@SS0006080831473 That's not what I expect it's just a reverse DCF model to see what growth rate is priced into the stock. I also expect fcf to grow not shrink.

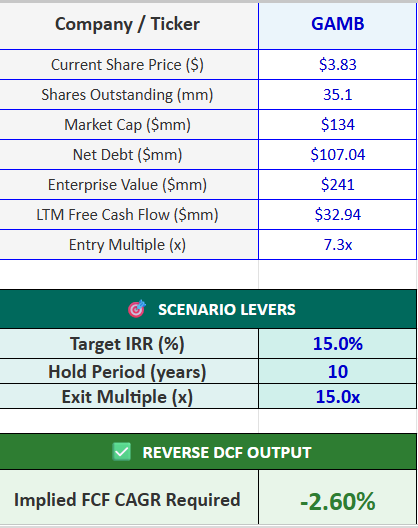

A small company that has gone under the radar is $GAMB. A reverse DCF model shows the market is pricing in negative fcf growth even with a 15% discount rate. To put it simply if $GAMB can grow fcf at a -2.6% CAGR over 10 years assuming a 15x multiple, you can make 15% IRR.

$NU is quietly building such a powerful tech stack in global finance. This interview with CTO Eric Young dropped some really interesting insights. Legacy banks run on old mainframes stitched together from dozens of messy acquisitions. Nubank is cloud native and mobile-first by design. Young highlighted their immutable data architecture. This means their system data can only be appended and never overwritten. This is a massive structural moat. It lets their developers ship code at warp speed without risking customer funds. They can iterate fast like a tech startup and still protect capital.

The real game changer is their AI strategy. Most banks just use AI for simple support bots. Nubank is going way deeper. They already bought an AI core team called Hyperplane. Now they are building custom foundational models for finance. They already published a paper on NuFormer. They use transformer architecture to read financial transaction histories. It is the exact same underlying tech behind ChatGPT. But instead of predicting the next word in a sentence, the AI predicts the next financial move. This gives Nubank an edge in pricing credit risk. Better risk models mean they can safely lend money to millions of new people. That directly expands their bottom line and prints cash.

Young also made it clear they are nowhere near done. They already dominate Latin America with 100M+ customers. But management is hunting a multi-trillion dollar global market. This is a pure tech juggernaut. Listen to exactly what he says at about predicting credit extensions. Expanding the loan book without expanding risk is key.

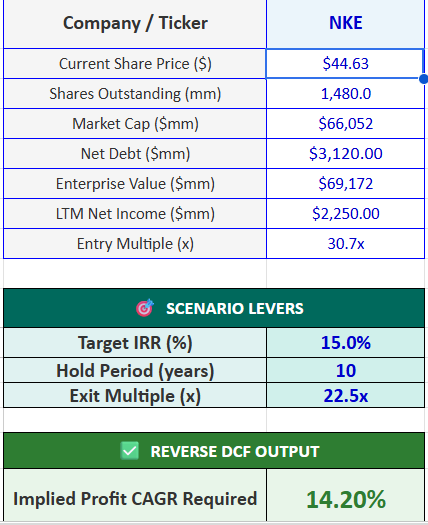

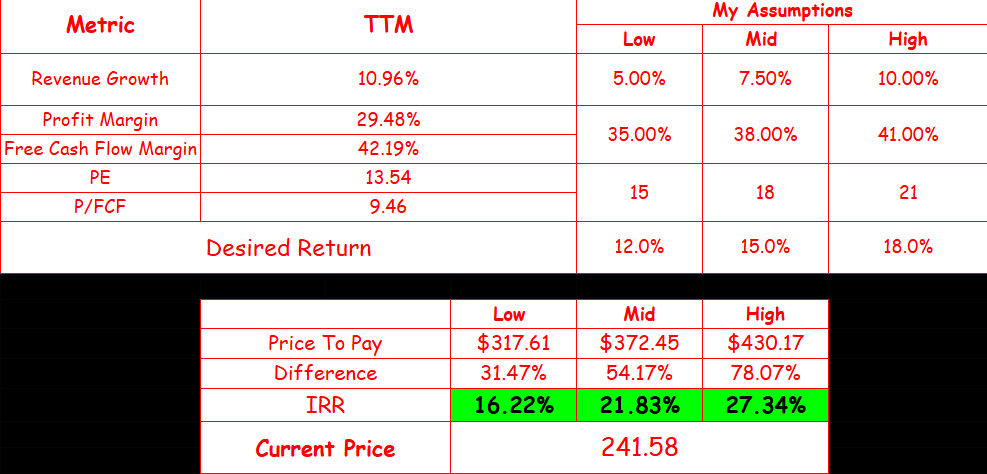

$NKE has been beaten down badly but the question is can they turn it around and can they grow profit at a high enough rate to generate a high rate of return. If they can grow profit at 14.2% assuming an exit multiple of 22.5x you can get a 15% IRR.

