AlwayzApin

3.1K posts

@michaelsikand USV technologies develop really quickly, no arguing here. But realtime streaming of such data volumes is probably hard to achieve in a warzone? Also mines can hit USV…

P.S. Sonar cannot distinguish between mines or seabed features. Data needs processing and analysis first.

English

This is insane.

We always talk about $KRKNF's tech in UUVs. But they just proved they can run their KATFISH mine hunter on USVs, fully remotely.

A USV is an unmanned surface vessel aka a robot boat. KATFISH is Kraken's towed sonar that gets dragged behind it, scanning the seafloor for mines at 3cm resolution. That data streams live to operators sitting safely onshore.

This matters because Iran is actively laying mines in the Strait of Hormuz. Clearing those mines traditionally meant putting sailors directly in the minefield aboard a minesweeper ship.

This system puts zero humans at risk and marks two successful USV demos in five months across a Royal Navy and now Turkish vessel.

When is the @Saronic collab coming?

English

@CatSE___ApeX___ Is this a sign that the carbon fiber issues have been resolved?

English

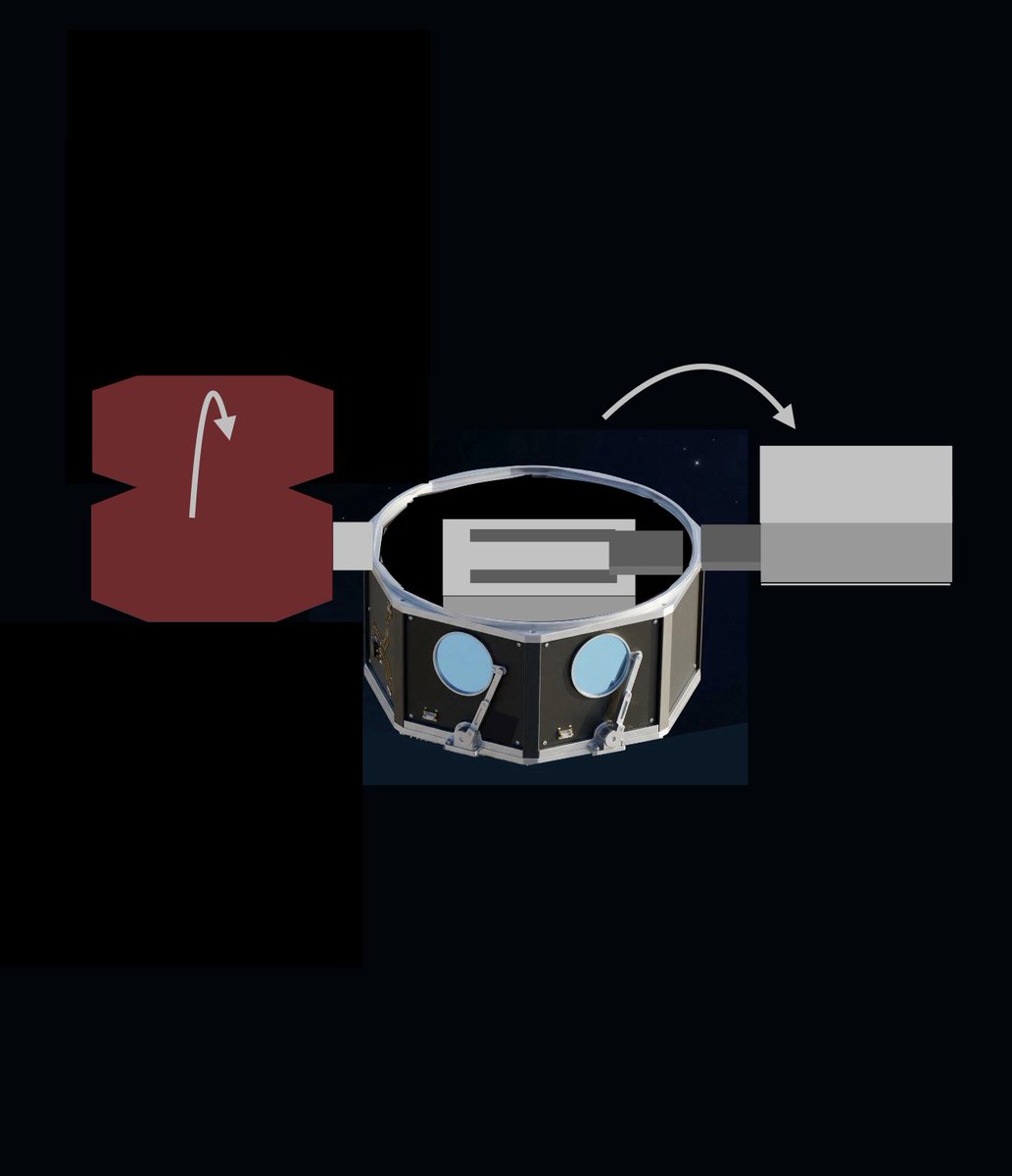

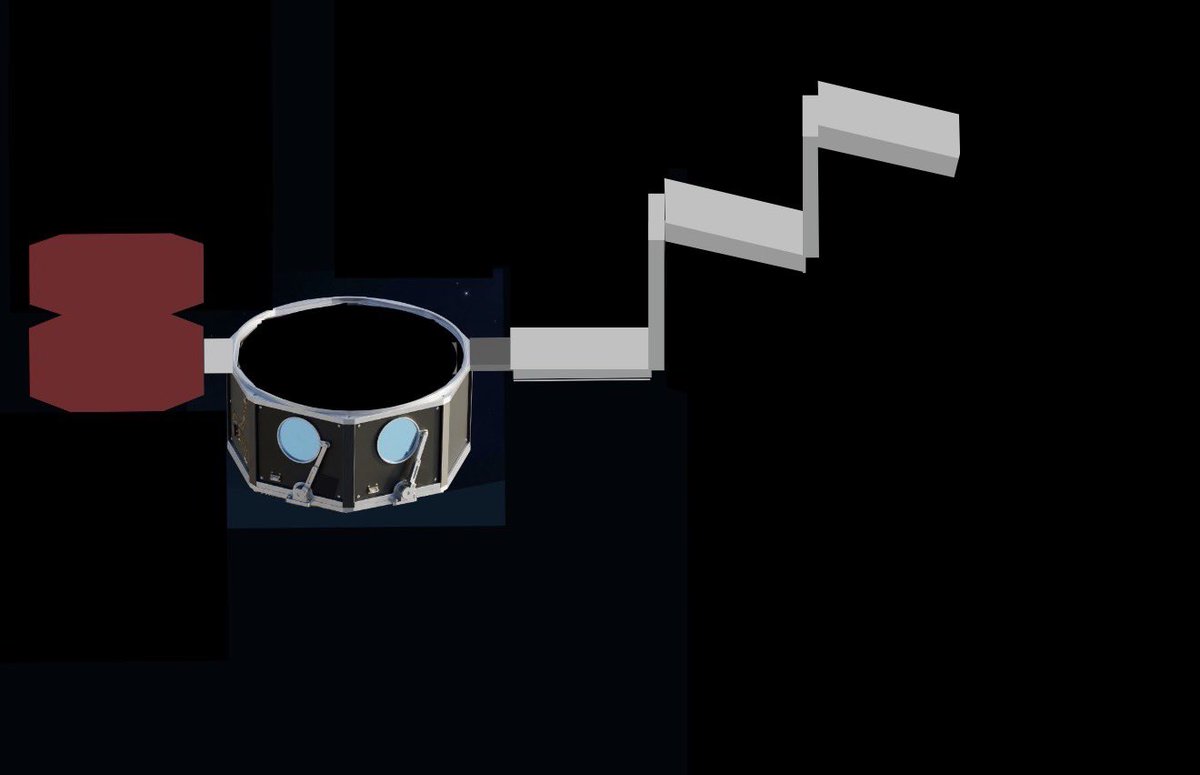

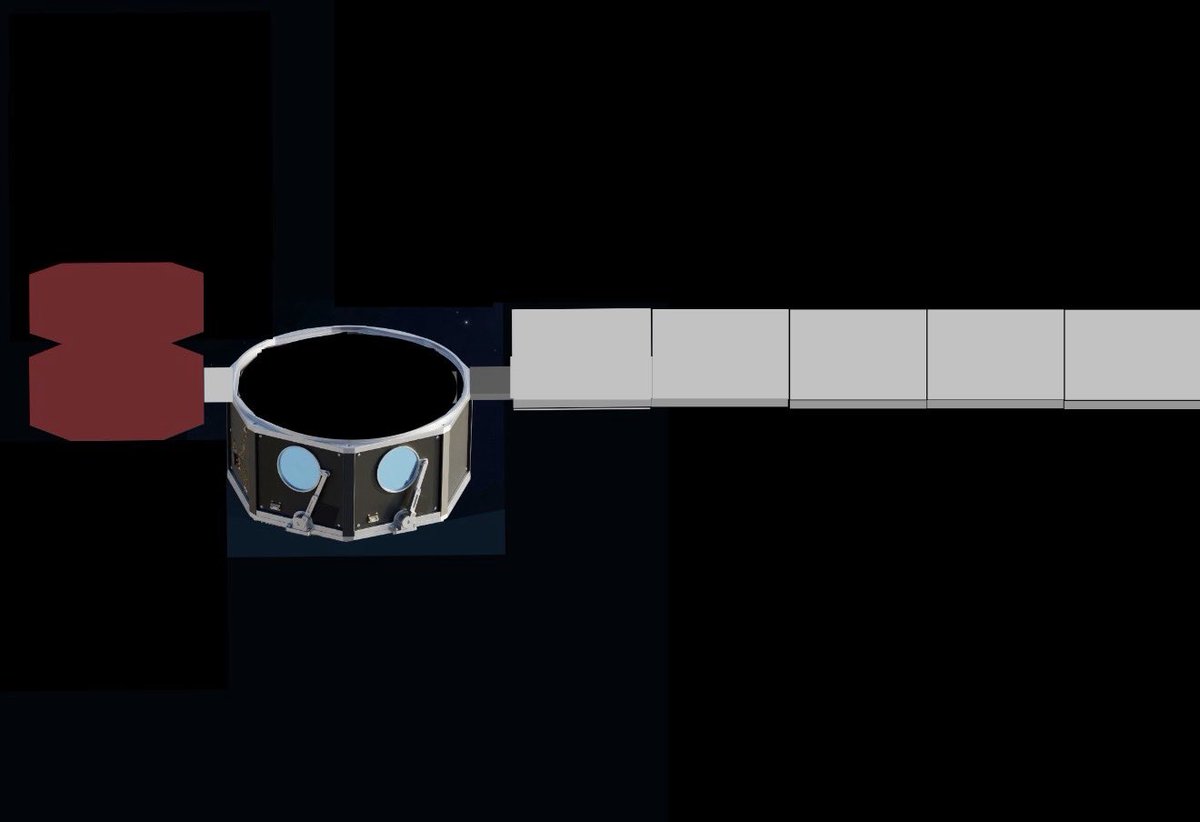

$ASTS the inside of the top of an AST Bluebird satellite.

It is where the phased array (grey cube in my sketch) is stowed during launch. Here we see the bus flipped upside down for mating of the array.

Steve@Steved24661

$ASTS: Oh just a quaint little visit to Midland from Meta. Probably nothing.

English

It’s funny because it’s true.

Headed to Indy tonight.

Go Blue!

Swanky Wolverine@swankywolverine

Michigan vs. Arizona recap

English

@Steved24661 @CatSE___ApeX___ The real question is does $ASTS have jurisdiction to file the suit in Beaumont, Texas?

English

$ASTS: This is a solid summary of the AST / Ligado v. Viasat / Iridium drama. I agree with most of it. With that said, I believe we should be watching for a lawsuit against Iridium, not Viasat.

There are really two reasons for this conclusion.

First, AST really doesn't want the Ligado deal to blow up. They want and arguably need that spectrum at this point. Because of this, I think AST is incentivized to put up with as much of Viasat's BS that they can handle.

Second, and on a more technical legal note, any lawsuit against Viasat will be limited to contractual damages, which, generally speaking, are more limited than tort damages.

