLY · $MU Hold · $COIN · $HOOD · $IBKR · $NVDA · $PLTR · $TSLA · CRWV · $APLD · ORCL Avoid · RGTI · $IONQ · SLNH · $QBTS · OKLO · $WMT · BMNR · $SBET · CRWV _ Explanations Strong Buys Nebius - Extremely undervalued, $7-9B ARR, reset to pre-MSFT deal prices, despite tripling their projected ARR since then, de-risking across the board, and having $4.8B cash for capex spend. Having that much in the balance sheet also isolates them from market credit tightening affecting CRWV and related companies. MSCI inclusion next week delivers an additional few hundred million to low billion in flows for price pressure CIFR - Very undervalued after reset, colo/leasing models with AMZN, GOOGL via Fluidstack isolates them from Burry short arguments. De-risked having long term revenue visibility via hyperscalers. Wulf - Same boat as sifter, GOOGL JV via Fluidstack de-risks them with long term revenue visibility. Not affected by GPU depreciation arguments. Just slow ramp like CIFR due to not doing full stack AI cloud offerings. Reddit - They're back to pre-ChatGPT fear search volumes, yet it's down from $270 to $185. Great earnings, extremely defensible social network to network effect. Not going anywhere. SNAP - $400m+ revenue/year added from AI partnerships. They're also increasing opex efficiency with Google Cloud costs from memories and then monetizing revenue from storage like iCloud. Extremely undervalued going into 2026. Obviously there's going to be tax harvesting from performance this year but very strong by mid December going into 2026. ALAB - Strong earnings beat across the board. Affected by your usual random sell-off. Last time this happened and they had all earnings beat they went from $100 -> $50 and then rallied to $250. This time it's happening again. META - Sub 20 forward p/e. Earnings were one-time tax, even though they beat expectations across the board. Meta > Amazon > Googl in terms of my undervalued mag7 list. Amazon - Fundamentals are increasing across the board and we're reaching your holiday spending time with Black Friday/December sales. Google - They're starting to sell TPUs like NVDA, Gemini 3 is amazing, Buffett is buying buying, they have everything forward for them. Bitcoin (IBIT) - Once in a year buy at $92k. All your leverage traders got margin liquidated and post margin-liquidations are typically when you want to buy for recovery. Don't see this being the same as Nov/Dec 2021, because there was fed tightening. It looks the same but we just came off two rate cuts. Solana - post margin liquidations, high usage but very centralized network riding stablecoin hype. Great recovery buy at $138 TSM - Not quite sure why they sold off. They already projected blowout quarter, blowout forward earnings with increased ~3% margins, and blowout current revenue. They're the center of the whole AI buildout. Rocketlab - Great buy off the 40%+ drop. This is a long term buy (rather than a swing trade), Neutron delay doesn't really affect long term fundamentals if you wait an extra bit. TSSI - Dell/SMCI is a pretty good proxy to see how this company would do. SMCI orders apparently will skyrocket Q2 2026, when the whole datacenter buildout starts ramping up. Revenue lag or quarter miss shouldn't be that bad. SMCI - Same here, quarter miss but forward revenue is insane and this company is very, very undervalued. Normally markets are forward looking so not quite sure why they're looking with blindfolds with companies like SMCI. GLXY - Amazing earnings, just affected by sector selloff. SG - People still eat their salad, it's basically reached all time low at $5.8 and was $40 just 1 year ago. Great recovery buy. Buys IREN - I DG'ed because they ended up buying GPUs and doing full stack iaas and orchestration is more complex than people think when they do deals for MSFT. But that aside it got sold off way too much alongside other DC sector stocks. KRUS - Kind my hidden swing trade stock but decided to release it because why not. We've kinda hit that bottom mark if you want to zoom out to a 5y timeframe you'll see what i mean. CRCL - This was my strong sell stock for the longest time because of dilution. We've