Valentin รีทวีตแล้ว

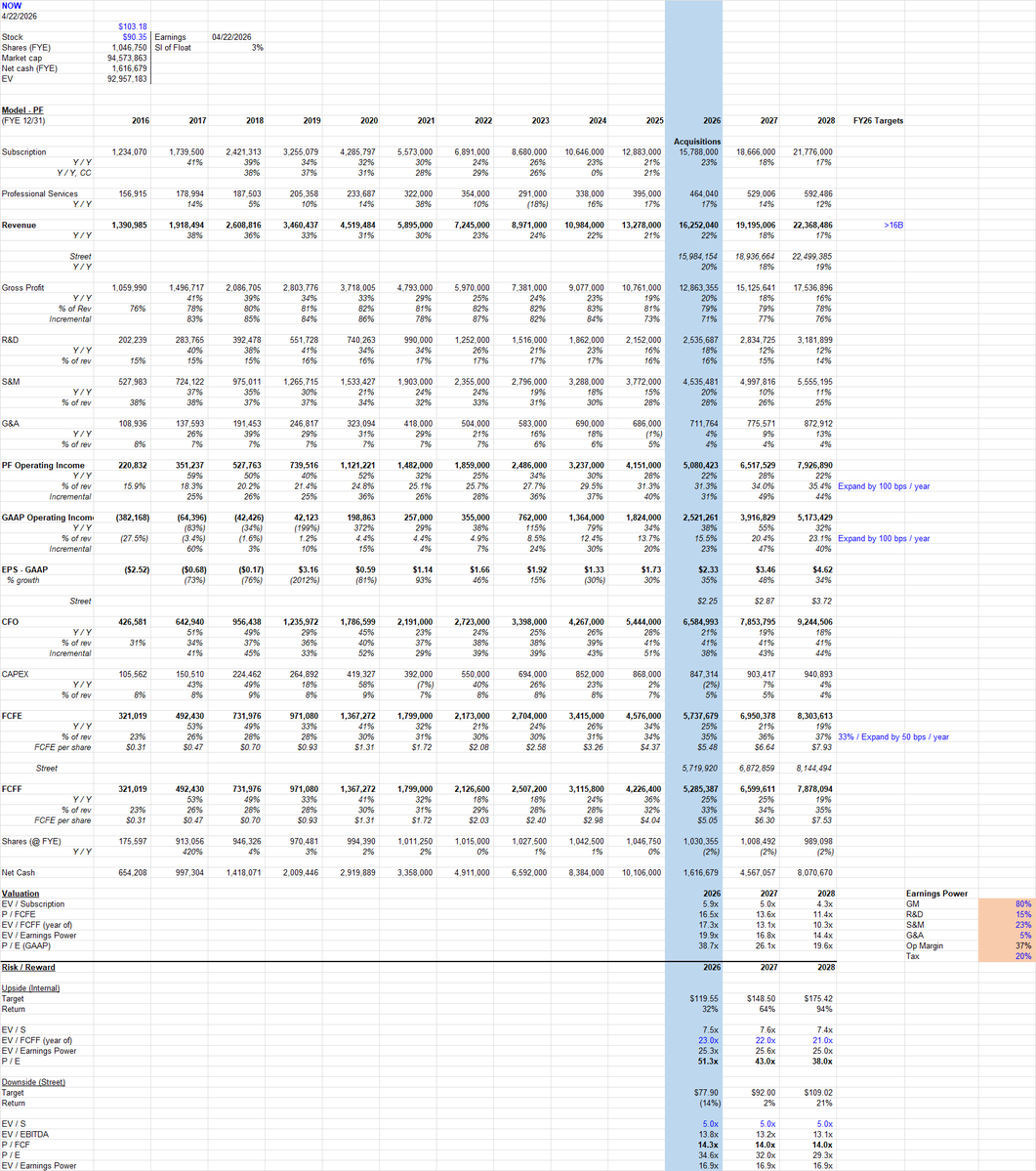

$NOW reported a squishy qtr with some wrinkles due to macro and acquisitions. AI is doing well but not accelerating the business yet.

Story is moving sideways although has ingredients for improvement. Numbers moving sideways as well.

Risk / reward is interesting.

Downside of -14% to 14x 2026 street FCF / 35x GAAP PE / 17x my measure of taxed earnings power.

Upside of 64% to 22x my 2027 FCF / 43x GAAP PE / 26x earnings power. Probably plenty of debate on what multiples to use. A clear acceleration in the business would probably take stock here or higher.

Qtr

Subscription rev growth was 18% yy cc organic down from 19.5-21.5% range last year.

Now the company said that growth would have been 75 bps faster if not for Middle-east deals pushed out by the war, and they said last qtr that growth this qtr would have a 150 bps headwind from self-hosting rev moving to hosted [oddly didn’t mention that again though].

So a forgiving look at Q1 growth suggests 18.75-20.25% depending on what you want to add back. No acceleration but at least a more modest decel perhaps.

cRPO math is even tougher but I calculate 20% yy cc organic – same as Q4.

Customer metrics were all strong w/ customers worth > $5 growing 22% yy. The one downtick was gross retention which ticked down from 98% to 97% (was last at 97% in Q1/Q2 of 2021).

Cash GM of 79.3% down from 82.1% last Q1 – primarily from move to hosting on hyperscalers from their own data centers, but also from ramp of AI.

PF OM of 31.8% up from 30.9% last Q1. SBC of 14.8% down from 15.2% last Q1 – nice but absolute SBC also grew 19% yy which is no bueno. Could be retention grants to acquired companies. They seem to get it as far as bringing SBC down though and brought it up multiple times.

GAAP OM of 14.6% excluding amortization was flat yy.

Guidance was confusing / soggy quantitatively while positive qualitatively.

The discussion on product / adoption was all positive.

AI revenue bogey was increased from 1b ARR this year to >1b ARR in prepared remarks, and then CEO / CFO said 1.5b is on the table. If they can hit the 1.5b, that implies ~10% of the business will be AI token derived by year-end growing ~150% yy.

Q2 guidance for subscription revenue implies 19.75-20.25% cc organic assuming the normal 100 bps beat (headline guide is 21-21.5% cc - 100 bps Moveworks - 125 bps Armis + 100 bps cushion). So technically an acceleration from the 18% in Q1.

Q2 guidance for cRPO implies 18.3% cc organic assuming 100 bps beat (19.5% guidance cc – 100 bps Moveworks - 125 bps Armis + 100 bps cushion).

The team suggested revenue ought to accelerate and would provide longer-term guidance at the upcoming analyst day. Seems plausible although I would guess the market will need to see it first, and we’ll need to see magnitude.

Margin guidance took a hit from the Armis acquisition closing early. By my math, they are guiding to 161m in Armis rev this year which makes no sense compared to their commentary on 12/23/25 deal announcement which said it is 340m in ARR growing 50% yy. CFO basically said acquisition math is sandbagged. They said Armis will be a 2% headwind to FCF which implies it will burn 325m / year. I’m guessing the burn is hopefully less and the revenue contribution meaningfully more.

Company decreased margin guidance for the year. GM will be 81.5% down from 82.0%. PF OM will be 31.5% down from 32.0%. FCF will be 35% down from 36%.

Other Highlights

-50% of net new ACV is not seat based. Foots w/ diligence that customers think of NOW as a solution.

-Moveworks closed more 7 figure deals in Q1 than all of last year.

-Analysts are going to be excited by what they see at upcoming analyst day.

English