ทวีตที่ปักหมุด

I RAISE MY PRICE TARGET FOR CLOVER HEALTH $CLOV TO $7.25

English

AL STOCK TRADES

5.9K posts

@ALSTOCKTRADES

Wall Street-Level Analytics. Retail Empowerment Through Data & Education. Not Financial Advice.

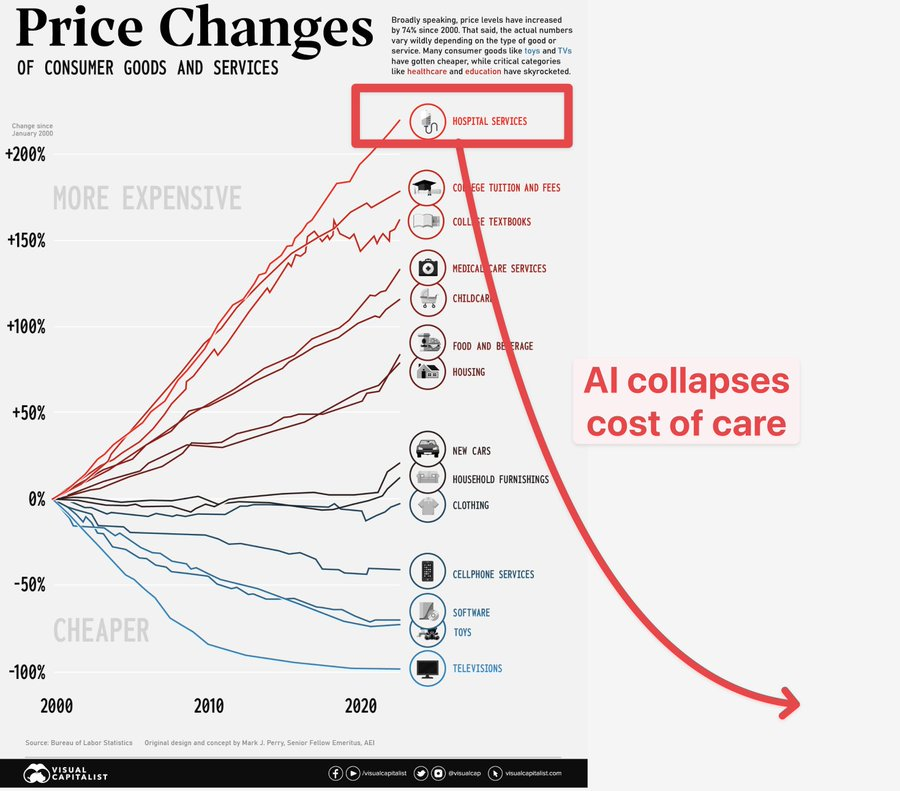

Chamath’s framing is clean but it’s missing a third door that nobody wants to talk about. The real story IGV is telling you isn’t just about whether AI replaces software or doesn’t. It’s about the death of the asset-light business model itself. For a decade the market rewarded companies that scaled on code and subscriptions with almost zero marginal cost per user. That entire thesis just got inverted. Every SaaS company bolting AI into their product is now eating 20 to 40 cents of variable compute cost on every dollar of revenue where they used to eat almost nothing. GitHub Copilot was literally losing Microsoft $20 to $80 per user per month at a $10 price point. That’s not a software margin profile, that’s a hardware margin profile wearing a software costume. So what you’re actually watching in that IGV chart isn’t just an AI disruption repricing, it’s the entire sector morphing from asset-light into something that looks a lot more like an industrial business, right at the exact moment the market is realizing it. Goldman figured this out in February and quietly launched their HALO framework, Heavy Assets Low Obsolescence, essentially telling clients that the companies who own atoms, not just bits, are the new defensible compounders. Their pair trade basket has outperformed the S&P software index by nearly 80 percentage points over the past year. But here’s what even Goldman isn’t saying out loud yet. If AI compresses the margin structure of subscription software permanently, and it forces every vendor into usage-based or outcome-based pricing just to survive, then the terminal value assumptions baked into every DCF on every name in that ETF are fundamentally broken. You’re not just looking at multiple compression. You’re looking at the end of the SaaS valuation framework as a category. The P/E on the software sector went from 51x a year ago to 27x today while earnings estimates barely moved. That tells you the market isn’t discounting a bad quarter, it’s discounting a permanent structural change in how these businesses make money. Meanwhile the companies that actually own scarce physical infrastructure, think data centers, power generation, copper, cooling systems, the cloud hyperscalers themselves on the capex side, those are the ones whose replacement cost goes up as AI scales, not down. The scarcity used to be code. Now it’s electricity and silicon. Everyone’s arguing about which software names survive the AI wave. The bigger question is whether “software company” even remains a distinct asset class when every one of them is forced to become a compute-intensive industrial operation just to keep the lights on.

