ทวีตที่ปักหมุด

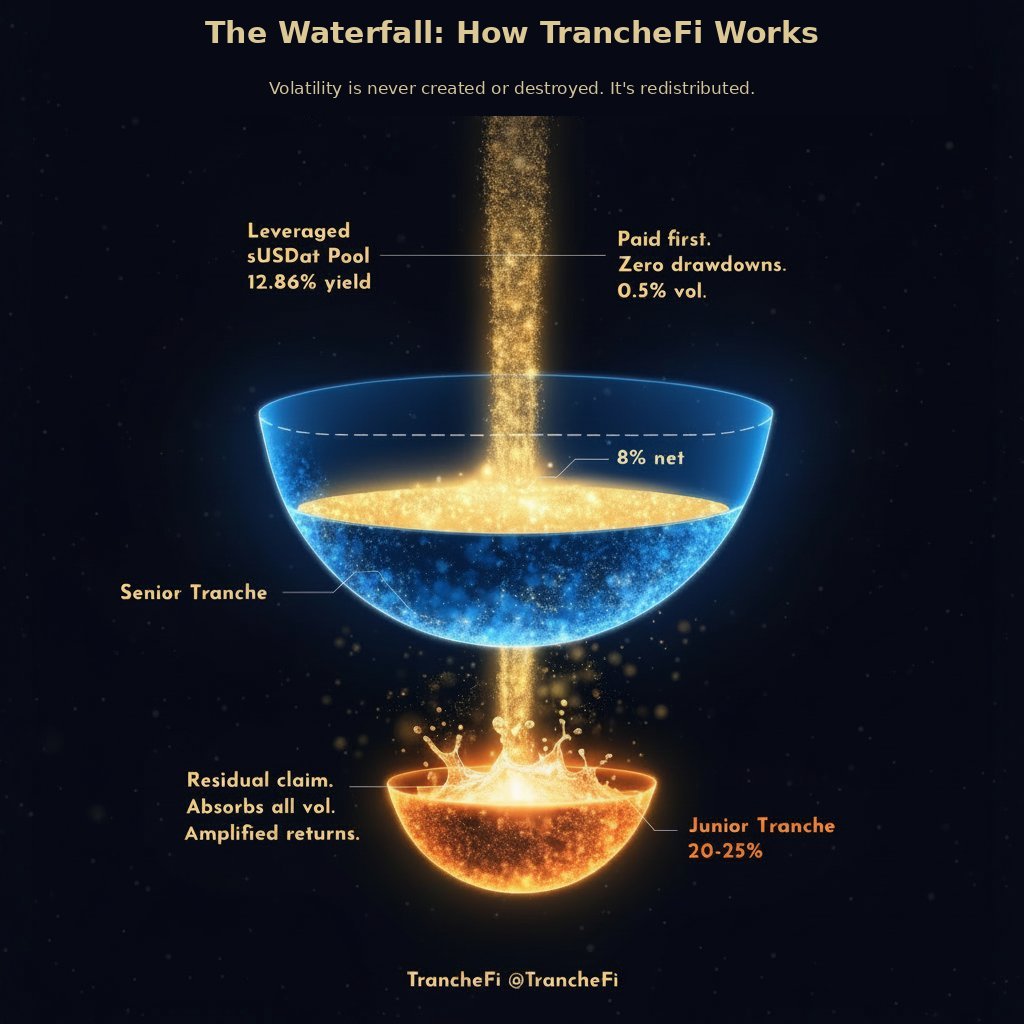

TrancheFi is a two-tranche yield vault built on Bitcoin credit.

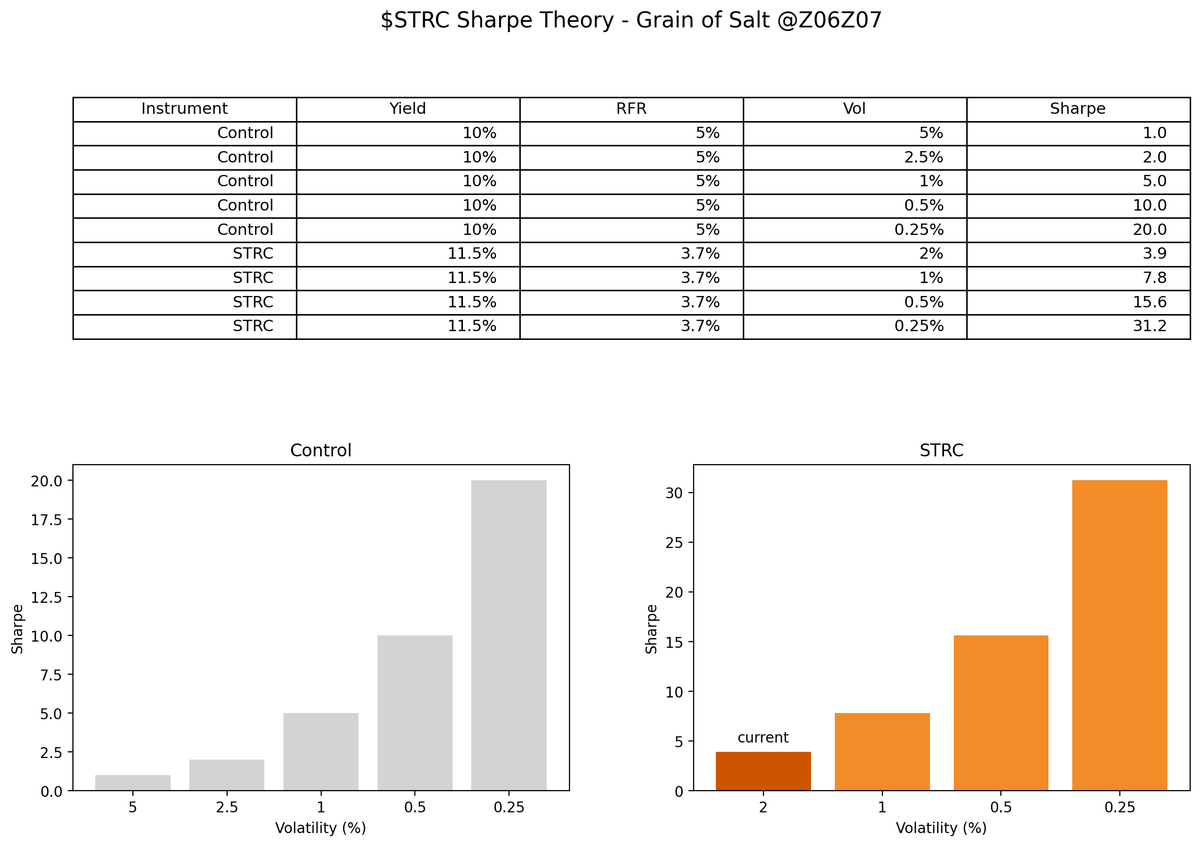

Leveraged sUSDat @saturn_credit (STRC wrapped on chain) produces a conservative estimate of 12.86% pool yield. The waterfall pays out in order:

1. Senior fills first. 8% net. Zero drawdowns. Paid before anything else.

2. Everything left over flows to junior. 20-25% net. Amplified because the overflow concentrates on 30% of the pool.

Same collateral. Same pool. One investor's stability is another investor's amplified return.

Backtested on 149 days of real STRC data through two Bitcoin crashes. Senior: zero negative weeks. Junior: recovered every drawdown within 3-6 weeks.

Structured finance meets DeFi infrastructure.

More soon.

English