@kainvests I think we see north of $4 just based on the $REPL CRL this upcoming week. With that said if we see some solid guidance and Q126 earnings next month I think we could go a bit higher to $6

$IOVA What are your thoughts regarding likelihood of organically getting and staying above $4 next week?

Do you expect any news in the following two weeks or are you betting on these occurring during the 26Q1 ER?

$IOVA Some thoughts on guidance for 2026, and why ATC ramp matters more than any revenue number!

Let's do a recap of how Iovance delivers its value proposition! 🏥

First, what is an ATC?

An Authorized Treatment Center is a hospital or clinic certified to administer a specific cell therapy. Remember, they can't just order it as if it were a pill, they need:

1. Specialised staff training

2. Dedicated manufacturing slots

3. Surgical teams (specialised in Amtagvi)

4. Financial clearance workflows

5. Pharmacy protocols

Getting certified is the easy part. Getting good at it and roll it out takes time!

Now, every autologous cell therapy - autologous comes from Greek autos meaning "self; so a therapy that comes from the patience (tumour) - follows a similar institutional learning curve:

The documented maturation cycle has 4 phases:

- Phase 1: Activation (Months 0-6). Centers get certified. Treat 0-1 patients. Every case is a massive internal project. Nothing is routine yet.

- Phase 2: First patient learning (Months 6-18). Centers treat their 1st-3rd patients. Administrative burden per case is enormous. Revenue is slow and lumpy.

- Phase 3: Workflow maturation (Months 18-30). Centres that have treated 3-5 patients develop institutional muscle memory. Referral pathways formalise. Slot utilisation improves. This is where per-center throughput starts climbing!

- Phase 4: Volume inflection (Months 30-42). Centres treating 5+ patients start treating 10-15+. Community referral networks activate. Per-centre throughput jumps non-linearly. Top 20% of centres end up doing ~60-70% of the total volume.

Let's look at Yescarta, CAR-T for lymphoma:

- Month 6: ~60 centers active. Average throughput: 2-3 patients/center/year

- Month 18: ~90 centers. Throughput: 5-7 patients/center/year

- Month 30: Clear bifurcation. ~20 high-volume centers doing 15-25 patients/year. Majority still at 3-5.

- Month 42+: High-volume centers at 30+/year. Community referrals mature.

Year 3 revenue was ~2.8× year 1. Not because they added 2.8× more centers BUT because existing centers got dramatically better at using their capacity.

Now apply this to Iovance:

- Amtagvi was approved February 16, 2024.

- That puts us at approximately month 26 today (April 2026).

According to the documented cycle, Amtagvi is entering Phase 3 Workflow maturation; right now.

The volume inflection (Phase 4) historically arrives around months 30-42. That's late 2026 into 2027.

The current ATC numbers aling with the above: Iovance has 85+ ATCs, BUT as of end of 2025, only ~48 had ever infused a single patient

Only ~11 had treated more than 10 patients

Average throughput: ~5 patients per center per year

87% of centers are still in Phase 1 or 2.

This isn't a failure; this is exactly where Yescarta was at month 26.

The capacity is already there, what we need now is training and positive results that encourage the ATCs to treat more patients!

Now, let's look at the factory: our beautiful iCTC.

It was designed to support 5,000-patient/year design capacity. Do the numbers! It is extremly underutilised; just like the ATCs.

So we don't have a demand problem, we have a maduration challenge that is expected.

Now, to make our lives more interesting, remember that they came in the last Q talking about community ATCs? This is a wildcare that could speed things up substantially!

In CAR-T history, academic centers dominated volume in years 1-2 (~70-75% of patients). The non-linear growth happened when community centers matured; because that's where 60-65% of metastatic melanoma patients are first seen.

Iovance's community ATCs began treating patients in late 2025.

Based on the historical template, they should start showing real throughput improvements in mid to late 2026; with meaningful volume contribution in 2027.

Now, Amtagvi has one unique friction CAR-T didn't have! Surgical resection of the tumor is required before manufacturing can begin. This means every centre needs an operational relationship between:

👩🏻⚕️Medical oncology (who refers the patient)

👨🏼⚕️Surgical oncology (who removes the tumor)

🏭The Iovance manufacturing team

When it all clicks guys, together with the fact that we have NSCLC and TILVANCE-301, what do you think will happen?

Do you think 2026 is the most interesting year for Iovance? Haha, no. 2027 and 2028 are the real deal, the true awakening before its first baby steps.

Now, let's focus on guidance in itself!

If you calculate the mean/average of the analyst covering Iovance, the expectation is $426.7M. (Source: webull.com/news/138217810…)

Now, after 2025's guidance catastrophe - they guided $450-475M, cut to $250-300M and the stock price went to the ground - management are likely to guide conservatively.

