ทวีตที่ปักหมุด

$NBIS is up 83.43% YTD but I still think the upside is just beginning.

Most investors would look at a stock that’s nearly doubled in six months and assume the easy gains are over.

I don’t.

I think Nebius is just getting started. This isn’t a story about chasing momentum. It’s a story about what happens when a company combines world-class engineering, customer obsession, capital discipline, and full-stack control, all aimed at solving the single biggest bottleneck in AI: infrastructure.

No debt. Over $1.4B in cash. Zero reliance on any one customer. And a founder who has built a multibillion-dollar platform before and is clearly doing it again.

Vertical integration done right

Nebius doesn’t rent space in someone else’s data center. It builds its own. The company designs custom racks in collaboration with NVIDIA. It owns and operates GPU-optimized, hyperscale data centers in Finland, Kansas City, and Iceland. A massive 300 MW facility in New Jersey is underway. A new site in Israel has just been greenlit.

All of it is purpose-built for AI workloads. Not general-purpose cloud. The result is structural cost and performance advantages. Better cooling. Faster deployment cycles. Tighter hardware-software integration. Energy efficiency on par with top-tier hyperscalers.

Most AI infrastructure providers are selling raw compute. Nebius is selling outcomes. The company offers everything from bare-metal GPU clusters to a complete AI cloud platform with integrated orchestration, inference-as-a-service, observability tooling, and API access to open-source models. Its AI Studio already serves over 60,000 developers. The cloud platform shipped nearly 50 software upgrades in Q1 alone. Kubernetes, Slurm, MLflow, DStack, SkyPilot. All supported. All optimized for AI workloads.

This is a software company disguised as a cloud platform. And that’s exactly what makes it so powerful. It starts with infrastructure. But the real moat is experience.

Execution is exceeding guidance

In their March call, management guided for $220M or more in ARR. They delivered $249M. In April, they hit $310M. For full-year 2025, guidance stands at $750M to $1B ARR. If current trends hold, that may prove conservative.

Revenue for Q1 came in at $55.3M. That may seem light, but it misses the bigger picture. ARR ramped hard during the quarter, and the timing of contract start dates muted revenue recognition. Profitability, however, showed clear progress. Adjusted EBITDA came in at negative $62.6M, ahead of expectations by over 30 percent. The core business is expected to be breakeven by Q3. Adjusted EBITDA will turn positive in the second half.

They are doing exactly what you want to see in a scaling infra business: ramping top line, managing burn, and delivering leverage, all while maintaining discipline.

Founder-led with full alignment

This is not another GPU reseller racing to undercut pricing. This is founder-led infrastructure execution.

Arkady Volozh built Yandex into a $30B tech ecosystem across search, cloud, e-commerce, and AI. He left the company over geopolitical reasons and brought hundreds of engineers with him. Now he’s building Nebius. And he’s all in. He owns a significant stake and has over 90 percent of his net worth tied to the company’s success.

hat alignment shows up in how they operate. Nebius is engineer-first, customer-centric, and focused on solving real bottlenecks with real infrastructure, not financial engineering.

You’re buying the whole ecosystem

And when you buy NBIS, you’re not just getting the AI cloud. You’re getting exposure to multiple high-upside bets.

