@ALikhodedov Thanks, just right amount of details for me to understand

English

Andriy Che

2K posts

$IDYA PFS curves from Optimum-02

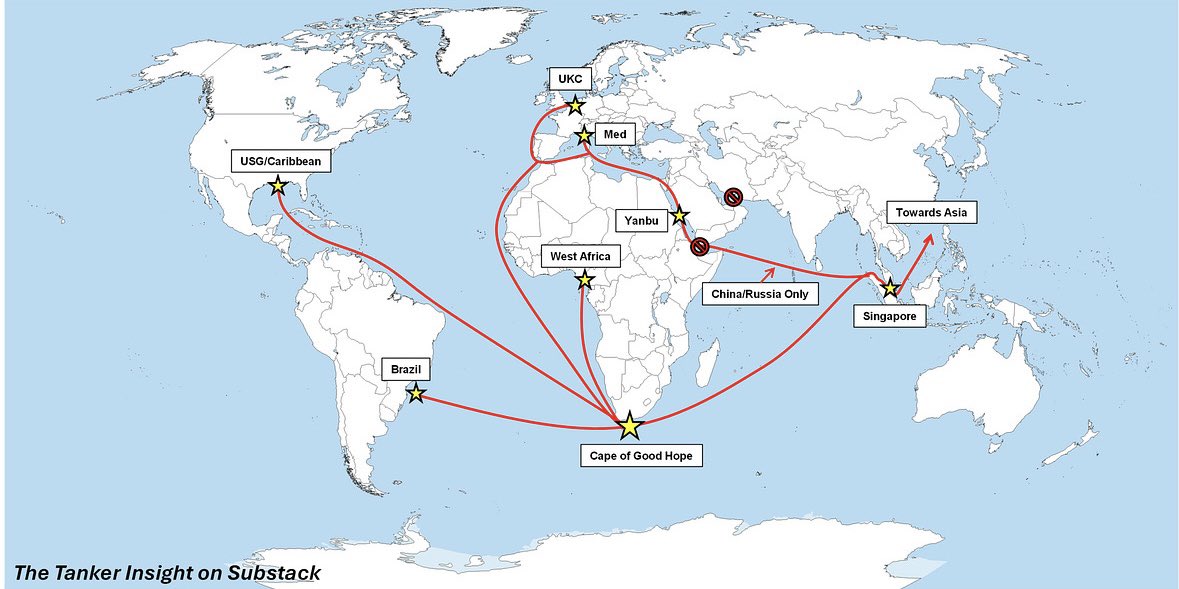

A boat with around a dozen armed men onboard just attacked a cargo vessel near the Bab al-Mandeb Strait in the Red Sea. The attack failed as they couldn’t board the ship. Looks like the Houthis are starting attacks to close the Strait and the route through the Suez Canal.

Apr 9 North Sea Platts window Total bid for Apr 30 - May 4 WTI Midland cargo at Dated Brent plus $22.35 CIF Rotterdam, equated to Dated Brent plus $19.25 on a FOB basis. And Trafigura bid for May 6-10 WTI Midland cargo at Dated Brent plus $21.60 CIF Rotterdam. Mercuria bid for May 5-9 WTI Midland cargo at Dated Brent plus $21.10 CIF Rotterdam. Gunvor bid for Apr 29 - May 1 Forties cargo at Dated Brent plus $21.85 FOB, while Total bid for Apr 28- May 8 Forties cargo at Dated Brent plus $21.00 FOB and Shell bid for May 6-8 Forties cargo at Dated Brent plus $20.25 FOB. Trafigura bid for Apr 21-23 Oseberg cargo at Dated Brent plus $21.65 FOB, while Total bid for Oseberg cargo Apr 26-28 at Dated Brent plus $21.15 FOB. Gunvor bid for May 7-9 Ekofisk cargo at Dated Brent plus $22.80 FOB and for Apr 24-26 Ekofisk cargo at Dated Brent plus $21.95 FOB. Trafigura bid for April 29 - May 1 Troll cargo at Dated Brent plus $23.55 FOB. It’s all bids. Just look at the physical players trying to grab crude even at these terrifying premiums. WAF crude diffs have also surged past Dated Brent+$10. It’s clear they don’t love peace! This definitely calls for a roar on Truth Social! #oott #iran

The physical market cares not for stories of peace. It only cares about delivery. Brent crude has fallen 14/bbl but phys is unchanged

