Alan Simon

13.1K posts

Alan Simon

@SlashSimon

Curious. Listening. Leading. An optimistic and determined problem-solver, collaborating with others to build fast and get things done in America.

เข้าร่วม Ocak 2010

215 กำลังติดตาม552 ผู้ติดตาม

“People drastically under appreciate how important everything that SpaceX & @elonmusk are doing right now.”

“It’s going to change the world.”

Christian Garrett (@CGarrett_15) @HillValleyForum

Molly O’Shea@MollySOShea

At 24 years old, SpaceX is already one of the largest & most *capital-efficient* companies ever built: SpaceX: ~$12B raised → $1.25T Val (target $1.75T IPO) OpenAI: ~$170B raised → $840B Val (target $1T IPO) SpaceX Financial Profile (Over 1 Year): 2025: $350B → 2026: $1.25T Valuation March 2025: $350B val, SpaceX had raised only ~$10B over 23 years, remarkably modest for its scale & valuation, +was already cash flow positive FY 2025: Generated about $8 billion in profit on $15-$16B of revenue, driven primarily by @Starlink's satellite internet service, which accounts for between 50% - 80% of total revenue (Reuters) February 2, 2026: $1.25T valuation, all-stock acquisition of xAI. Deal valued standalone SpaceX at ~$1 trillion & xAI at $250 billion. Widely reported as the largest M&A transaction in history. March 2026: @elonmusk announces SpaceXAI + Tesla TERAFAB Project, goal to reach a trillion watts of compute/year 2026: Targeting ~$1.75 trillion IPO Note: @xai (now part of @SpaceX) has reportedly raised ~$42B total (PitchBook). Combined, that’s ~$54B total capital against a ~$1.25T valuation. Figures based on recent public reporting; estimates may vary. Christian Garrett (@CGarrett_15) of @137ventures

English

@SpaceX will likely have the largest IPO in history sometime this year. The result will be orbital data centers at scale powered by the sun and commercialization of the moon. Starship will become a rocket-powered flying railroad.

Regolith mining and refining will be one of the first big projects. Robots, cobots, and other forms of automation will be prevalent. But, people will also spend some time working on the moon. Just ten short years from now, there will be a thriving moon economy, including tourism.

#moon

Alan Simon@SlashSimon

Moon City Is Coming Based on Elon Musk's recent announcement, SpaceX has prioritized establishing a self-growing city on the Moon instead of immediate Mars colonization, citing faster development timelines due to shorter travel times (2 days to the Moon vs. 6 months to Mars) and more frequent launch opportunities (every 10 days vs. every 26 months). The roadmap for lunar development builds on SpaceX's existing Starship program, which is designed for heavy-lift capabilities, orbital refueling and human-rated landings. While specific milestones beyond the near term aren't fully public, a logical progression based on the company's current trajectory, NASA Artemis partnerships and reported targets includes the following phases: 1. Near-Term Preparation and Testing (2026-2027) - Ramp up Starship orbital flights and demonstrate in-orbit refueling, a prerequisite for lunar missions. - Conduct uncrewed precursor missions to test landing precision, propulsion and surface operations on the Moon. - Key milestone: An uncrewed Starship lunar landing targeted for March 2027, as part of initial site surveys and technology validation. 2. Initial Human Presence and Base Establishment (2027-2029) - Follow the uncrewed landing with crewed missions, potentially integrating with NASA's Artemis program, e.g., using Starship's Human Landing System variant for Artemis III or follow-ons. - Deploy initial habitats, possibly inflatable modules or 3D-printed structures using lunar regolith, along with solar power arrays and basic life support systems. - Begin in-situ resource utilization (ISRU) experiments to extract water ice, oxygen and propellants from the lunar surface, reducing dependency on Earth shipments. 3. Infrastructure Buildout and Expansion (2030-2032) - Scale up to regular cargo and crew rotations, leveraging Starship's reusability for frequent deliveries of equipment, robots and supplies. - Construct core facilities like pressurized living quarters, greenhouses for hydroponic agriculture and mining operations for metals and volatiles. - Integrate AI and robotics for autonomous construction, enabling the self-growing aspect where the base expands using local materials without constant human oversight. This could include data centers or compute farms on the Moon, as hinted in broader xAI synergies. 4. Achieve Self-Growing City Status (2033-2035) - Transition to a semi-autonomous settlement capable of sustaining and expanding a population of dozens to hundreds, with closed-loop life support, local manufacturing and energy independence. - Focus on economic viability, such as lunar mining for rare elements or serving as a waypoint for deeper space missions. - Full self-growing city realization targeted within less than 10 years from the 2026 announcement, meaning by 2035 at the latest, where the outpost can grow organically without risking collapse from Earth-side disruptions. This timetable aligns with Musk's stated goal of a lunar city in under 10 years, driven by the ability to iterate rapidly. Delays could arise from technical challenges like radiation shielding or regulatory hurdles, but SpaceX's track record suggests aggressive pacing. #SpaceX #Moon #Starship #Industrialinspiration