That's where Iridium comes in. IF discovery ends up showing collusion between Viasat and Iridium, AST could conceivably sue Iridium (not Viasat) for tortious interference with contract / business expectancy. This would unlock all sorts of potential damages, including punitive damages. As the judge said yesterday, the damages have the potential to be very large.

That said, we are a long way from all of this. And for this theory to be viable at all, it requires Iridium and Viasat to have made the colossally stupid decision to collude against AST / Ligado. But if they did, look out. Things could get spicy, and its possible $ASTS could be an eventual beneficiary.

keaze@keyesmn

$ASTS Wanted to comment on the latest Viasat/Inmarsat case filings and try to provide a high level cliff notes. The filing and link that many are sharing is not the Judge’s order - it’s Ligado and AST providing a complaint that Viasat didn’t do what they said they would do. What some missed (myself included) - but was attended by some (including @thekookreport) - was the hearing with the Bankruptcy judge that was held yesterday. In that hearing the judge agreed that it appears on its face that what Ligado and AST claim is true - Viasat failed to live up to their end of the contract, and as a result they have materially damaged AST and Ligado. You may recall that in their Mediated Agreement Viasat promised to provide affirmative support for the AST transaction to the FCC. They failed to do so. It’s actually a very clear cut case of breach of contract. The judge held the payment in escrow assuming that it could be used if damages are awarded - after discovery and further court proceedings. So there won’t be a quick win by any means, but it looks like there will be some sort of win. So then what of damages? Very unlikely we are looking at punitive damages, much more likely that we get expectation damages - or more simply put, what did we miss out on by the delays brought on by the Viasat objection, and what of the risks created by their opposition? So this could include additional fees for lawyers brought on by the delays, but experts will have to opine about the risk of non-approval and opening the door to other objectors - and that could get large, up to and perhaps over the $535M. How much is it worth to have a clear path to FCC approval? Only experts will be able to convince a judge. Judges will want to see proof of quantified damages - which is a high bar, an Viasat will hope that an FCC approval will remove the risk that they will owe a lot in the way of damages by saying, “see, you got the approval, no big deal.” What might get interesting is discovery. If you hav something crazy like Viasat an Iridium agreeing to both contest the application, then you have conspiracy and collusion and then tortious interference opens up another avenue for damages - then perhaps you get to punitive damages and get a multiplier thrown in there. Discovery will take time, this won’t be quick - but at the very least they will likely be clawing back some of the cost of the acquisition and perhaps a whole lot more! Very stupid gamesmanship on the part of Viasat. I hope to see AST really press this.

English

The Army has suspended the aircrew of the Apache helicopters that flew near Kid Rock's house - NBC

KidRock@KidRock

This is a level of respect that shit for brains Governor of California will never know. God Bless America and all those who have made the ultimate sacrifice to defend her. 🇺🇸 🙏

English

Today $ASTS received a monster off-balance sheet litigation asset from a US District Judge. Ligado is moving forward, and so too is a large damages lawsuit against $VSAT. $VSAT had blatantly violated a confirmed bankruptcy plan, since cured after getting smacked by multiple courts. Today we heard the judge rule in favor of $ASTS AND specifically hold back $100MM, which is viewed as conservative, for potential future damages in favor of $ASTS.

English

One of my maxims in life: never ever trust a man who wears a bow-tie.

Elon Musk@elonmusk

Probability of me getting a fair trial if this is how the judge dresses is 0.0%

English

@TheIranWatcher wouldn't it have been more effective to poison the food?

English

🚨 At least 5 dead in suspected “pager-style” attack using canned food!

Reports claim explosive devices were hidden inside canned food distributed to Basij and security forces in Fars Province, detonating upon opening.

At least 5 killed, multiple injured, and distribution has reportedly been halted with warnings issued by the Islamic Republic of Iran.

This follows the same pattern as past “pager-style” attacks where everyday items are turned into weapons.

Did Israel carry this out like the pager attacks in Lebanon, and could there be more covert operations like this ahead?

English

@Aviation_Intel Would EMP take out generators inside BM granite mountain hideouts?