The "you're not an investor if you sell" club.

$ADBE down 28% since cut.

$DUOL down 50% since cut.

$ALAB down 23% since cut.

$TMDX down 23% since cut.

$PATH down 15% since cut.

$HIMS down 70% since cut.

$PYPL down 24% since cut.

Learning to cut losses is an important part of an investor journey.

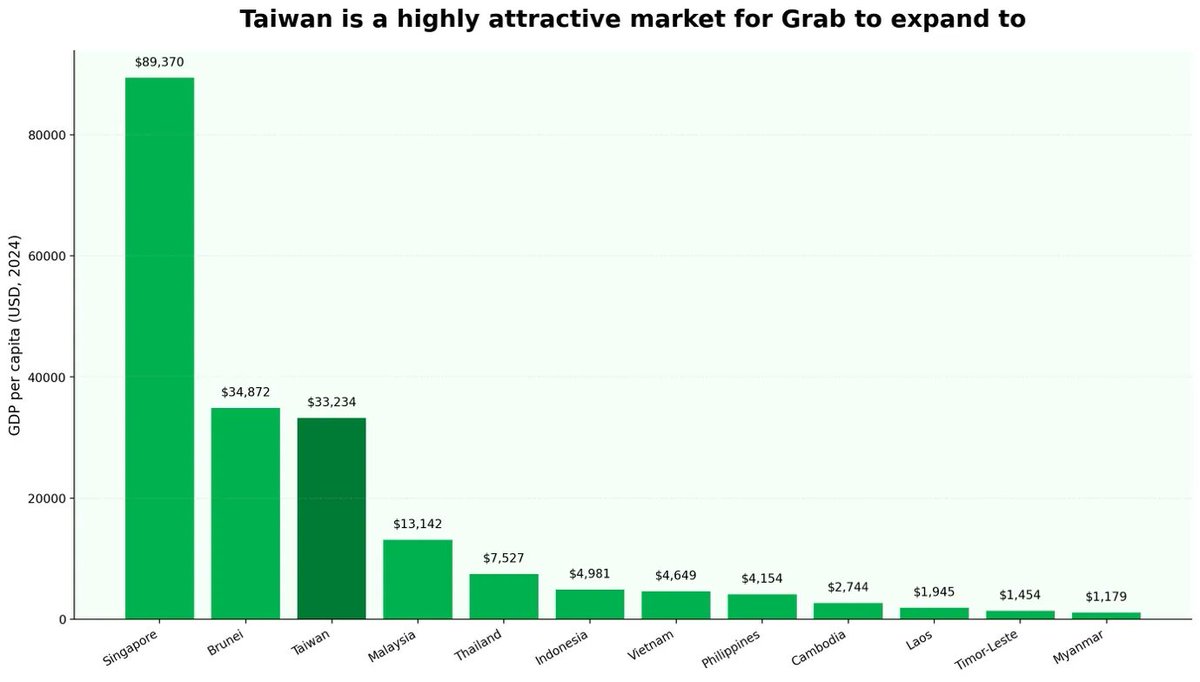

Here is why $GRAB decided to enter Taiwan! 🇹🇼

Apart from Singapore, Taiwan has a much higher GDP per capita compared to Southeast Asia.

- $33K

- 2.5x Malaysia

- 4.4x Thailand

- 6.6x Indonesia

- 7.2x Vietnam

Smart deal for just $600M!

