@iBladesi Mikey getting the full alt asset mgr treatment he always wanted ;)

English

ExcessDefaults

3.2K posts

The most important concept for allocators to understand in private equity is that IRRs are numbers used in marketing and not representative of investor retuns In the below example, a 20% "IRR" is actually equal to an 11.9% annualized return (and that's with generous assumptions)

Chemicals have been laggards for years. Today their relative trends flipped from bear to bull, with lots of runway remaining.

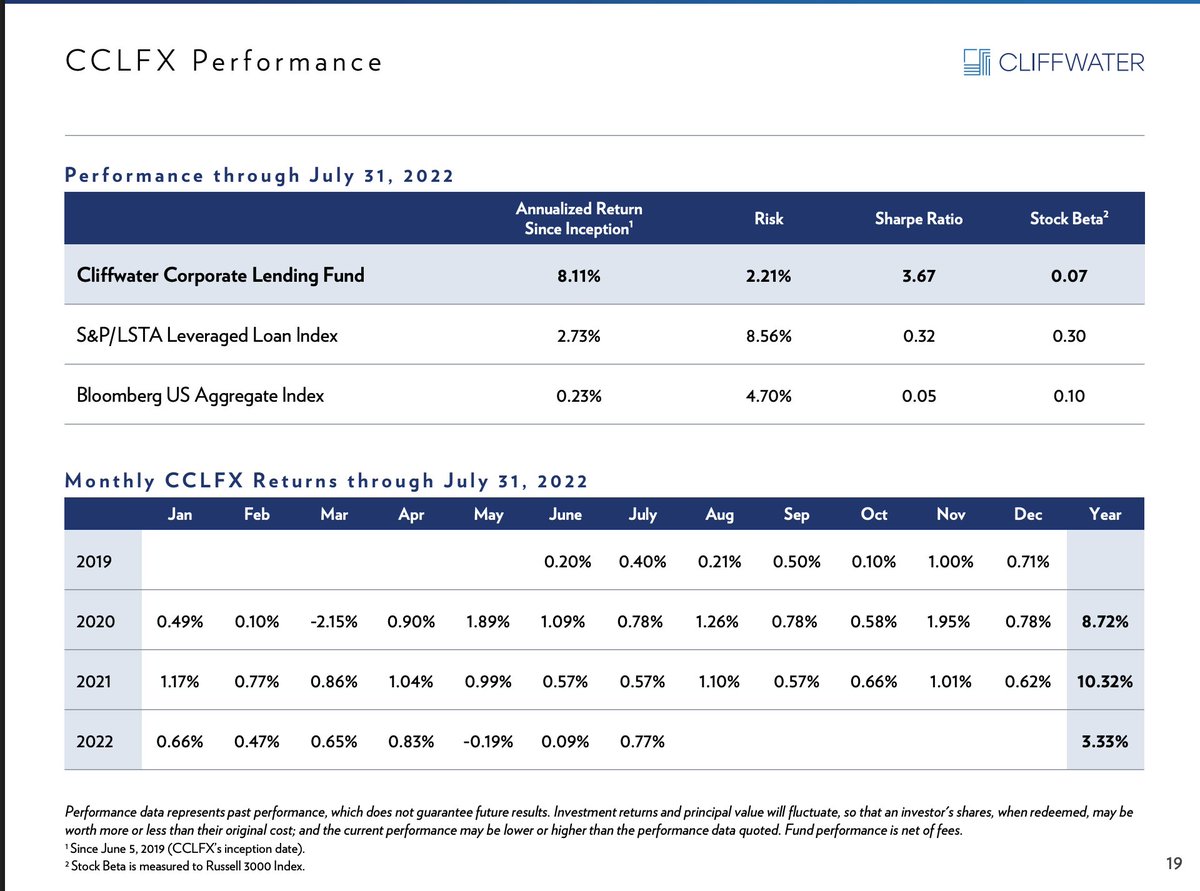

Cliffwater discussion on dentist forum getting spicy - v interesting bc all between a sizable group that all hold position in it.

BDC Software Exposure A HF friend of mine had his analyst go through the 10-K's of the top 22 public BDCs. The analyst used Pitchbook and Claude to categorize every loan by industry. According to their findings, $OTF had highest software exposure 55% by Pitchbook and 65% by Claude .. not surprising at all. But 2nd biggest exposure to software was $TSLX at 46% by Pitchbook and 57% by Claude .. pretty surprising. Do your own work but transparency is coming to PC one way or another. I don't have positions in either $OTF or $TSLX.