English

Alan Simon รีทวีตแล้ว

Reshoring American critical mineral production one claim at a time.

Brandon Beylo@marketplunger1

This is Taylor Sulik (@TheTungstenGuy). He's a former US Coast Guard member turned mining entrepreneur and founder of Mithril Mining (@Mithril_Mining). What started as an intense passion in 2023 is now a full-fledged project generator business model with Strategic Tungsten Assets under ownership. Taylor isn't using Claude to make fancy calendar productivity apps. He's building a US tungsten company to provide the much-needed metal to the Department of War. And he almost died this weekend doing it, getting stuck in 3+ feet of snow staking claims in Idaho; rescued by the Sheriff's Department. This is American Entrepreneurship at its finest. I joined Mithril because I believe in Taylor and his mission to resurrect American Tungsten Production. Taylor is doing a very hard thing (building a mining company from scratch). But he's doing it. And his story is worth following.

English

Alan Simon รีทวีตแล้ว

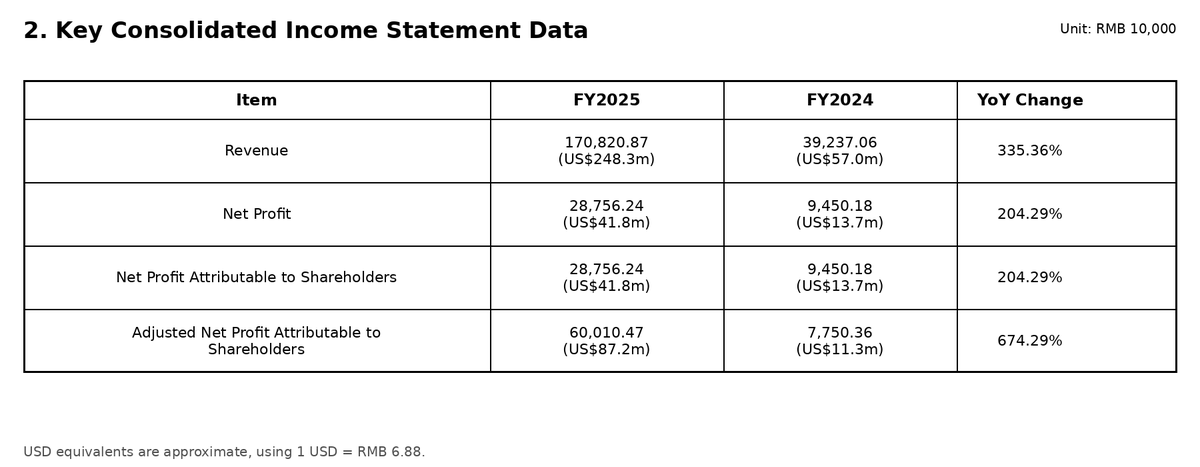

Incredible, lol, robot maker Unitree just filed for IPO and not only do they make money, their adjusted net margin is 35%, putting it on par with software companies. Humanoid fever is only going to increase from here I think :) At @TechBuzzChina we have some new special projects in this area we are announcing soon!

Some stats:

- Unitree’s STAR Market (Shanghai) IPO has been accepted, with a planned raise of RMB 4.2 billion (US$611 million) and an implied initial post-money valuation of at least RMB 42 billion (US$6.1 billion)

- 2025 revenue reached RMB 1.71 billion (US$248 million), - up 335% YoY, while adjusted net profit exceeded RMB 600 million (US$87 million), up 674% YoY.