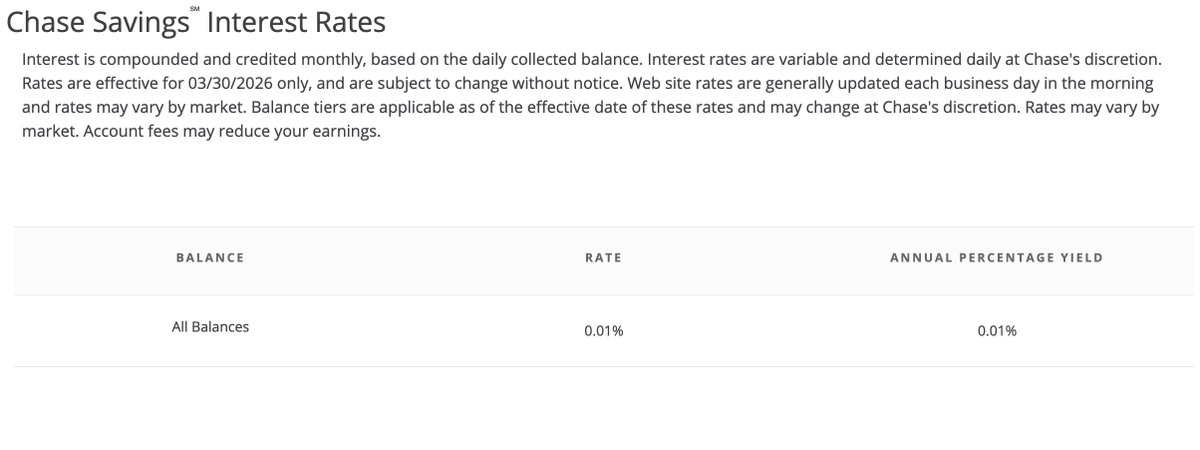

I don't understand why big banks like $JPM even bother paying interest if they are gonna do this.

This is just an insult to your customers.

No wonder companies like $SOFI are getting so popular.