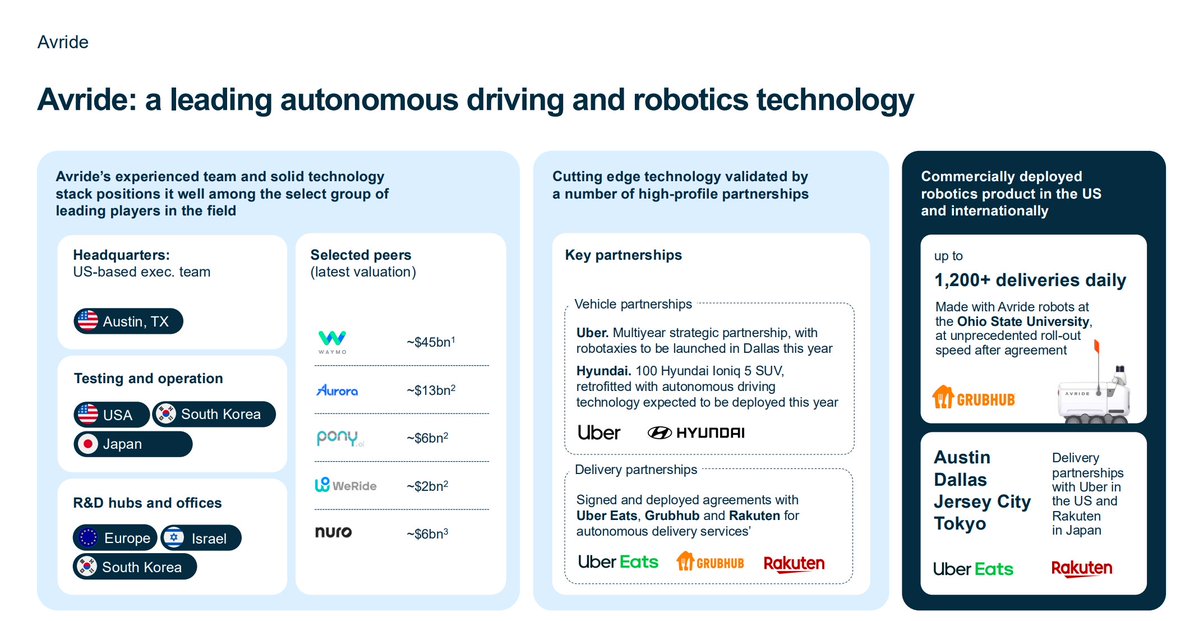

Avride is their autonomous vehicle and delivery robotics platform. Already partnered with Uber, Grubhub, and Hyundai. Completing over 1,200 robot deliveries per day. A 100-vehicle fleet is launching by year-end. Management believes Avride is worth billions and is actively exploring third-party investment.

Toloka is their AI data labeling business, already working with Microsoft, Shopify, and Anthropic. It just secured strategic investment led by Bezos Expeditions. Revenue doubled year over year in Q1.

TripleTen is their EdTech and tech reskilling business, growing 144 percent year over year. It’s expanding across Latin America and now booking early B2B revenue.

And then there is ClickHouse. Nebius owns 28 percent of it. ClickHouse is currently raising at a $6B valuation. That makes their stake worth roughly $1.68B. If monetized, this could fund years of infrastructure expansion without touching the equity base.

Demand is just getting started

These aren’t side projects. These are strategic assets. Each could move the needle materially on value.

But the real story remains the core platform. GPU supply is constrained globally. Hyperscalers are hitting capacity limits. And demand for high-performance compute isn’t slowing. It’s compounding. Nebius is meeting that demand not with shortcuts, but with scale. They are actively deploying H200s, preparing for Blackwells, and building toward 100 MW of contracted capacity by the end of 2025.

They’re not just meeting demand. They’re ahead of it.

And the customers are coming in waves. Today it’s AI-native startups and model builders. Tomorrow it’s enterprises and frontier AI labs. Beyond that, it’s national-level AI infrastructure programs. Governments around the world are now funding their own AI initiatives and looking for sovereign compute providers. Very few companies are in position to serve them. Nebius is.

There are not many businesses in public markets with this level of control over their stack, this level of customer traction, this kind of financial position, and this kind of alignment at the top.

They are targeting 30 percent EBIT margins at scale. Adjusted EBITDA turns positive this year. Their GPU depreciation schedule is more conservative than peers like CoreWeave. They have committed to limiting dilution by leveraging their subsidiaries and investments for capital. And they have the firepower to do it. Between Avride and ClickHouse alone, there are billions in optional liquidity on the table.This is not a story of explosive revenue with no path to profitability. This is disciplined, full-stack cloud infrastructure execution with optionality everywhere you look.

And right now, it is still misunderstood.

I’m not here to guess what the stock does next week. But I am very confident that three years from now, most people will look back at this period and realize this was the inflection.

The infrastructure is being built. The contracts are being signed. The customers are scaling. The engineering team is delivering.

I will be opening a large position Monday.

English