Tut C🅰️pital@kingtutcap

$VELO: WTF is going on?

The price action over the past two weeks has been quite weird so I've been trying my best to wrap my head around it.

Unless something severely bad isn't public yet, it does seem mostly due to the insanely high short interest (anywhere from 25-50%) + PIPE overhang rather than fundamental business issues. When you zoom out, the company is actually getting deeply entrenched into defense and space additive manufacturing, both of which are experiencing supercycles.

From a financial standpoint...

Velo ended Q3 with roughly $11M in cash. Then in December they did a $10M equipment sale + $28M net proceeds from PIPE. Sitting at around $50M in cash by end of year.

Their cash burn is around $9-10M per Q which gives them multiple quarters of runway without even assuming big revenue jumps (which is happening). Most of their debt is also pushed to 2027 (~$20M), with only a small portion due in 2026 (~$5.5M).

Yes, they are not swimming in cash but they're not on life support either. They have time to execute. The company is guiding for EBITDA profitability in H1 2026.

Will they raise again eventually? Probably. That's normal for scaling and keeping up with the high demand. The difference is raising to expand vs raising to survive. Right now it looks more like expansion. And to be frank, expanding the float is actually good to allow more institutions to jump in and reduce the volatility/crackhead behavior that the stock always experiences.

From a business standpoint...

Velo isn't just selling printers like they used to pre-2026. They're getting qualified inside defense and aerospace workflows. Once a company is qualified to produce parts for military or space programs, they don't get swapped out easily. It tends to lead to repeat orders and multi-year production.

Just take a look at recent wins over the last 2 months.

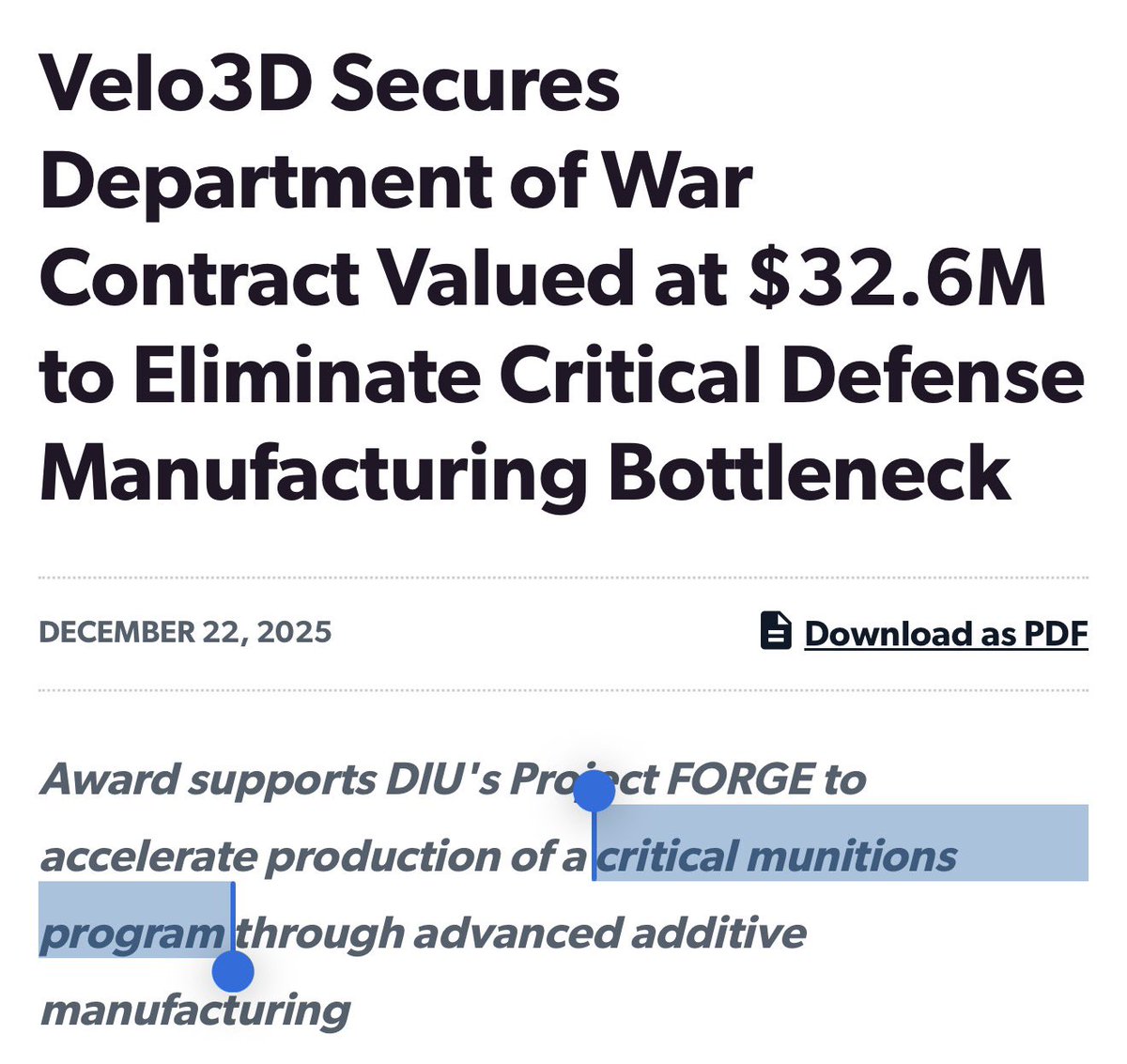

1) DIU / Project FORGE — $32.6M OTA contract (Dec 22, 2025)

Velo3D announced an OTA contract valued at $32.6M supporting DIU’s Project FORGE tied to a “major weapon system program of record.”

2) U.S. Army GVSC — CRADA + then qualification

Jan 13, 2026: CRADA with U.S. Army DEVCOM GVSC to develop/qualify AM parts for ground vehicles and military systems.

Feb 10, 2026: Velo3D said it was selected as the first qualified AM vendor for U.S. Army ground vehicles (per their release).

3) Feb 17, 2026: $11.5M multi-year full-rate production (Defense prime)

Velo3D announced a $11.5M multi-year full-rate production Rapid Production Solutions contract from a “key U.S. defense prime contractor” for a sensitive national security program entering full-rate production.

4) Market evidence of “defense flywheel”

Mears Machine landing a 10-year / $100M revenue agreement with a major defense OEM using a fleet of Velo3D Sapphire XC printers (strategic ecosystem effect).

Throw in the NDAA which was signed last December prohibiting AM from China + Russia without a national-interest waiver and encourages domestic production in addition to $3.3B allocated for additive manufacturing in the FY26 defense budget.

Also throw in SpaceX continuously ramping up Starship ahead of giga IPO as well as other space/defense clients like Anduril, Lockheed Martin, Raytheon, GD, Firefly, etc... all of which again are part of the super spending and production cycle.

All I see is a hypergrowth company in the right place at the right time working hand over fist to meet the aggressive demand from two of the hottest industries at the moment.

The company is currently at ~$220M market cap with 2025 revenue guidance around $50M (30% YoY growth) and 2026 will most likely be higher will all the positive tailwinds the AM industry and Velo3D specifically is experiencing.

...

So yes there might be a bit of an overhang from the PIPE but we're talking 3.6M shares that went effective late Jan and the daily trading volume since then has exceeded that by a lot.

So what are the shorts betting on that I'm missing?