You have two choices: 1. This is the beginning of the end of the AI replacement cycle. Everything up until now was false alarms and mis/disinformation. You can start to scale back into these companies because, once the noise subsides, these companies are durable and will be around roughly in the same or better position in 10 years. 2. This is the beginning of the beginning of the AI replacement cycle. Customer churn slowly ticks up. NDR slowly ticks down, RPO begins to be discounted - initially by a little, then by a lot. SBC gets minimized, FCF gets maximized. Valuations become exercised in seeing which assumptions are reliable and which are unreliable - all roads lead to more vol an a general downward trend on price and multiples. Good luck to all the players.

Congratulations to the most important AI company in healthcare (shhhh don't tell anyone :-) Foundation AI model companies with no proprietary data and no true feedback loop will be revealed in a few years to be valued like any other commodity solution.

HealthEx was proud to showcase several demos at the CMS Healthtech ecosystem gathering yesterday in DC. HealthEx supported demos for @AlteraHealth, @CloverHealth, @MEDITECH, @UnitedHealthGrp, and our own demo with @HeyEpic, @NetsmartTech, @CloverHealth, @MedAllies, @Kno2, @Clear, and @claudeai. HealthEx is also proud to be one of teams meeting MVP requirements for the KillTheClipboard category, and to be one of the first apps featured in the Medicare App Library. The important work we are doing to enable patients to access and share their health records, at the moments that matter, wouldn't be possible without the collaborators here that span the breadth of healthcare. Thank you also to @CMSGov for convening collaborators across the public and private sector, all working together to empower patients in their health journeys!

Happening now! Join CMS virtually for the Health Technology Ecosystem: Live! First Wave Launch. Innovators from across health care will be showcasing the Minimum Viable Product of their new health tech. Don't miss the opportunity to get a first look at the cutting-edge apps designed to transform healthcare delivery. Join now: go.cms.gov/4c9Kgog

Providers should be able to spend their time delivering high quality care, not doing paperwork or hunting down patient’s health history from other providers. The Health Tech Ecosystem is focused on helping you get the right information when you need it. Help CMS shape the future of interconnected care. Take the pledge today: go.cms.gov/4sYbK7j

Honored to demo at the @CMSGov Health Tech Ecosystem: Live! First Wave Launch this Thursday. Two real patients. Two new capabilities: the first payer data via TEFCA IAS, and Smart Health Links for seamless record sharing. We signed the Kill the Clipboard and Conversational AI pledges - and we're backing them up. With @CloverHealth @counterparthlth @HeyEpic @Clear @Kno2 @NetsmartTech @AnthropicAI #HealthTech #TEFCA #CMS #DigitalHealth

Healthcare AI just showed up at the Webbys. 🏆 The Clover Health Broker Assistant is a 2026 @TheWebbyAwards nominee in AI – Customer Experience or CRM. We built it to take the complexity out of Medicare Advantage for the brokers on the front lines helping people find the right plan for them. Voting is open through April 16, every vote counts and we'd appreciate your support. 👉 wbby.co/58831N

A really important additional reason for your parent or grandparent (or great grandparent) to consider Clover as their insurer