ทวีตที่ปักหมุด

Nomatic

19.4K posts

Nomatic รีทวีตแล้ว

Nomatic and the Edge Podcast team (DeFi Dad) are great influencers to follow for DeFi Yields and projects:

Nomatic@Nomaticcap

English

Nomatic รีทวีตแล้ว

I can't get over the fact that Dune is about an oppressed people fighting for their homeland, waging a jihad to bring down a hegemonic empire by threatening to cut off the flow of their most precious commodity after the empire had assassinated their religious leader's father.

English

.@joekent16jan19 is an American hero

Tucker Carlson@TuckerCarlson

Joe Kent on why we actually went to war with Iran.

English

@HardYackaMacka @NickNemo17 @SecScottBessent @POTUS @SECPaulSAtkins @SenatorTimScott @SenWarren That's fine if the information is real

English

QME

TLDR: I am a recovering alcoholic with no fund, no credentials, and no lobbyist. I rebuilt myself from nothing. Then I broke into finance with no degree, no pedigree, and no permission.

I parsed SEC filings for a $31.5 billion private credit fund called Cliffwater. Not because anyone asked me to. Because nobody else would. The filings are public, but they are buried in footnotes that are not indexed, not searchable, and not structured for analysis. I have been told by fund managers that nobody even attempts this.

Billions of dollars in pension capital, and the people who manage money for a living do not bother to read the filings.

So I read them. Every loan. Every amendment. Every semi-annual PIK disclosure. 2,330 positions. I hand-researched fifty.

I found 189 loans where borrowers are paying interest with more debt instead of cash. I found over 50 loans that are not generating enough cash to service their debt at all — carried at par on the books of a fund that has never reported a losing month in 41 months.

The fund's Sharpe ratio is 3.75. Bernie Madoff — who was fabricating returns and could pick any number he wanted — ran a 3.5. He got caught because the numbers were too smooth by Markopolos. The greatest quant fund in history, Renaissance Technologies, runs a five or six.

Cliffwater is claiming risk-adjusted returns that would be impossible even if you insider-traded with perfect information every single time, because the volatility of the underlying markets would still prevent it.

Nobody asked questions.

Bloomberg confirmed 14% redemptions 48 hours after I published. S&P cut the fund's outlook to negative this week. Cash on hand fell 76% in six months.

This is not an isolated fund. This is the structure. $9.4 trillion in private equity. $3.5 trillion in private credit. They all pay their own valuation agents. The valuation agents decide what the funds are worth. No valuation agent has ever been fired for saying the number was too high.

The marks produce the NAV. The NAV produces the fees. The fees come from pensions. The pensions come from firefighters and teachers and nurses in Oregon and California and Illinois who will never read a private placement memorandum in their lives.

Wall Street ran out of rich people. The endowments were full. The sovereign wealth funds were tapped. So they went downstream — to 401(k)s, to retirement accounts, to interval funds sold to people who have no idea what they own.

1. Direct the SEC and FSOC to examine Level 3 fair value practices across interval funds and BDCs.

2. Require that valuation agents be independent of the funds they mark.

3. State publicly that the current self-marking regime creates systemic risk.

4. Mandate position-level mark disclosure for every fund that accepts pension capital.

There are two ways this ends. It breaks all at once like 2008 and we fix it. Or it rots slowly like Japan: one fund blows up, six weeks of quiet, another one, and nobody connects it for a decade while a generation of retirees gets destroyed.

I am not asking anyone to take my word for it. I am asking them to read the filings.

If you know someone in the administration, a regulator, or anyone on a legislative committee, please send this to them. One person learned this from a one-bedroom apartment. Your government can too.

The will is what is missing.

Nick Nemeth (Mispriced Assets)@NickNemo17

English

Nomatic รีทวีตแล้ว

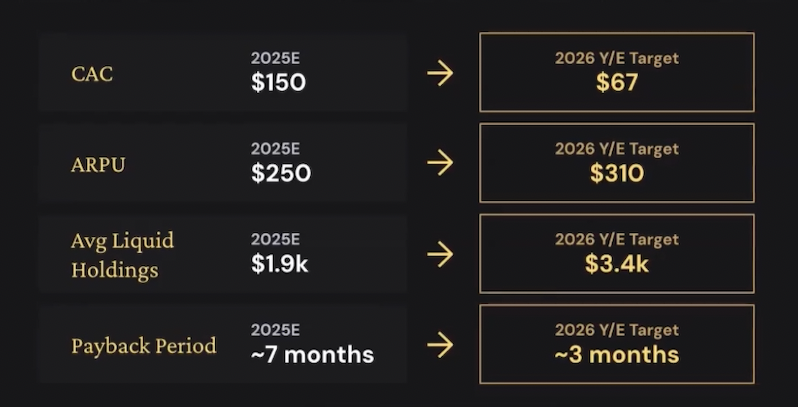

✅Etherfi buybacks are back on (no clue why they were off for a few days)

✅ Final investor vest sent out. No more VC overhang.

