@EndicottInvests TBH after it was destroyed on zero news at the end of last year this is the bare minimum especially how disgustingly cheap this stock is still

English

blkjf

54 posts

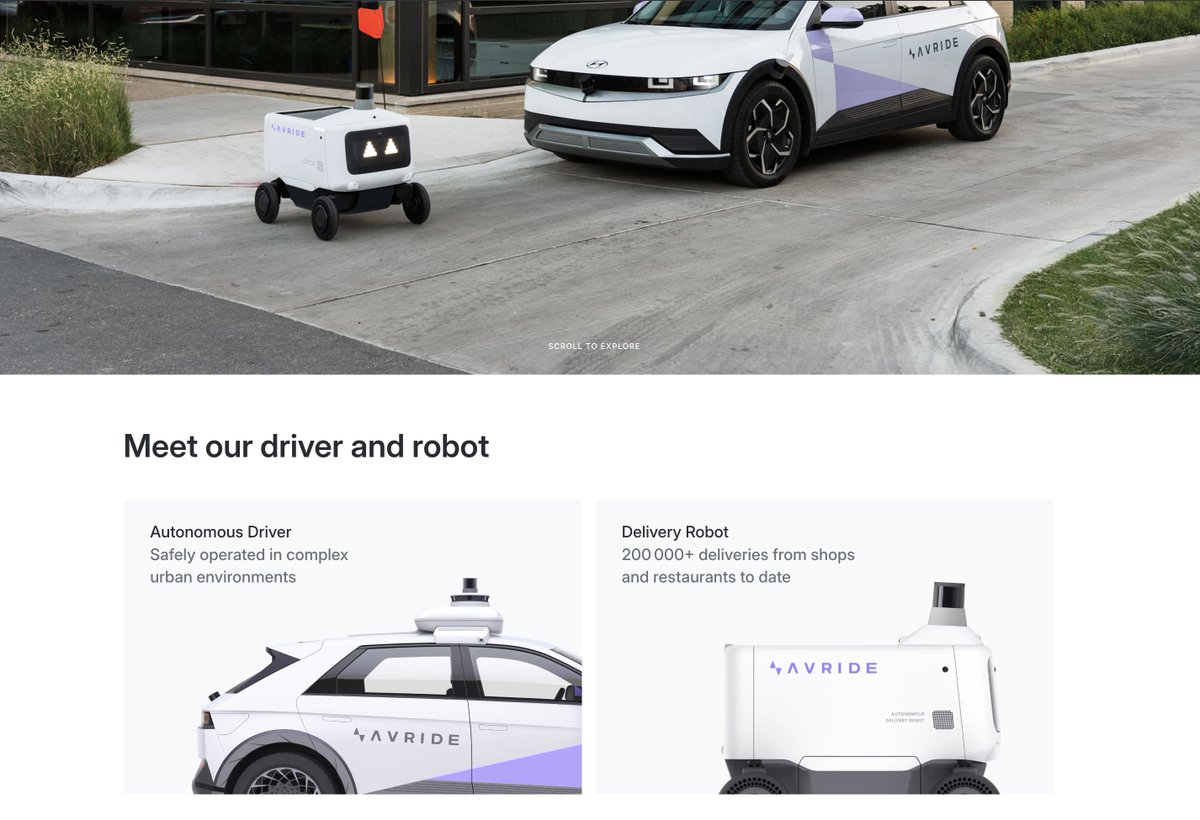

Nebius [ $NBIS ] is the most undervalued growth company right now. And it has the potential to become the next $GOOGL at a $21B market cap. There's one simple reason: It's portfolio companies are mindblowing. The most incredible example on this concept is the company $FTX. Here's the story: When we look at how $META grew into a $1T+ company, it wasn't just Facebook. It was their portfolio companies Instagram, Whatsapp, and others made Meta dominate the social media landscape. $FTX was doing something similar, but in digital assets and frontier technologies. Four years ago, in 2021, $FTX invested $5.8B into a large basket of assets. And put a large chunk into these three core companies: 1. Anthropic, 13.56% at a $2.5 Billion valuation. 2. Robinhood [ $HOOD ] 7.6% at a $8.54B valuation 3. Solana [ $SOL ], 41M+ tokens. Fast forward to today, that would have been: · Anthropic in it's latest round is worth $350B. That stake would have been worth ~$47.4B. · Robinhood is now worth over $100B. That stake would be worth ~$7.6B. · Solana is now worth $131.5 per token, making the stake well over $5.7B. Those three companies alone generated well over $55B+ in value in 4 years time, and this is not even including FTX's tens of billions of dollars + hundreds of other investments + holdings in Chime, Layerzero, Aptos, Hidden Road (bought by $COIN), and crypto. Their portfolio companies outlasted their core business (and imagine, how much it would have been worth if the core business kept scaling like $GOOGL search did alongside Youtube). $NBIS now has the same setup as $FTX did in crypto, $META in social media, but in artificial intelligence with a legitimate and incredibly rapidly growing core business. Nebius owns: 1. Clickhouse, 28% at a ~$7B valuation ($6.3 H1 2025) 2. Avride, 83% at a ~$6B valuation. (post Uber raise) 3. Toloka AI, ~65% at a ~$640 million valuation 4. TripleTen, 100% at a ~$300m valuation. · Clickhouse powers Anthropic, $META, $TSLA, $NET, and many fortune 500 companies. · Avride is a self-driving car robotaxi company, spun out of Yandex that $UBER invested in a $375M round in to compete with Waymo. · Toloka is a AI labeling platform that Amazon, Microsoft, Anthropic, and Shopify uses. $1.96B + $4.96B + $416M + $300m = $7.6B valuation in portfolio companies that are growing faster than most public growth companies. But if we look at their core business that is scaling to 700%+ Y/Y to $7-9B ARR, with $4.8B in cash, powering $META, $MSFT, Cursor, governments, and many more... This might be the last month it's under $90 before it receives hundreds of millions to low billions of extra inflows from MSCI inclusion today. There's no other datacenter growth company that has this type of portfolio if we look at crowd favorites like $IREN or $CIFR. $NBIS is only valued at $21B and the market is sleeping on this opportunity.

$PYPL New hire for @PayPal ads! 'Paypal has incredible reach. Over 430M active accounts. 35M merchants. 200+ markets. An unmatched view into what consumers purchase and what they may want next. This unlocks a rare opportunity to bring unique commerce solutions and new ad revenue to premium publishers and platforms. As payments become the new cookie, I’m excited to help build our industry’s next great advertising business in this new agentic world. Reach out and let’s build new partnerships together. We're moving fast at PayPal Ads!' Jim Prandato has previously worked at The Trade Desk, Spotify, and Roku. Not bad at all. Seems like Dr. Mark Grether is wasting no time 👏

Fun fact: Back in April, analysts estimated $NBIS' 2026 revenue at $880.9M. Today, that estimate is over $1.5B, a 74% increase in just five months. The company still has limited coverage, so I expect expectations to keep heading higher.

$NBIS' Founder and CEO, Arkady Volozh, is selling ~4.1M shares for roughly $270.5M. This was a pre-planned sale (from June) and only represents 13.3% of his position. He remains the largest shareholder, still owning over 11% of the company. Nothing burger IMO. Insider sales rarely mean much when alignment is intact, and that’s exactly the case here. I have no doubt Arkady’s motivation remains unchanged.