English

My liberal 4.0 daughter just got into her dream school. 7% acceptance rate. Absolutely unreal. Insanely proud of her.

Now do I rob a bank, push a cheaper school, put her in student loan debt, or dust off the old captain’s hardhat and head back to sea?

Decisions. Decisions.

English

Look what I found today filed to the ITU for $ASTS from the FCC…. More shells, wonder who these are for?

Filings now for up to 543 satellites from the 243. Adding 3 new shells.

C🅰️tSE@CatSE___ApeX___

Credit for find @tottaway22 itu.int/ITU-R/space/as… It’s an update to USASAT-NGSO-20 effectively doubling the constellation size 2/

English

@SpaceInvestor_D It’s also because it’s their last year being #1 at commercial direct-to-device service. @AST_SpaceMobile takes the crown in 2027.

English

Why a SpaceX IPO in 2026?

It’s not about liquidity for employees or early investors, and it’s not because SpaceX needs cash to survive.

The goal is to raise an enormous war chest at peak valuation and deploy it into orbital AI infrastructure before anyone else can, building a massive moat.

If reports are even close, the raise would give SpaceX the firepower to start building massive AI data centers in orbit at speed, while competition is still asleep.

This is about building the next industrial frontier.

At scale. First.

Space Investor@SpaceInvestor_D

👀

English

@DeItaone If they are responding through mediators, then that is a prime definition of negotiation.

English

IRAN'S ARAQCHI SAYS EXCHANGE OF MESSAGES VIA MEDIATORS "DOES NOT MEAN NEGOTIATION" WITH THE U.S.

English

English

@biancoresearch My Hawks are going to take out the Huskers tomorrow, that’s all that matters. Don’t really disagree with you re Michigan.😄

English

@BTCsupernova The job of the Big 10 is to lose, and get arrested ... see Michigan Football

English

Six of the sweet 16 teams are Big 10 teams.

What is the national response to this?

To scream college sports are broken and propose legislation to fix it.

😆

x.com/PeteNakos/stat…

Jim Bianco@biancoresearch

The Sweet 16 will be all power-conference schools: Big Ten, SEC, ACC, Big 12, and Big East. Since the field expanded to 64 in 1985, it has only happened twice: last year and this year. This year, we can now say it with three games left to finish, as they feature power conference schools playing each other. NIL + the transfer portal are hollowing out March Madness. The old Cinderella model is dying because mid-majors can’t keep the veteran cores that used to make these runs. Once those players establish themselves, they jump to bigger stages and bigger money at power-conference schools. The only double-digit seed left is No. 11 Texas. One of the richest athletic departments in college sports is not what comes to mind when you think “Cinderella.” A bracket with Siena, Miami (Ohio), Saint Louis, and/or High Point still alive would have felt a lot more like March Madness.

English

In early 2022, a buddy of mine was an LP in one of the big crypto funds at the time. This was before things really blew up but the cracks were already starting to show

The GP of the fund reached out to my friend one day, asking for more capital at a 15% guaranteed return. After giving it some thought, my friend called back the next day and requested a full redemption. That fund ended up going belly up later that year

Anyways, I think about that story a lot

English

man's got a point

dcnh@davec_NH

Put ICE in every Hospital ER, and watch your Healthcare cost drop.

English

@AST_SpaceMobile This belongs here.

x.com/catse___apex__…

C🅰️tSE@CatSE___ApeX___

Maybe You don’t see it clearly now. But this is a model for the world. DoD wants TAK type connectivity everywhere. It goes for First Responders, Customs and Coast Guard. It goes for the intelligence services. It goes hard. It requires bent-pipe for sovereignty and it will see spectrum allocated to it. Opening the door to new markets globally. Europe, Asia, USA, Latin America, etcetera. Singapore is early. As is FirstNet. More will come. Much more.

English

DSTA AND AST SPACEMOBILE DEEPEN SPACE-BASED CELLULAR BROADBAND PARTNERSHIP

dsta.gov.sg/docs/default-s…

English

@LostFundamental @Gunwalls1 MNOs will end up just including it as part of all premium packages. Because they have to to compete with other MNOs. Basically becomes a standard expectation by customer and MNO adds it in to maintain market share. There will be billions of end customers that have the service.