✅ Daily spend at ATH using cards ($2.5M/d)

✅ Staking TVL back above $6b

✅ Upbit listing yesterday

✅ Adding ~300 new cards a day

✅ CAC going down, ARPU going up, Payback period compressing

sallygazzy mode

note: dcf cap seeded ethfi

English

Hyperion or ticker $HYPD stands out as the most unique DAT I have covered. Rather than the typical buy, hold, and trade at a premium to NAV strategy, they have decided to put their HYPE to work in a very nascent HYPE DeFi ecosystem. This uniquely positions HYPD to gain not only substitution yield from first-mover advantages on things like lending, HIP-3, and staking, but also builds deep relationships within the HYPE ecosystem while positioning them to become early airdrop participants at a zero cost basis. Run by @hyunsujung_ as CEO, Hyunsu displays a masterclass on how to run a DAT.

Disclosure: This analysis focuses exclusively on HYPD's revenue opportunities and active DeFi deployments. I am not covering the full capital structure, outstanding PIPE deals, warrants, or dilution mechanics in this piece.

Hyperion's Revenue Streams:

HYPD breaks down into 5 revenue streams as it stands today.

1. Kinetiq Partnership for Staking

While I cannot see exactly how much HYPE is staked with Kinetiq, I do know there was a significant amount where they received nearly 2 million KNTQ tokens, coming out to about $216,000 at current prices. Remember, this is a $30 million company receiving these tokens at a zero cost basis. This is just the beginning of the airdrop flywheel: by being an early and deep participant in the Kinetiq ecosystem, HYPD is systematically positioning itself for future token distributions across every protocol it touches, all generated from capital already deployed for other purposes.

2. Felix HIP-3 Fee Share

This is the most distinct part of the revenue and DeFi flywheel, and where I feel the most bullish. HIP-3 deployers earn 50% of the fees, while the other 50% goes to the protocol, which is then used to buy back HYPE and burn it (hype rules). Felix currently has 12 HIP-3 perpetual futures markets live. At current volumes, Felix HIP-3 has done approximately $50 million in daily volume. At a 4.5bps fee take for Felix as deployer, they are generating around $8 million annually. Since HYPD provided 500,000 HYPE to assist the deployment of their HIP-3 market, I estimate they receive anywhere from 10–20% of these fees, or approximately $800,000–$1.64 million annually at this very early stage. This fee structure could be broken down differently, but we will not know until the earnings next week.

3. Rysk Partnership

Rysk is a bit more complex to explain and a fairly new venture for HYPD, but it is the most intellectually interesting part of their yield strategy. HYPD is using kHYPE and stablecoins as collateral. This is the clever part: kHYPE is already earning 2.37% staking APY while sitting in the vault as collateral. So HYPD is stacking two yield streams on the same capital simultaneously: base staking yield plus options premium on top. I am not yet sure how much notional they have deployed. I estimate approximately $10 million, though this has not been disclosed and will hopefully be confirmed on the earnings call. Based on the volatility environment, covered call strategies on HYPE can yield anywhere from 8–30% annually on notional. At $10 million deployed, HYPD could be generating anywhere from $800,000 to $2.5 million annually from this stream alone.

4. Native Markets / USDH

HYPD allocated 300,000 HYPE to the 1 million HYPE requirement needed for USDH to qualify as an aligned quote asset on Hyperliquid. HYPD is essentially one of three anchor stakers of USDH, earning the standard staking rate of 2.37%, which comes out to approximately $300,000 per year at current HYPE prices. That is the pure yield side. But there is an indirect angle that is actually more interesting. If USDH adoption grows from $21 million today toward the billions that USDC currently holds on Hyperliquid, HYPD's early strategic position as an anchor staker likely earns them deeper ecosystem rewards, governance influence, and potentially a share of the reserve yield distribution. The 50% of USDH reserve yield that goes to "ecosystem development" is currently unspecified in terms of who receives what. HYPD being one of only a handful of anchor stakers puts them in a privileged position for that. So approximately $300,000 per year from staking, with a potential additional $100,000–$500,000 from ecosystem rewards as USDH scales. THIS COULD BE A GIANT DEAL FOR HYPE PER SHARE METRIC NERDS.