- In the first 9 months of 25, humanoid robot revenue reached RMB 595 million (US$86 million), surpassing quadruped robot revenue of RMB 488 million (US$71 million) for the first time.

- Unitree shipped over 5,500 units last year, occupying 32.4% of the global humanoid market

- Of the IPO proceeds, the biggest chunk, RMB 2.02 billion (US$294 million), will go toward robot model R&D, followed by RMB 1.11 billion (US$161 million) for robot body R&D. Another RMB 445 million (US$65 million) is earmarked for new product development and RMB 624 million (US$91 million) for a manufacturing base.

English

TLDR: The SMR craze is a classic “category error” driven by CCGT envy. Gas plants win because the expensive, complex part (the jet-engine turbine) is fully factory-built, hot-tested, and shipped. Site work is just quick installation (24-36 months).

Nuclear is the opposite: the reactor itself is only 25-40% of costs. The real drivers: civil works, excavation, containment, seismic quals, nuclear-grade QA, redundant safety systems, and regulatory oversight are site-specific, labor-heavy, and don’t shrink proportionally with size.

Do you agree or do you think that certain SMR companies can avoid this conundrum?

Do you think that fusion power will one day obsolete fission?

chris keefer@Dr_Keefer

The SMR craze reflects a fundamental category error & combined cycle gas turbine envy. It tries to map the attributes of a CCGT plant onto nuclear, where the underlying cost structure & physical infrastructure is fundamentally different. A CCGT plant is essentially a jet engine bolted to a heat recovery steam generator and a smaller steam turbine. The critical point is where the complexity sits. The gas turbine, which is the expensive & technically demanding component, is built in a factory, hot functionally tested & shipped to site as a finished machine. Construction on site is largely installation, foundations, piping, electrical connection, using conventional materials & repeatable processes. That architecture shifts risk into manufacturing & compresses timelines. Rather than building the hardest part on site you are simply installing it in 24-36 months. Nuclear does not behave this way. It can incorporate modular components, but the NSSS is only 25-40% of cost. The dominant cost drivers sit elsewhere. Civil works, excavation, basemat, containment, seismic qualification, remain site specific & labour intensive. Nuclear grade quality assurance, documentation, & inspection add another layer of fixed overhead. Safety systems with redundancy and independence are function driven, not size driven, so they do not shrink proportionally with output. The nuclear steam supply system is not analogous to the gas turbine in a CCGT. It is not a fully integrated, factory proven machine that arrives ready to run. The plant comes together on site, under regulatory oversight, with integration, testing & certification happening during construction & commissioning. This is why economies of scale are so strong in nuclear. Many of the costs do not scale linearly with power. When you reduce reactor size, you reduce output & revenue, while a large share of the cost base remains. Studies show that smaller reactors actually increase the relative share of on site construction because the civil works do not shrink in proportion to capacity. The SMR thesis assumes nuclear can transition from a project to a product, capturing the modular, factory built economics of gas plants. The constraint is that the parts of nuclear that dominate cost remain stubbornly project based. None of this explains why the comparison is made in the first place. CCGTs are extraordinarily compelling. They are marvels of thermally efficiency, capital light, fast to deploy & supported by a global supply chain of standardized components. They are the most successful large scale power plants of the past decades. It is natural that nuclear developers would look at that model & attempt to emulate it but in so doing they are committing a grave category error, an error that sets the western nuclear industry up for decade(s) of disappointment. Some SMRs will get built but they will not replicate the CCGT promise. They will be mini versions of large reactors with mini revenues to pay off the significant inherent costs of nuclear.

English

At 24 years old, SpaceX is already one of the largest & most *capital-efficient* companies ever built:

SpaceX: ~$12B raised → $1.25T Val (target $1.75T IPO)

OpenAI: ~$170B raised → $840B Val (target $1T IPO)

SpaceX Financial Profile (Over 1 Year):

2025: $350B → 2026: $1.25T Valuation

March 2025: $350B val, SpaceX had raised only ~$10B over 23 years, remarkably modest for its scale & valuation, +was already cash flow positive

FY 2025: Generated about $8 billion in profit on $15-$16B of revenue, driven primarily by @Starlink's satellite internet service, which accounts for between 50% - 80% of total revenue (Reuters)

February 2, 2026: $1.25T valuation, all-stock acquisition of xAI. Deal valued standalone SpaceX at ~$1 trillion & xAI at $250 billion. Widely reported as the largest M&A transaction in history.