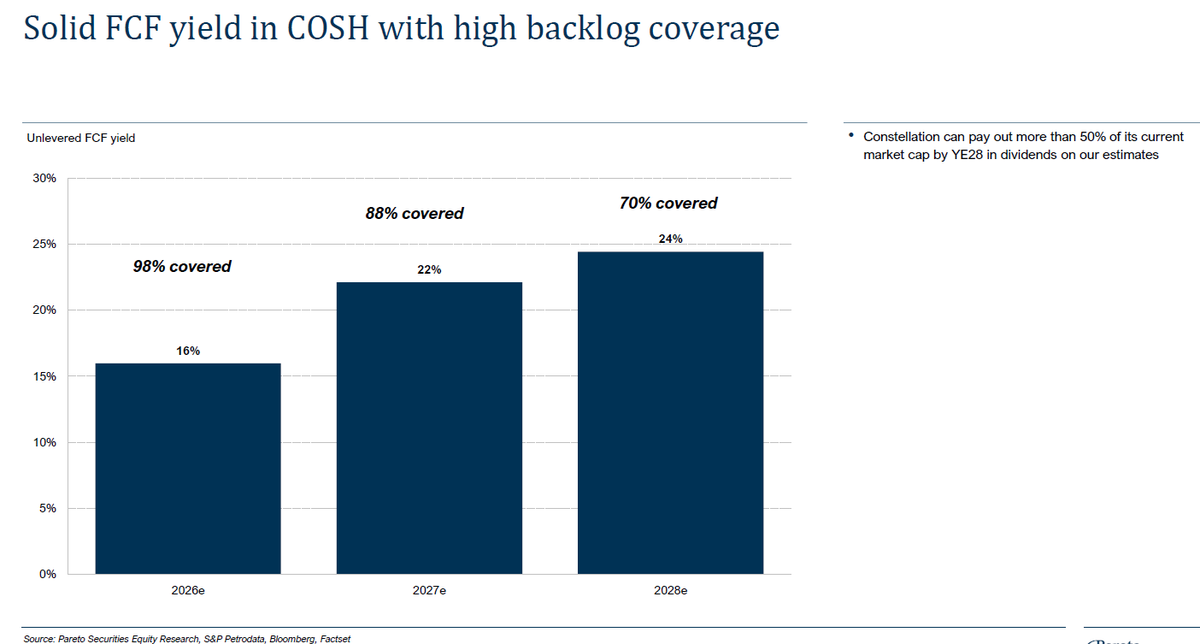

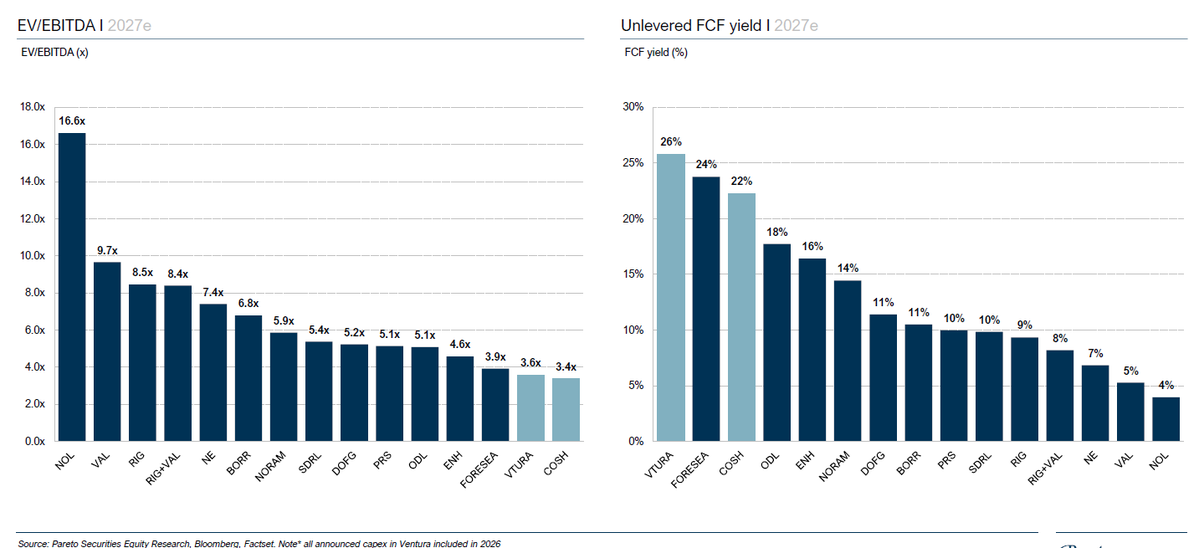

As anticipated, Constellation Oil Services has secured ~10 years of combined contract extensions with Petrobras across three rigs (Brava Star, Gold Star, Alpha Star), adding ~$1.1B in net backlog through 2030. * Backlog visibility is the key takeaway, removing near-term rollover risk across all three rigs through at least 2028–2030. * Blend-and-extend implies day rate concessions; however, I still expect the company to distribute close to half of its current market capitalization as dividends over the next three years. * No transition gaps across extensions, eliminating idle time risk and supporting full utilization. * Brava Star’s MPD upgrade, combined with its role in the Búzios field, suggests Petrobras is further embedding COSH into its pre-salt development program, increasing switching costs. * The offshore oil sector was already benefiting from structural tailwinds prior to the war; these have now been reinforced, and if there is a clear regional winner, it is Brazil. Given COSH’s illiquidity on Euronext Growth Oslo, the market may not reprice this immediately; Tuesday’s open could still provide an attractive entry point. $COSH.OL