5. HyperLend

This is the most straightforward but newest revenue stream, announced in early 2026. HyperLend is a private credit market on HyperEVM where institutions can lend and borrow against collateral. I do not yet know how much HYPD has lent, what collateral terms were negotiated, or how the deal is structured. I expect full disclosure on the March 26 earnings call. Based on remaining deployable treasury and typical private credit rates in crypto markets of 10–15%, and assuming a deployment of approximately $10 million, I estimate this stream could generate $1.0–$1.5 million annually. This remains my most speculative estimate.

A note on the HYPE treasury

One important accounting distinction worth understanding: HYPD's gross HYPE holdings stand at 1,862,195 tokens; however, only 1,427,178 HYPE sits on the balance sheet. The difference of approximately 435,000 HYPE is largely explained by the 500,000 HYPE deployed to Felix under the HAUS agreement. Because HYPD is providing the use of those tokens as HIP-3 deployer collateral rather than holding them outright, they cannot be carried on the books in the traditional sense. This is not a red flag. It is a structural consequence of HYPD being an active ecosystem participant rather than a passive holder. The HYPE is still theirs, still earning fees, and still underpinning the Felix revenue stream.

Against a current market cap of approximately $32 million, even the bear case implies a revenue yield of roughly 8%, while the base case implies ~14%. I look forward to the March 26, 2026 earnings call to gain clarity on the Felix fee split percentage, the Rysk notional deployment, the HyperLend deal structure, updated HYPE staking figures across all validators, and the full year 2025 financials. The combination of these disclosures should allow for a materially more precise revenue model and a clearer picture of the path to operational cash flow breakeven.

What makes this story truly compelling is what happens with these fees at the protocol level. The majority of revenue generated across every one of these streams ultimately flows back into the Hyperliquid ecosystem, with the protocol using 97% of trading fees to autonomously buy back and burn HYPE daily. Every trade on Felix generates fees that burn HYPE. Every option written on Rysk generates activity on HyperEVM that burns HYPE. Every USDH transaction generates reserve yield that buys back HYPE. HYPD is an active participant in a self-reinforcing flywheel where every dollar of revenue it helps generate tightens the supply of the very asset it holds. More activity drives more buybacks, more buybacks drive a higher HYPE price, a higher HYPE price increases the value of HYPD's treasury, and a more valuable treasury enables larger ecosystem deployments that generate even more activity. This is not a typical DAT.

English

@shaundadevens Yeah or you tbh (have this one bookmarked).

We also have Nick booked for a podcast next week 👀

English

When Carlos publishes a report you drop everything to read it.

One of the best in the game.

Carlos 🟪@0xcarlosg

English

@Nomaticcap no wonder syrupUSDT was the main mover this week

with all the private credit run-up last week it was quite obv where the volume will go