hit the point where MC is reasonable again ~$17B and stablecoin volumes like USDC will grow. A huge percent of the float was either 2D after earnings or ~Dec 2nd, I haven't looked into it exactly, but it could go lower which is why I didn't raise it to strong buy. LTC - Litecoin ETF didn't have much of an impact as expected, but if you've been watching since the most recent sell-off, Litecoin held its ground much beter than other cryptos. There's been a lot of altcoin rises like ZCash randomly, so Litecoin has potential. MRVL - They're not priced like other semis that grew 57%. KRKNF - Anduril supplier, and long term defensibility due to critical military components. OSS - Likely anduril supplier, low MC anyway, potential for $200m+ contract even at $100m MC CORZ - $8.7 billion colo with CRWV over 12 years gives CORZ more predictable cashflows, and majority of capex ~80% ($~196m/ $244.5 million Q3) or so was funded by Coreweave, which is a lot nicer of a model for shareholders than convertible debt or toxic debt interest cutting into margins. ~1.3-1.5 GW capacity, Coreweave only taking up 500 MW, and revenue offsetting capex makes it really good. Reason it's not strong buy is Coreweave lol. Extremely high interest debt and openai taking up close ~1/3 of their backlog is worrysome. WLAC - Waiting for spac IPO. High potential there. WYFI - I didn't like this as much due to no long term revenue visibility with hyperscalers, etc. and they didnt get such contracts in their last ER. That being said it got reset to IPO prices so even if I didn't like WYFI as much before, it's a decent buy again. AMD - Huge demand for small/medium sized models/inference. Especially with backlog coming from OpenAI. That being said it's OpenAI that promised $1T+ in capex they don't have so it's not strong buy anymore just given openai competition from gemini3, grok, and other llm models. TE - Energy play that got sold off. CRDO - Same reason as ALAB but it didn't drop as much so it's not as strong as a buy; still great company for connectivity with mag7 clients. FLNC - Energy that got sold off HIMS - Improving fundamentals with Zava acquisition coming in this quarter, $250m+ buyback, pretty solid. BULL - Retail trading is still popular, potential for strong monetization like Robinhood just because of large retail clients. ETOR - 15 p/e or so, 1/3rd cash, pretty undervalued but just tax harvesting. FISV - seems like a UNH type buy at $250. FiserV doesn't look like it's going anywhere at ~7.5 forward p/e 9/e. I'll do a deeper dive one day. FLY - Same thesis from before, medium lift payload with northrop gives it a higher chance of succeeding (when competing with RKLB on reusable medium lift). It's just waiting for 2026 and then stock price is lower than it was before. MU - Memory demand is insane during AI Ramp Avoid RGTI IONQ QBTS - Quantum zero revenue. Probably longer recovery window during high beta selloff because they lack fundamentals to back up MC. SLNH - Just taking advantage of data center hype to raise funds/dilute, with marketing 2.8 GW capacity buildout. If they can convince people to keep giving them money then sure it might pay out but otherwise just stay away and go with nebius or cifr. OKLO - zero revenue, way ahead of its time. WMT - nobody can convince me that walmart which is growing at 3-4% a year deserves a 40 p/e. BMNR, SBET - just buy ethereum as an underlying asset. But that being said I wouldnt buy ethereum above $3k either so these two are a sell. CRWV - so if you're short-term trading, it's actually a extremely solid recovery buy at $75. But.. if you're holding, yeah i'd stay away due to high interest debt cutting into margins, large contracts with openai (like ORCL), still a question mark where openai's getting $1t+. Not quite sure why anyone would buy coreweave when you have nebius which is better in every metric. _ Commentary This is just extremely TLDR-light and half-feels, don't take it as actual DD (but I personally trade on this) That being said, this market wide drop in growth stocks is an amazing opportunity to load up in names you didnt have before (eg. NBIS, RKLB, IBIT, others).