March 2026: @elonmusk announces SpaceXAI + Tesla TERAFAB Project, goal to reach a trillion watts of compute/year

2026: Targeting ~$1.75 trillion IPO

Note: @xai (now part of @SpaceX) has reportedly raised ~$42B total (PitchBook). Combined, that’s ~$54B total capital against a ~$1.25T valuation.

Figures based on recent public reporting; estimates may vary.

Christian Garrett (@CGarrett_15) of @137ventures

X Freeze@XFreeze

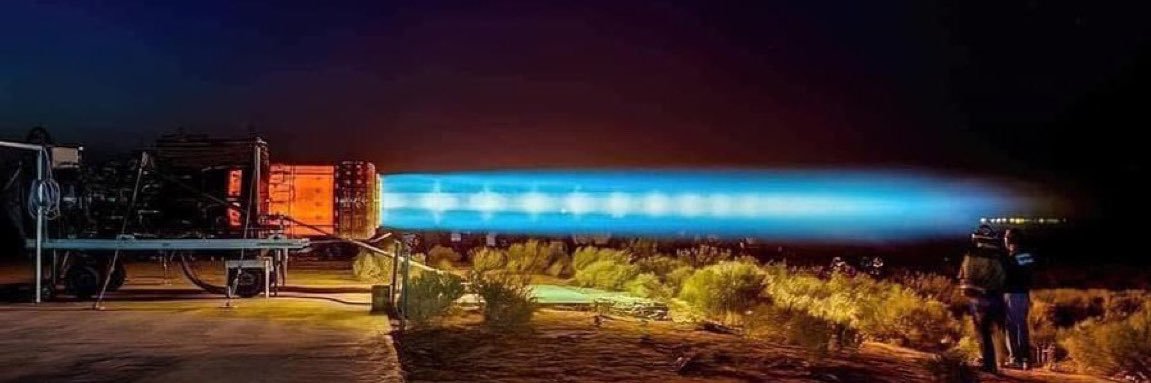

It’s actually insane what SpaceX is doing to the space industry right now In 1981, it cost ~$65,000 to put 1 kg into orbit For 50 years, the industry accepted this as the standard. Reusable rockets were "impossible" Then one company - led by a man obsessed with getting humanity to Mars, decided that $65,000/kg was unacceptable Right now, Elon and the SpaceX team are building Starship to hit $10–$20/kg That is a massive ~4,000x price collapse It’s actually wild that we get to watch this happen in real time

English

#TERAFAB is monumental and will be added once it’s operational.

x.com/spacex/status/…

Alan Simon@SlashSimon

The Tired, Old, Obsolete Industrial Order Is Finally Over Two huge new factories from Anduril in Ohio and Hadrian in Alabama just opened. This is signal, not noise. It represents a shift in how America builds at scale. For decades, U.S. industrial decline wasn’t just about fewer factories, it was about losing the center of gravity of production: speed, iteration, and control of the full stack. What @PalmerLuckey/@anduriltech and @2112Power/@HadrianInc are doing is reconstituting that center of gravity in America, but with fundamentally new architectures. Anduril’s Arsenal-1 factory in Ohio isn’t a traditional defense plant. It’s a software-defined arsenal. High-rate autonomous systems production, vertically integrated, designed for continuous iteration. This is closer to a hyperscale data center mentality than a Cold War factory. It collapses the timeline between design, production, and deployment. Hadrian’s Factory 4 in Alabama does something equally important but further upstream: it rebuilds precision manufacturing capacity using automation-first machine shops. Not just more machining, but programmable, scalable, and repeatable production that removes one of the biggest chokepoints in aerospace and defense supply chains. Together, they signal three deeper truths: 1. American factories are being re-invented, not just rebuilt. These are not legacy plants with incremental upgrades. They are new production primitives with software, robotics, and AI embedded at the core. This is the industrial equivalent of cloud-native vs on-prem. 2. The geography of American industry is re-expanding. Ohio and Alabama matter. This isn’t coastal tech cosplay. It’s the reactivation of interior industrial corridors. The map is shifting back toward places that can support scale: land, power, workforce, and logistics. 3. The bottlenecks are being attacked directly. Anduril targets defense production speed. Hadrian targets precision manufacturing capacity. These are not random bets, they are aimed squarely at the constraints that have limited U.S. industrial output for decades. Factories like these do important things that create real signal: •They attract adjacent suppliers and talent •They force competitors to respond •They increase national production throughput in measurable ways This is how flywheels start. The real question is whether these new factories are early nodes in a much larger graph? Is this the beginning of a new American production stack where the center of gravity shifts back to speed, scale, and sovereign capability? The answer is yes and this is a tipping point that will help propel America into a safe and prosperous future! #Anduril #Arsenal1 #Hadrian #Factory4 #America #Ohio #Alabama #Industrialinspiration