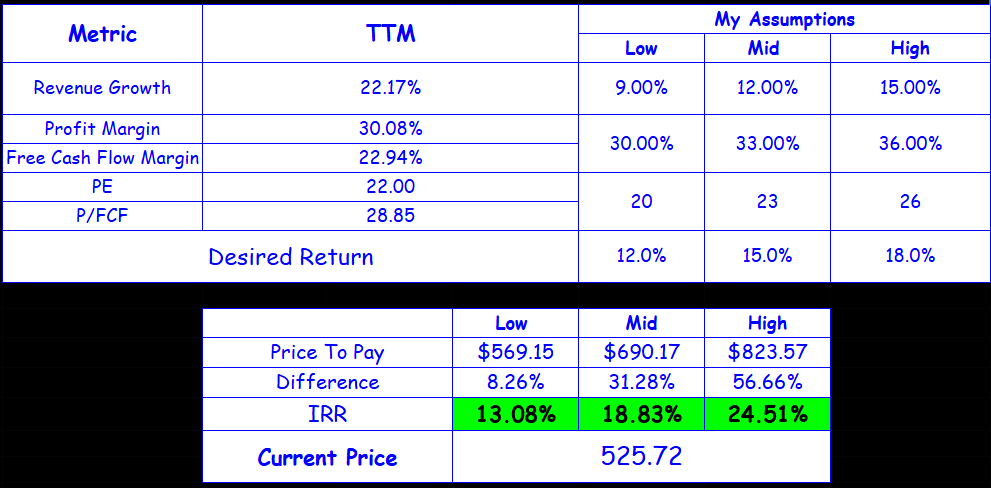

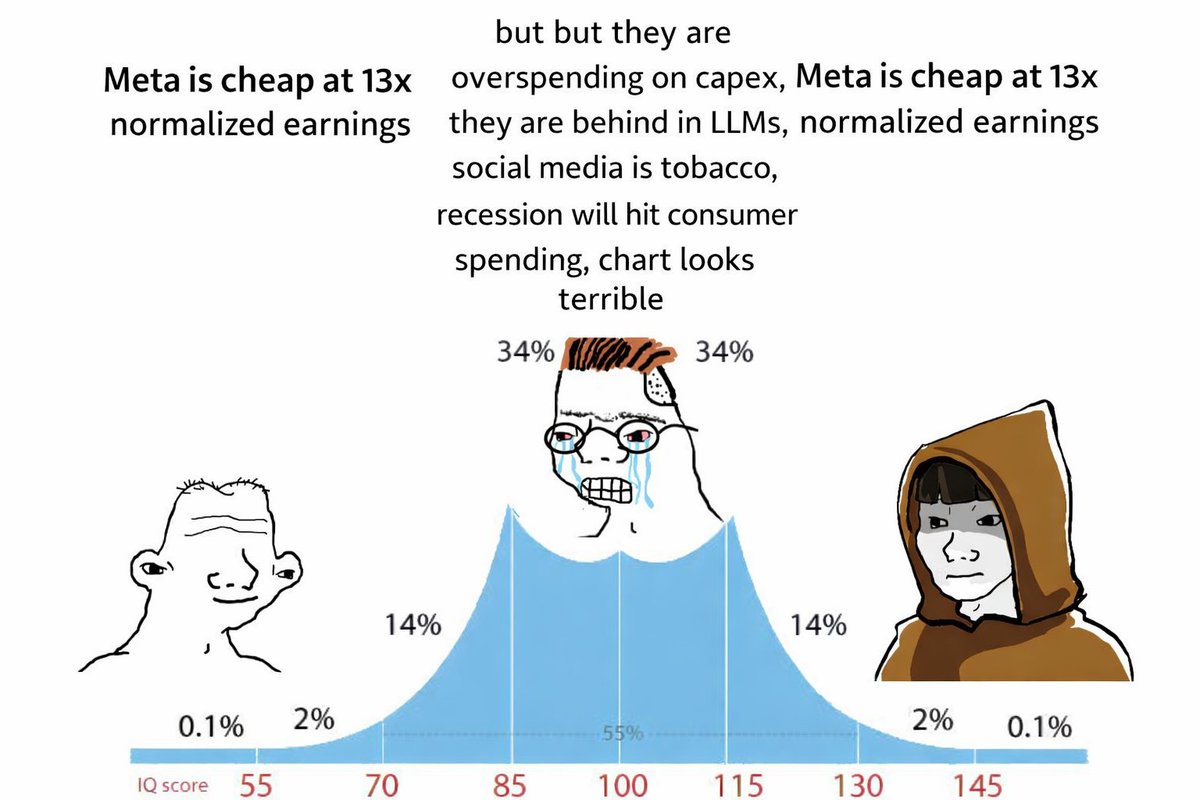

$ADBE is out of my circle of competence but the valuation is very attractive. If these assumptions play out even on the low end you can make a lot of money.