We can expect formal guidance in the $350-450 range. Most likely slightly below or above ≈$400.

But, remember, when we read the PR for 26Q1 results and join the ER call, we will be paying close attention to margins, demand and any input on ATCs.

Oh, team, what a jewel we have between our hands and what a privilege it is to watch it grow in real time!

🎙️ Please feel free to challenge, ask and contribute as always. That's the whole point of social media!

$IOVA For anyone drawing parallels to the REPL CRL remember who’s guiding this ship:

• Dr. Raj Puri (Chief Regulatory Officer): 30+ years at the FDA, including nearly two decades leading CBER’s cell and gene therapy division

• Dr. Marc Theoret (SVP, Regulatory Strategy): Former Deputy Director at the Oncology Center of Excellence with deep oncology review experience

This isn’t a team guessing their way through the process they helped build the framework.

Different company, different dataset, and importantly a regulatory team that knows exactly how the FDA thinks and what it expects.

$REPL CRL

$XBI $IOVA readthrough

Did FDA do anything wrong re: the $REPL situation?

I think one can make an argument for it: The initial BLA review team should have never let them submit BLA in the first place given various issues already raised in FDA/REPL communications over the years dating back to as early as 2021 (tho one can also argue that this is also REPL management's responsibility/decision, they decided to take the risk based on the info they had at the time). A similar situation recently happened to $CORT's rilacorilent BLA in Crushing's Syndrome ( non-oncology rare disease) which ended with a CRL. Such mistake may have put REPL in a much worse position today than they otherwise could have.

I remember they still had tons of cash (>$500M) prior to the first BLA/CRL and could have deprioritized the RP1 program (which btw FAILED primary endpoint in a phase 2 randomized trial against anti-PD1 MONOTHERAPY in CSCC, a less aggressive form of skin cancer compared to melanoma, strong sign that RP1 may not add much to anti-PD1 monotherapy), tighten the belt, and used the resources on future gen programs or business development in-licensing activities instead of rushing into a commercial-stage biotech. They lost >1.5 years and >$200M cash between then and now.

Does $REPL's second CRL signal tightening bar at FDA for oncology?

I don't necessarily think so. Based on the information i have, on this particular case, FDA didn't really tighten the bar. Richard Pazdur has been with the FDA for DECADES and is considered the "steady hand" at FDA. The issue is that $REPL's phase1/2 data package is too weak (you would know if you've designed and interpreted an oncology clinical study before). Single-arm accelerated approval pathway in oncology at FDA is still very much alive and open to drug candidates that demonstrate EXCEPTIONAL efficacy profile in a population with NO OPTION available.

Could $IOVA's Amtagvi meet such bar in NSCLC?

With the 26% ORR data disclosed in 2023, i wasn't sure. But with the durable response data disclosed in late 2025 with mDOR NOT REACHED in 2L+ metastatic NSCLC after a median follow-up of >2 YEARS, my confidence increased significantly as it's reminiscent of durable responses seem in Melanoma. $IOVA dropped 7.7% today (in a bad macro backdrop: XBI -1.8%, after yesterday's 15% run up) likely partially due to $REPL CRL readthrough about tightening regulatory environment on innovative drug modalities that relies on single-arm registration study. But i don't think the bar really changed much at FDA in oncology where the regulatory framework is relatively mature/well established. The philosophy/logic behind single-arm AA requirement remain the same.

These are just my immature thoughts reacting to today's event. I could be very wrong and welcome open discussions.

$dgxx $70mil ATM is a reduction of ATM use from what they had before. They had a $200mil ATM now only $70mil. I think they are confident on large institutional funding coming in

I don’t see much movement from current SP until a contract is executed. Shout out to the ones with diamond hands $DGXX will re rate once the deal is executed. Patience will pay off. I’ll continue adding until then 🚀

$DGXX might be quietly cooking something interesting under the radar right now

Let me explain ↓

@Digipower recently changed their LinkedIn location to Houston, TX with no PR or official update (at least none that I’ve seen yet).

That alone is interesting… but it gets better.

This location sits in a major distribution/manufacturing hub, right in the heart of Texas an area seeing some of the largest data center buildouts in the U.S.

So why does this matter?

My take: this could point to USDC scaling production/logistics potentially building and shipping pods ready for deployment at customer sites.

If that’s the case… being in one of the hottest AI infrastructure markets in the country would make a lot of sense.

Does this point to being close to a 90MW colocation deal? They will need a lot of pods!

What do you all think?