English

@JLopas @aphysicist Modern versions of factory towns will hopefully soon emerge.

English

@aphysicist West Texas is pretty clearly the right place for this. Abundant solar + the regulatory ability to build.

Harder to recruit talent, though. Would need to do a similar thing to Starbase where the city needs to be built around the factory.

English

possible terafab sites??

- ports (piketon, OH): ~3,700 acres, ~10 gw, ~$60–70b, softbank / sb energy, doe, aep

- gw ranch (pecos, TX): ~8,000+ acres, ~5–7.6 gw, multi-$10b, pacifico energy

- lea county (NM): ~3,500 acres, ~7–10+ gw, multi-$10b, new era energy

- monarch campus (WV): ~2,250 acres, ~8 gw, ~$10–15b implied, nscale (nvidia-backed)

- homer city (PA): ~3,000+ acres, ~4–5 gw, multi-$10b, energy/infrastructure consortium

Elon Musk@elonmusk

No, that’s just the little advanced technology fab, where we will be iterating on chip designs. We couldn’t possibly fit the Terafab on the GigaTexas campus. It will be far bigger than everything else combined there. Several locations for Terafab are under consideration. It needs thousands of acres and over 10GW of power at full scale.

English

The Tired, Old, Obsolete Industrial Order Is Finally Over

Two huge new factories from Anduril in Ohio and Hadrian in Alabama just opened.

This is signal, not noise. It represents a shift in how America builds at scale.

For decades, U.S. industrial decline wasn’t just about fewer factories, it was about losing the center of gravity of production: speed, iteration, and control of the full stack.

What @PalmerLuckey/@anduriltech and @2112Power/@HadrianInc are doing is reconstituting that center of gravity in America, but with fundamentally new architectures.

Anduril’s Arsenal-1 factory in Ohio isn’t a traditional defense plant. It’s a software-defined arsenal. High-rate autonomous systems production, vertically integrated, designed for continuous iteration. This is closer to a hyperscale data center mentality than a Cold War factory. It collapses the timeline between design, production, and deployment.

Hadrian’s Factory 4 in Alabama does something equally important but further upstream: it rebuilds precision manufacturing capacity using automation-first machine shops. Not just more machining, but programmable, scalable, and repeatable production that removes one of the biggest chokepoints in aerospace and defense supply chains.

Together, they signal three deeper truths:

1. American factories are being re-invented, not just rebuilt.

These are not legacy plants with incremental upgrades. They are new production primitives with software, robotics, and AI embedded at the core. This is the industrial equivalent of cloud-native vs on-prem.

2. The geography of American industry is re-expanding.

Ohio and Alabama matter. This isn’t coastal tech cosplay. It’s the reactivation of interior industrial corridors. The map is shifting back toward places that can support scale: land, power, workforce, and logistics.

3. The bottlenecks are being attacked directly.

Anduril targets defense production speed. Hadrian targets precision manufacturing capacity. These are not random bets, they are aimed squarely at the constraints that have limited U.S. industrial output for decades.

Factories like these do important things that create real signal:

•They attract adjacent suppliers and talent

•They force competitors to respond

•They increase national production throughput in measurable ways

This is how flywheels start.