English

Alex_Capital ретвитнул

@Sandeman52 congrats, incredible results and you were one of first people who introduced $NBIS to me, riding 2000 shares with you

English

Wow guys…I just crunched my updated stats as of yesterdays close…and I am incredibly humbled. 🙏

Over the last 12 years:

24,900% gains

CAGR: 58.5%

That’s an average return of 58.5% every year for 12 years in a row.

Yes, it’s a snapshot in time. Things could change.

I think I’m done posting net worth and exact $$$ numbers. It’s bad karma. Plus I don’t need the added headaches.

As far as percentages though, I’m very pleased and feel incredibly blessed. 🙏🙏🙏

English

Here’s a look inside my €2,060,847 portfolio:

% + (cost basis)

$PLTR 67.6% ($10) 📊

$TSLA 11.2% ($68) ⚡️

$AMD 8.2% ($97) 💻

$SOFI 4.3% ($7.8) 🏦

$HIMS 3.3% ($24) 💊

$SPOT 3.2% ($146) 🎵

$META 1.8% ($284) 💬

Total unrealised P/L: +€1,602,318 🟢

Any stocks you recommend? 💬

English

@aleabitoreddit Great results, impressive. Would be keen to hear how you’re positioning a model portfolio over the next 12 months given the current market.

English

They’re still there.

It’s just hard to say anything….

When all my recent thesis posts from $HPS.A, $IQE, $AXTI, $SIVE, $AAOI, $LITE, $NBIS, Win, Shunsin, $AEHR, $TSEM, $SOI, and many many others I call out.

Just hard outperforms the market.

Year to date of +1,116.29% isn’t too bad, right chat?

strictrope@strictrope

@aleabitoreddit Your haters seemed to have disappeared!

English

Thinking 3-5 years out, what’s the best play here?

A) $NBIS

B) $IREN

C) $SOFI

D) $HIMS

I keep asking myself WHICH SHOULD I ADD?

English

From 11:30-12:30 I will run through any symbol you want and give you the reading

1hr Symbol AMA for Subscribers Let's Go!

English

Alex_Capital ретвитнул

🇺🇸🇮🇷 U.S. intelligence believes Iran's new Supreme Leader is gay.

The source: one of the CIA's most protected assets. The confidence: high enough to brief the President.

Iran has executed thousands for exactly this since 1979.

The revolution didn't just eat its children.

It may have crowned one.

NY Post, @clashreport

Mario Nawfal@MarioNawfal

🚨🇺🇸🇮🇷 U.S. government warns that Americans in Iran face a significant risk of questioning, arrest, or detention. Authorities say even showing a U.S. passport or U.S. ties could get you locked up. They're told not to travel to Afghanistan, Iraq, or the Pakistan-Iran border region, while land routes to Armenia, Turkey, and Turkmenistan are open. Source: US Embassy Security Alert

English

@Sandeman52 Holding 2,000 shares strong with you, bro 🚀 Obviously pocket change for your portfolio.😅😂

English

$NBIS $950k gain on my portfolio today,

plus the $50k in premium I made from puts I sold,

blessed to say $1M gain today.

Will it come back down?

Maybe.

Does it matter?

No.

Why not?

Because this is just the beginning.

That simple.

Let’s go fam! 🫡👍👊

English

Alex_Capital ретвитнул

This war is over by April 1st. Like this post and retweet it. If you do and I’m wrong I’ll give one of those lucky people $1000 through Zelle. Gotta have Zelle.

English

$NBIS like I said. I wasn’t worried. Made this back and then some thanks to the puts I sold.

SandemanStocks@Sandeman52

I can make you feel better. I’m not worried and give zero Fooks

English

@aleabitoreddit Do you still see $NBIS as a long? I rememebr you had $400 target by EOY...

English

Last year I shared my 1 year return:

630.44% before I even joined X.

Lot of conspiracy theorists out there.

But I do happen to be a decent discretionary trader.

Large part of it was

> front-running halving

> buying $RKLB in the 10’s

> buying $HOOD in the 10’s

> catalyst trading Presidential nominations

> riding multiple waves up.

Majority of people don’t rotate and sit on a single stock the entire time.

The trick is to ride every wave up and if earnings start to slow/stop, move on to the next and don’t get too attached to a stock.

It’s the same thing with this year, just different sectors and catalysts.

Serenity@aleabitoreddit

Year to Date: 412.72% Lot of it is just picking the right sector, profiting off of Jane Street algos weekly, and a bit of luck. In terms of bottleneck longs, these are currently my favorite: 1. Memory - Samsung, Sk Hynix, $SNDK, $MU, $SIMO 2. Photonics - $LITE, $COHR, $AAOI, $AXTI, (maybe Yamamura too, but not to the same degree). 3. Power/Grid - $XLU. 4. Advanced Packaging Capex - $AMKR, $ONTO, $CAMT, $KLIC, and $FORM. I’ve talked about all of these before aside from maybe $KLIC? But most if not all are up like 50-100%+ in a short timeframe, which amplifies overall returns from trading. Best lesson I’ve learned this year was to rotate where the money flows and current bottlenecks. Rather than attempting contrarian turnaround plays in sectors like cybersecurity. I publish all my ideas for free too so hopefully people can take away a thing or two!