x.com/incyd__/status…

Ash (🇺🇦,🤖)@incyd__

tradfi private credit is cracking on-chain lending protocols are the next opportunity or the exit liquidity? here's what's happening and why syrupUSDC is the most interesting case study right now the macro context first — private credit is under more stress than any point since 2008 → blue owl permanently gated redemptions on its $1.6b OBDC II fund in february after a 200% surge in withdrawal requests. attempted merger would have crystallized 20% haircuts. shares dropped 9% → UBS projects private credit defaults climbing up to 3 percentage points in 2026 — worse than leveraged loans or high yield bonds → 15% of private credit borrowers can no longer cover interest payments per goldman sachs → PIK usage (paying interest with more debt instead of cash) is rising across the sector — 8% of BDC investment income now comes from PIK → morningstar DBRS: 61% of private credit borrowers showing margin compression over the past year → jamie dimon used the "cockroach" analogy — when you find one problem, more are nearby → gundlach called private credit the "top candidate to start the next financial crisis" this matters for defi because the narrative is shifting. tradfi institutions are now actively looking at on-chain credit markets — not as experiments but as potential distribution channels for risk they can't easily offload through traditional structures defi should not be exit liquidity for tradfi's problems which brings us to maple's syrupUSDC — the largest on-chain private credit product at ~$2.66b in deposits (63% of maple's $4.59b AUM) ➢ current 30d apy: ~4.8% ➢ yield source: overcollateralized institutional lending (120-170% collateral ratios, avg 160%+) ➢ borrowers: trading firms, market makers, crypto-native hedge funds ➢ collateral: btc, eth, liquid assets held at anchorage, bitgo, copper ➢ loan terms: fixed-rate, fixed-duration (typically 30 days), 5-9% borrower rates ➢ protocol fee: 15-20% of borrower interest (no separate management/performance fees to depositors) ➢ zero lender losses since may 2024 launch across $12b+ in cumulative originations yield decomposition: where does the 4.8% actually come from: → primary: overcollateralized crypto lending (this IS the base yield, no points or incentives since drips ended) → secondary: collateral staking enhancement (maple stakes posted btc/eth via liquid staking, passes portion to lenders) → tertiary: futures basis trading and selective defi liquidity provision → zero t-bill or treasury exposure — entirely crypto-native yield for context: aave usdc supply pays ~2.33%, compound runs 2-3%, vanguard money market (VMFXX) pays 3.76%, ethena susde fluctuates 3.5-5.1% the spread over fed funds has compressed from 500+ bps at launch to ~115-120 bps today. yield dropped from 21.3% total in 2024 (including drips rewards) to 4.8% net. that's a real normalization what must stay true for this yield to persist: → crypto borrowing demand must stay healthy bull markets drive rates, downturns compress them → collateral ratios must hold october 2025 flash crash saw lowest ratio touch 136% (normally ~156%), 9 margin calls all cured within 3 hours → instant withdrawal buffer must remain funded ($200m+ reported) — contractual max is 30 days but typical processing is under 5 minutes since april 2025 → maple's underwriting must continue performing — the 2022 defaults ($54m across orthogonal, babel, auros) were under the old unsecured model that's been completely replaced the risk stack you need to understand: → the core foundation lawsuit is real. core alleges maple breached an exclusivity agreement and misappropriated confidential info while building syrupBTC. injunction was granted blocking syrupBTC launch. maple returned 85% of btc principal. maple says it doesn't affect syrupUSDC but it raises questions about governance and asset segregation → centralization risk: admin keys, upgradeable contracts, protocol pausability. this is not a permissionless lending market → no deposit insurance. period → us investors excluded (no KYC required but automated AML screening + self-certification of non-US status) → yield compression could continue if fed cuts further and crypto borrowing demand softens, the 115bp spread over risk-free could narrow to the point where the risk premium doesn't compensate composability is where syrupUSDC actually differentiates: → aave v3: collateral-only, 73% LTV standard, 90% LTV in e-mode. $750m+ inflows within 6 months of listing → pendle: PT-syrupUSDC (fixed-rate) and YT-syrupUSDC (leveraged floating yield), pools exceeding $125m → morpho: leveraged looping (deposit → borrow USDC → mint more syrupUSDC → repeat) → kamino (solana): leveraged looping at up to 5-8x → drift: yield-bearing perpetual futures margin: earn ~5-8% on collateral while trading → cross-chain via chainlink CCIP on ethereum, solana, arbitrum, base the blue owl parallel is worth sitting with. a $1.6b tradfi fund gated redemptions permanently. syrupUSDC processed $67m in instant redemptions during the october 2025 crash without breaking stride. on-chain composability and real-time collateral monitoring are genuine structural advantages over opaque tradfi credit vehicles but .. and this is the part that matters, maple still operates as a centralized underwriter with full discretion over loan origination, borrower selection, and collateral management. the "decentralized" part is the deposit rail. the credit decisions are fully centralized the question for allocators is whether 115bps over risk-free adequately compensates for smart contract risk + centralization risk + no deposit insurance + regulatory uncertainty + the lawsuit overhang. in 2024 at 21% total yield the math was obvious. at 4.8% it requires a more honest conversation about what you're actually being paid for what's your threshold? at what yield does the risk-adjusted math stop making sense for on-chain private credit vs just parking in a money market fund

English

@TomintheT @FlashTrade Cool, thanks for the heads up, I hadn't heard of them.

English

@Nomaticcap Sir,.....Awesome product + revenue + holders rights = @FlashTrade⚡️. Do check them out.

English

Important for all crypto token investors.

A first principles starting point is whether a protocol is a good product that generates revenue. But an even more fundamental question is: does the token actually give holders any rights?

Put simply, can your investment be rugged?

Listen to @TheiaResearch break down token holder rights:

English

“There’s our little geopolitical AI expert! Why don’t you come downstairs and tell us more about your equity puts and how the Strait of Hormuz will lead to a global famine?”

English

I'll say it again.

DeFi depositors love fixed supply rates, even if it means being adjusted on a 2-4 week basis.

Guaranteed yield > 7-day average APY.

If you can pull it through, the product is going to attract more deposits. Sky's sUSDS is a good example.

Fluid 🌊@0xfluid

Introducing: Fluid Lite USD Vault A Fixed-rate Cross-chain Vault with the best risk-adjusted yield on stablecoins. Automated. Just deposit. Earn. That's it.

English