The real question is whether these new factories are early nodes in a much larger graph? Is this the beginning of a new American production stack where the center of gravity shifts back to speed, scale, and sovereign capability?

The answer is yes and this is a tipping point that will help propel America into a safe and prosperous future!

#Anduril #Arsenal1 #Hadrian #Factory4 #America #Ohio #Alabama #Industrialinspiration

English

Great to host @howardlutnick and his team at our factory – the largest autonomous aircraft manufacturing facility in the US. We are at the beginning of another industrial revolution. AI and robotics will dramatically remake the world over the next 5-10 years. Done right, we can save lives, save money, and save time. Today America is the global leader in autonomous logistics and @zipline is working hard to keep it that way

English

I'm a simple man.

All I want is to build a generational company that brings heavy industry back to America at the largest possible scale.

English

The Genesis Mission is one of the most important moves in American industrial revival. This mission will tackle some of America’s most complex science and technology challenges.

Through a $293 million Request for Application (RFA) titled The Genesis Mission: Transforming Science and Energy with AI, DOE is inviting interdisciplinary teams to leverage novel AI models and frameworks to address over 20 national challenges spanning advanced manufacturing, biotechnology, critical materials, nuclear energy, and quantum information science.

Full details 👉 science.osti.gov/Funding-Opport…

#DOE #GenesisMission

U.S. CTO Ethan Klein@USCTO47

What did y’all think the Genesis Mission meant? vibes? papers? essays? We are funding a national scientific effort. Nearly $300M to kick things off and we’re just getting started! Advanced manufacturing ✅ Biotechnology ✅ Critical materials ✅ Nuclear energy ✅ Quantum ✅

English

Identifying the Startups Most Likely to Build the Nvidia of Biocomputing

Biological computing is a field where living biological systems (cells, DNA, proteins, and neurons) are used to store information, process data, and perform computations. This is similar to how silicon chips work in traditional computers.

Instead of using transistors and electricity, biological computing uses biochemical reactions inside living systems. Think of it as programming biology the way we program software.

The Biological Compute Stack

The sector is emerging in four layers:

1. Wetware compute with neurons / cells performing computation

2. Molecular memory with DNA data storage + DNA logic

3. Bio-electronic interface with chips connecting silicon to biology

4. Biological manufacturing with DNA synthesis and molecular tooling

The platform winners will likely control multiple layers simultaneously.

Tier 1

Category-Defining Platforms

Cortical Labs

Cortical Labs is currently the most advanced biological compute startup.

Their system is a CL1 biological computer with ~200k living neurons grown on silicon electrodes.

The Biological Computing Company

This company is pursuing biological AI accelerators. Instead of building a standalone biological computer, the company wants to integrate neuron-based processors directly into AI pipelines. This could become the first practical hybrid bio-AI compute architecture.

FinalSpark

FinalSpark focuses on biological neural networks as cloud infrastructure. Their neuroplatform allows researchers to remotely interact with living neuron cultures.

Tier 2

Molecular Computing and DNA Infrastructure

Biomemory

Biomemory is building commercial DNA data storage systems. DNA is the densest storage medium known. One gram of DNA could theoretically store~200 petabytes of data.

Atlas Data Storage

Atlas emerged from Twist Bioscience with a large seed round. The company aims to industrialize DNA data center storage.

Roswell Biotechnologies

Roswell is building molecular electronics chips that detect and manipulate single molecules. This technology could become a critical bridge between semiconductor chips

and biological molecules.

Tier 3

Biological Manufacturing Infrastructure

DNA Script

DNA Script builds enzymatic DNA synthesis machines. These machines print DNA sequences on demand.

Ansa Biotechnologies

Ansa focuses on long-strand DNA synthesis. Longer sequences are critical for storing large data blocks and running complex molecular computation.

Evonetix

Evonetix is bringing semiconductor-style manufacturing control to DNA synthesis. This approach could make DNA production scalable, precise and programmable.

Molecular Assemblies

This company also focuses on enzymatic DNA synthesis. Their approach may enable higher fidelity DNA manufacturing.

For American industrial strategy, biological computing represents a frontier technology on par with AI accelerators, nuclear power, and advanced robotics.

#biocomputing #industrialinnovation

English