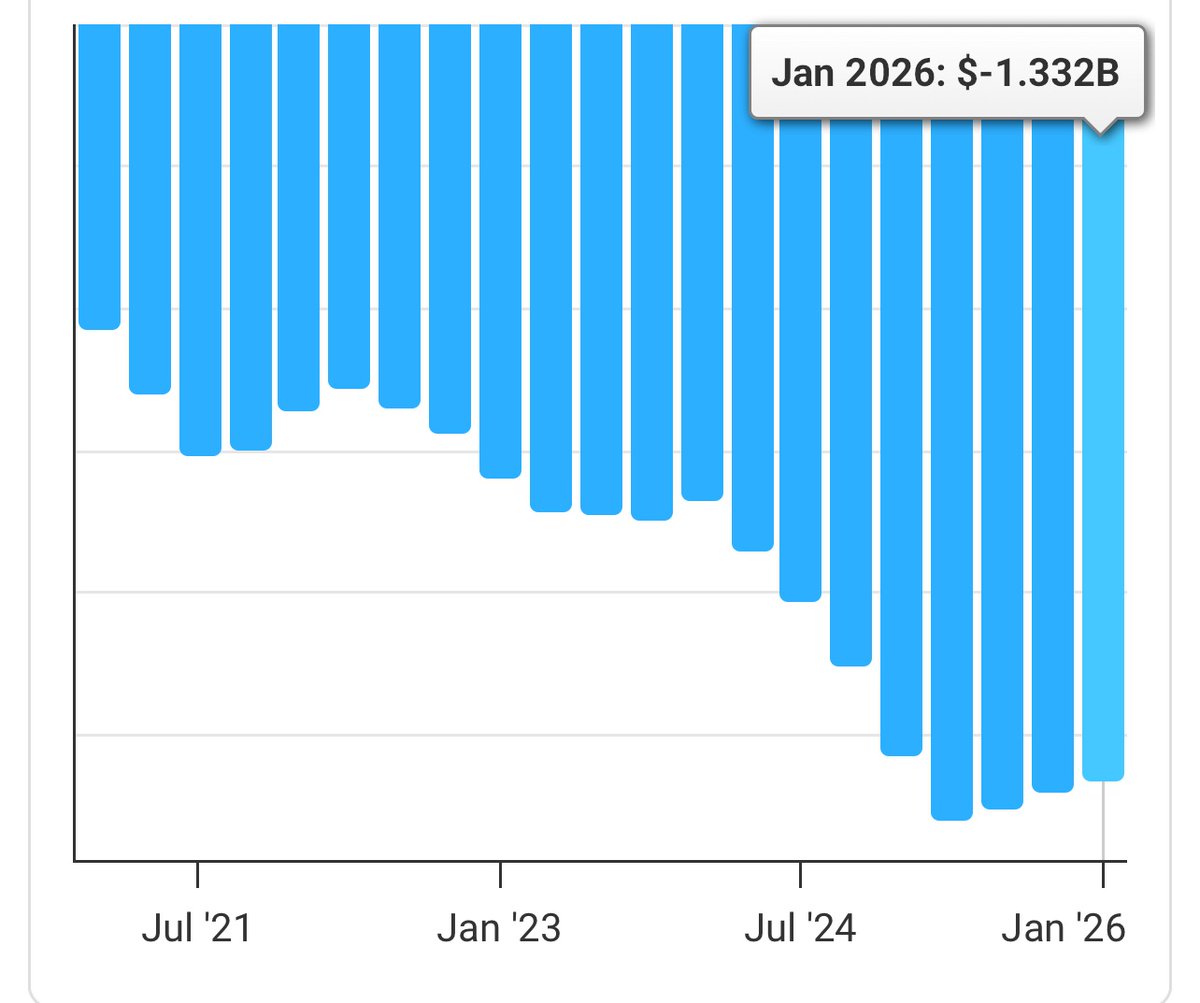

@buccocapital Hey but you can buy this endless stream of losses for only 11x sales now!

English

Jason Liebel

188 posts

@JasonLiebel

L/S investor. Background in asset allocation, finance, economics. Engaged in public markets and private real estate. 🇺🇸🇸🇪

NEWS: The rumors are true, @maustermuhle reports 👇 The National Park Service is removing a popular section of the 15th Street NW protected bike lane, saying that it will cause more traffic during cherry blossom season. 51st.news/trump-administ…

SALESFORCE JUST BOUGHT BACK $25 BILLION WORTH OF STOCK Salesforce $CRM just said it went forward with the prepayment and initial delivery of ~103M shares under its previously announced $25B accelerated share repurchase "This transaction, the largest ASR in history, represents the immediate execution of half of the $50 billion aggregate Share Repurchase Program authorized by Salesforce's Board of Directors in February 2026."

This morning, we released our newest note on the Once Upon A Farm $OFRM IPO. Co-founded by actress Jennifer Garner, the co has seen wild success in its refrigerated/cold-pressed snack pouches. However, nearing mature gross margins, we struggle to see how this unprofitable company can expand much further, even on the heels of solid y/y growth. See why below - earnings on March 12. cedargroveresearch.com/p/ipo-notes-un…

Already was $EVLV's largest deal in history but now: "[GCPS] has finished installing Evolv weapons detectors in every middle and high school..and officials are now exploring whether elementary schools could be next" *Btw 3x more elementary vs HS & MS wsbtv.com/news/local/gwi…

$TALK - Why I think It could be a multi-bagger, with 100% upside to 2025 revenue growth and EBITDA estimates. 1) people with access to talkspace through health insurance coverage will grow +35% to c.200m (2/3 Americans) over next 12 months, thanks to Medicare roll out.