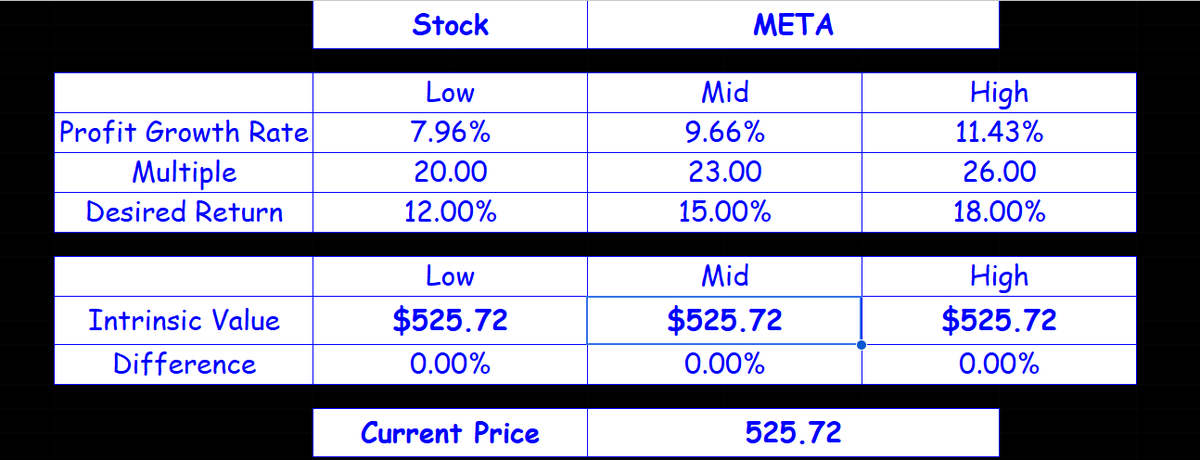

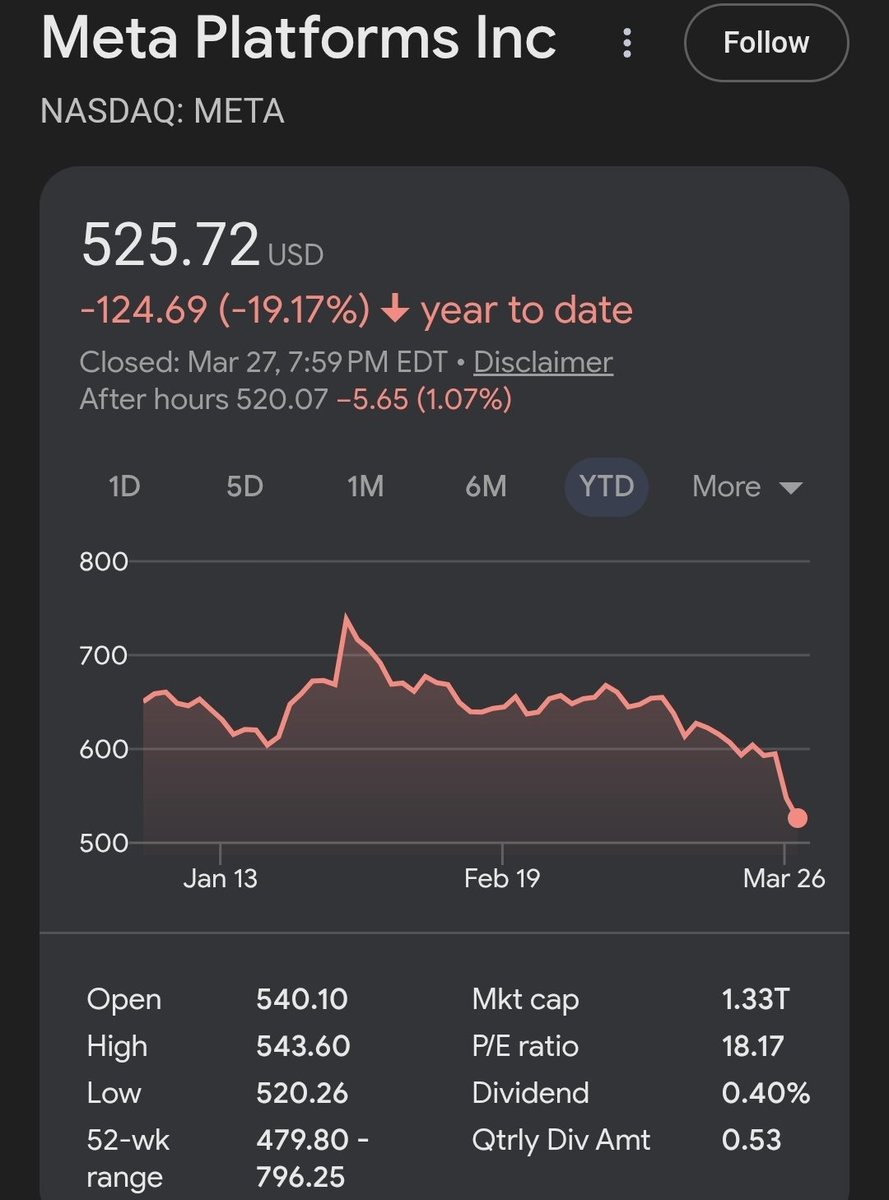

If $META can grow net income on average around 9.5% a year for the next 10 years assuming a 23x exit PE multiple, you can make a 15% IRR for the next 10 years.

@FluentInQuality It's more about giving lenders another option and with FICO having much higher prices already they might not be able to raise prices at such a high rate.

@DaCatalyst VantageScore has been 'competing' with FICO since 2006 (I believe). FICO's moat hasn't moved because the GSEs mandate it. Tell me the specific regulatory change that breaks that, and I'll revisit the margin assumption.

I stress-tested $FICO with the most conservative assumptions I could justify.

- 12% revenue CAGR

- Only 1% margin expansion over 10 years

- No dividends whatsoever

- Minimal buybacks

- 26x P/EBIT exit multiple

Projected total return: 16.66% CAGR over 10 years.

Not the base case.

Not the bull case.

The conservative case.

For a business that scores every American's creditworthiness.

The bar to win here is remarkably low.