English

@Gunwalls1 Semantics but you are right. Please show me a case where MNOs succesfully upsold anything? They tried with Spotify, Netflix etc. products of actual use to people. This product has 0 value to 99% of their customers in high ARPU countries that can actually afford the $10 extra.

English

$ASTS - A good example of top-down analysis (CK Capital) unhinged from reality. In a world where mobile ARPU is $10/month across 7bn mobile subs, $ASTS will quickly convert 1bn of those to spend another $10/month for a service 99% of them don't need....

x.com/LostFundamenta…

CK Capital@CKCapitalxx

$ASTS has a path to becoming a trillion dollar company and the math isn’t complicated. Let me show you exactly how it gets there. Start with Starlink as the benchmark. Starlink took 5 years, over 10,000 satellites, and tens of billions in capital expenditure to reach 10 million subscribers and roughly $10 billion in annual revenue. SpaceX is now targeting a $1.75 trillion IPO valuation with Starlink’s implied value sitting around $1.17 trillion on that subscriber base. 10 million subscribers. $10 billion revenue. $1.17 trillion implied value. $ASTS is targeting 5 billion mobile subscribers globally. Not 10 million. 5 billion. And the business model is structurally superior to Starlink in every way that matters for scale. Starlink competes with carriers. They built their own hardware, their own dish, their own subscriber acquisition funnel. Every customer has to buy a $600 terminal, cancel their existing provider, and switch to a new service. Customer acquisition is expensive and friction is high. That is why after 5 years and 10,000 satellites they have 10 million subscribers. $ASTS does not compete with carriers. They partner with them. AT&T, Verizon, Vodafone, Rakuten, Orange, TELUS, and 50+ operators worldwide have already signed agreements. Those carriers collectively cover 3 billion existing subscribers whose phones are already hardware compatible. No new device. No new plan. No new anything. The carrier offers satellite coverage as a simple add-on and the existing customer base opts in. Zero customer acquisition cost on $ASTS’s side. Starlink charges $120 per month per residential customer. $ASTS operates on a wholesale model where carriers pay per subscriber. A $5 per month add-on to an existing carrier plan is not a stretch. Carriers charge $15 to $30 per month for international roaming today. A dead zone coverage add-on in rural America, at sea, or in the air is a premium feature people will pay for without thinking twice. Now run the math. 1 billion subscribers at $5 per month is $60 billion in annual revenue. That is 20% penetration of the 5 billion subscriber target. That is 33% penetration of the 3 billion already on partner carrier networks. Starlink is valued at $1.17 trillion on $10 billion in revenue. That is roughly a 117x revenue multiple. $ASTS generating $60 billion at a fraction of that multiple tells you everything you need to know. At 15x revenue on $60 billion that is a $900 billion market cap. At 20x that is $1.2 trillion. At Starlink’s implied multiple it is multiples beyond that. But let’s stay conservative. Even at 10x revenue on $60 billion that is a $600 billion market cap from a $35 billion market cap today. That is 17x from here on a scenario that requires 20% penetration of an addressable market where the distribution is already built and the hardware is already in billions of pockets. Now look at this realistic time line. BlueBird 6 is already in orbit. The largest commercial communications array ever deployed in LEO, exceeding 120 Mbps peak data speeds. Commercial service activating this year across the US, UK, Japan, and Canada. $3.9 billion in cash on the balance sheet fully funding the constellation buildout. Zero dilution risk on the launch campaign. The 2025 revenue was $70.9 million. 2026 guidance is $150 to $200 million as commercial billing starts and government contracts ramp. The revenue line is just starting to move. The subscriber base is not priced in at all. Starlink needed 10,000 satellites and 5 years to get to 10 million subscribers fighting for every single one. $ASTS needs 45 to 60 satellites and already has 3 billion potential subscribers sitting in their partners’ existing customer bases waiting for the switch to flip. The constellation is almost complete. The carriers are signed. The phones are compatible. The revenue is starting. $35 billion market cap. $1 trillion is the destination. The satellites are going up now.

English