English

If I had to turn $100k -> $1M in 1 year.

It would be: $XLU OTM 2 year leaps

2026 is the first time in modern history markets have:

- falling interest rates

- AI inference + buildout

There's a potential ~40% for XLU (1000%+ OTM), from mapping.

Here's my macro thesis:

1. Rate Cuts

When the Fed cuts rates without a recession, utility debt becomes cheaper, and institutional rotates low-yielding cash to for utility dividends.

This causes immediate valuation multiple expansion:

1995: The S&P Utilities sector returned +31.3% in 1995 and another +12.1% in 1996 - ~47% cumulative return

2019 Mid-Cycle Cut: Result: XLU generated a +25.9% total return in that single year

Standard soft-landing rate-cut cycle naturally maps to a 25% to 30% baseline return. And we're entering a new rate cut cycle in 2026.

2. The Infrastructure Supercycle Capex

Infra CapEx gives the sector compounding earnings growth. Following the early 2000s, utilities entered a massive CapEx cycle to modernize aging grid infrastructure.

Because they were constantly spending and expanding their guaranteed rate base, XLU returned +23.5% in 2004, +16.3% in 2005, +20.8% in 2006, and +18.4% in 2007.

However this time:

The $800B+ AI buildout of 2026 makes the 2004 grid modernization look like pennies.

So you have Valuation Multiple Expansion (+15% to +20%), from rate cuts from #1. EPS growth (+18% to +20%) from #2 from capex spend historically. Just from a history lesson.

But 2026 is the most unique moment in history from AI usage.

Just from my own model projections as all former estimates are likely wrong from extreme AI ramp (eg. DOE/LBNL projections):

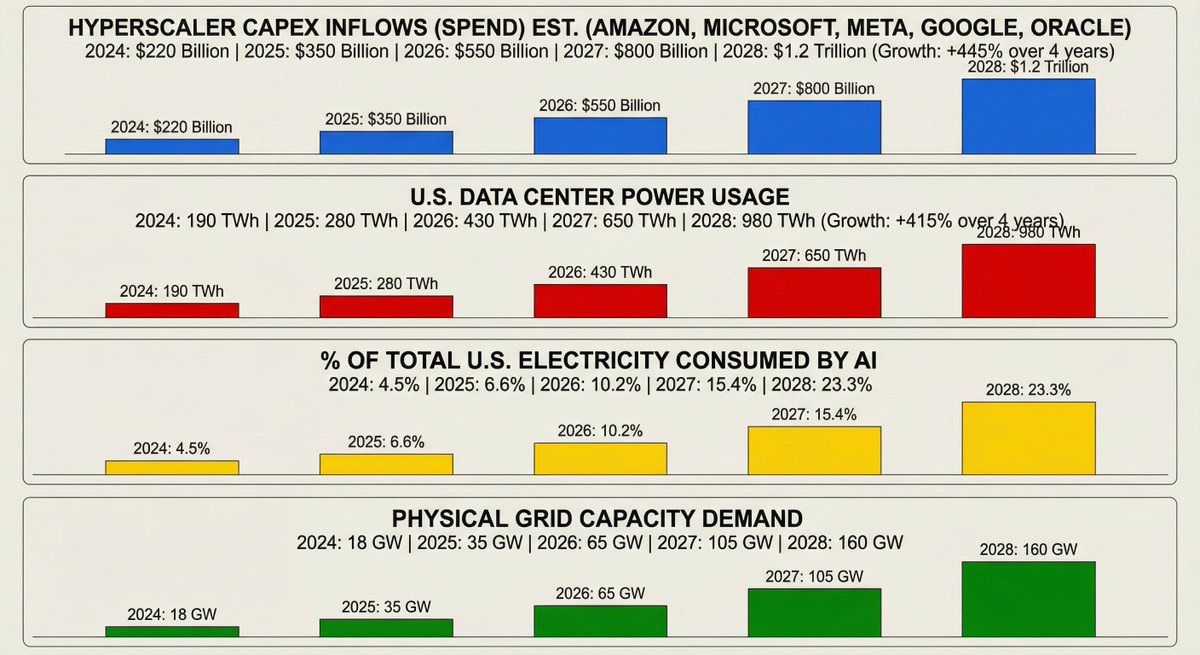

Hyperscaler CapEx Inflows (Spend) - (Amazon, Microsoft, Meta, Google, Oracle) into DCs est:

