@MoodyWriter13 It‘s LPKF’s management talking about the volume ramp next year, Philoptics says the same.

English

Wonderboy

3.4K posts

@SonicTed

Interested in commodities, tech, macro picture and frauds

$LPK, >80% of TGV/metallisation players have already qualified and purchased equipment. Where could valuation go? Some speculation, as glass substrates are an entirely new and emerging market: > Advanced IC substrate market: $14bn organic today, total market → $31bn by 2030 (Yole) > AI/HPC/data centre: estimated quarter to a third of that and the fastest-growing segment. Could be a c.$10bn market by 2030, could be significantly higher given the scale and pace of the AI buildout > If glass becomes standard for AI packaging, which $INTL, Samsung, $TSMC and the entire Korean ecosystem are betting on, then a large share of AI substrate production could flow through LPKF's technology > Every glass core substrate needs TGVs drilled through it. LPKF's LIDE is the leading production-proven method at panel scale (>80% share, with Philoptics as the main competitor) > The equipment layer typically captures 10-15% of end-market value during buildout phases. LPKF's addressable share (TGV formation + singulation + bonding) is perhaps c.30% of that equipment layer. > At a $10bn AI substrate market, that gives LPKF c.$300-450m in annual revenue > Apply $ASML's 10-year median P/S of c.10x and you get c.€3-4bn. Current market cap: ~€250m. That's a 12-16x. I hold a long position in $LPK

$AIXA controls ~90% of InP MOCVD reactors and every one ships with LayTec metrology inside, the only provider ensuring atomic-level precision. LayTec is owned by Nynomic (M7U), a tiny German photonics group valued below its book value. open.substack.com/pub/fwriter/p/…

so the platform group is going ski slope style, incredibly cheap but black box serial acquirer. $TPG ?

$LPK, why am I excited? You don't need to go to China to get glass mate... > Glass core substrates are the future of semiconductor packaging. Intel, Samsung, Absolics, TSMC. They're all building glass core capability for AI packaging. > $LPK sits right in the middle of it. Think ASML for glass, the enabling equipment layer every manufacturer needs. > Their LIDE technology is the dominant process for Through Glass Via fabrication, and their CEO has confirmed an exclusive, paid engagement with a "well-known" US semiconductor partner for CPO-on-glass work. I think this is $INTC. > $LPK's entire market cap today? c.€250m. > Here's a supply chain diagram showing where glass substrates fit alongside $LITE, $COHR, and the other names you know. A couple to call out: - InP / GaAs substrates: that's $AXTI - SOI Wafer: that's $SOI > Every other stage in the supply chain is already bottlenecked or bracing for demand surges.... PS. More thoughts on $LPK's solar business to follow.

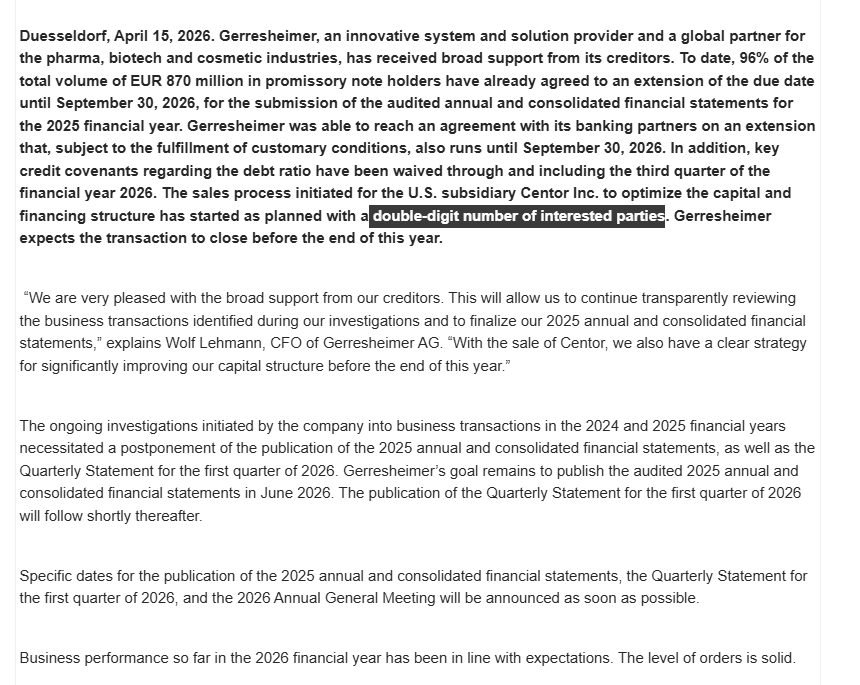

@alexthegreat183 Yeah looks bad, but they are also selling centor and guiding FCF positive. They bought Centor for $725m in 2015. I think today it's worth more like $450-$700m. Net financial debt is 1.9Be Q3/25. So that would remove at least 25% of it. They say a lot of interested buyers.