@DigipowerX Appreciate all the color you provided as well as your patience with execution! @michelamar3 looking forward to the next 3 years and what’s in store! $DGXX 🚀

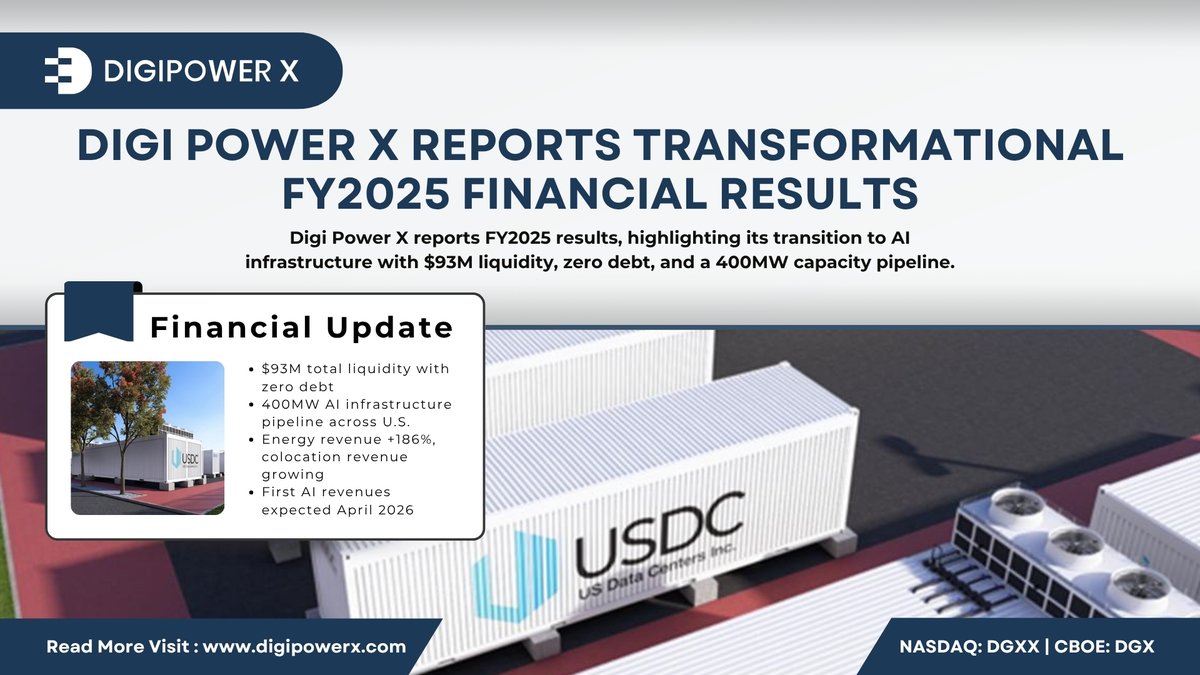

@DigipowerX Inc. (NASDAQ: $DGXX has reported its Fiscal Year 2025 financial results, marking an important step forward in our ongoing transformation.

Over the past year, we have continued to strengthen our foundation — both operationally and strategically — as we transition toward AI infrastructure and high-performance computing.

Key highlights from FY2025:

• Maintained a strong liquidity position to support future growth

• Continued investment in AI data center development

• Advanced our strategy through US Data Centers (USDC)

• Focused on scalable, energy-backed infrastructure

As demand for AI compute accelerates globally, access to power and efficient infrastructure has become more critical than ever.

At Digi Power X, we are building to meet that demand — combining energy assets with next-generation data center solutions.

We believe this positions us well for the next phase of growth as we move into 2026.

Read more - Digi Power X Inc. (NASDAQ: DGXX has reported its Fiscal Year 2025 financial results, marking an important step forward in our ongoing transformation.

$DGXX

#digipowerx#dgxx#ai#datacenters#infrastructure#energy#hpc

$DGXX This will sound obvious, but the longer we do not dump, the more peeps will step up. All the day traders are just waiting for the dump, but when it doesn't come, they get nervous.

$2.25 today perhaps?

As well as this $150 per kW per month under a long-term colocation agreement, 90 megawatts of capacity is projected to generate approximately $162 million annualized.

Combined, these two segments represent a projected annualized run-rate of up to approximately $282 million $DGXX

What type of valuation does $DGXX get on this if executed (10MW / ~4,000 GPUs): Priced at $3.50 per GPU-hour under a year-to-year customer agreement, and operating at approximately 98% utilization, the GPU fleet is projected to generate approximately $120 million annualized

With $DGXX earnings coming up after hours today. I am putting together a group chat for the community to discuss all things Digi. Leave a comment and shoot me a DM if you’d like to join!

Imagine you had to choose your life at age 40:

Option A:

Single. No kids.

$50M net worth.

850 credit score.

Private jet.

Option B:

Married. 2 kids.

$3M net worth.

Drive a Toyota.

10 BTC in cold storage.

500 credit score.

Fly Southwest.

Be honest, which life are you choosing?