2024: $220 Billion

2025: $350 Billion

2026: $550 Billion

2027: $800 Billion

2028: $1.2 Trillion (Growth: +445% over 4 years)

U.S. Data Center Power Usage:

2024: 190 TWh

2025: 280 TWh

2026: 430 TWh

2027: 650 TWh

2028: 980 TWh (Growth: +415% over 4 years)

% of Total U.S. Electricity Consumed by AI:

2024: 4.5% of the U.S. grid

2025: 6.6%

2026: 8.2-10.2%

2027: 13.4-15.4%

2028: 21.3-23.3%

Lawrence Berkeley National Laboratory and the Department of Energy seem off by AI usage (they're projecting ~12% by 2028)

Physical Grid Capacity Demand:

2024: 18 GW

2025: 35 GW

2026: 65 GW

2027: 105 GW

2028: 160 GW

Basically you can just see 2026 into 2028 being the inflection point whereas 2024-2025 where slower years on the ramp up.

Then there's the "Desperation Premium" for independent companies. Because grid capacity is sold out, tech giants are paying massive premiums to utilities to cut the line. eg. PJM Interconnection (Virginia "Data Center Alley"), capacity prices spiked from $28.92 per MW-day in 2024 to an unfathomable $329.17 per MW-day for 2026/2027.

$VST or Constellation are a large weighting in the ETF as independent power producers.

Across the board, you can see the extreme ramp from 2026 (now) into 2028 compared to previous years, alongside extreme capex going into building the infrastructure.

2026 is the first time in modern market history that every single thing is firing at the same time for the boring grid/power sector with AI as the biggest tailwind.

And as Elon quotes it: "Billions of dollars of the most advanced hardware. Sitting dark. Not because the chips won't work. Because there's not enough electricity to run on them".

Again 2026 is an absolute historical anomaly due to AI and MMs have priced in historical IV (extremely flat ~14%-16%) for OTM calls.

We're seeing an explosion in AI inference (beyond previous measurements) as well as training (per OpenAI report today).

So the most boring sector on earth (power/grid), might just be the start of a major rally due to hyperscaler/gov spend into grid improvements -> extreme power consumption from AI inference/training -> rate cuts and others.

This is just my personal thesis, options come with risk and magnifies downside too. These are also my own projections, no certainty if they will exceed or be lower than them.

But basically:

2026 is an absolute historical anomaly.

New bottleneck in the US is power.

There's extreme demand from AI, extreme capex, rate cuts:

$XLU looks like the best trade for exposure.

Time will tell if this is right or not.

Serenity@aleabitoreddit

Trade Idea: Long OTM $XLU leaps (2 years, Dec 2027/Jan 2028). This feels like once-a-generation long due to AI. XLU has concentration in $VST / $CEG power companies. Two reasons: 1. Paradigm shift due to AI DC electricity usage. 2. Low option IV (~14%) based on historical averages (flat since 2000s). AI power usage is astronomical. This cannot be understated. Never before in history have DCs use up this much GWs in power, especially when they require outputs of nuclear reactors for training LLMs. This forces $META, $AMZN, $GOOGL, and others to sign multi-year agreements to consume as much power as possible. And yet they still don't have enough. -> So, trillions would likely be poured into grid upgrades. Usually interest rates hurt the sector but we're going into more rate cuts, so it makes the sector a much better long. OpenAI's letter to congress pleaded the US to invest in energy as well to compete vs. China. So, this feels like a once-a-decade type long due to: - paradigm shift eating up any available power from AI - trillions in grid upgrades to compete vs. China - rate cuts. And low IV pricing from historical averages.

English

@jakebrowatzke Very tough, how are you dealing with that mentally?

English

I have lost $7M in 2 months.

I have never ever spent $1M in my entire 30 year life.

English